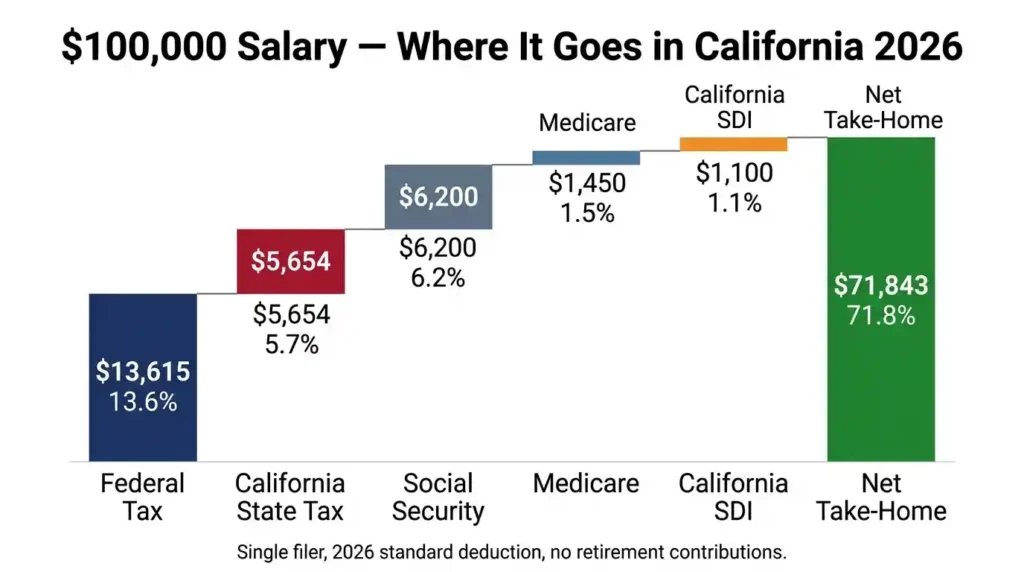

A $100,000 salary in California leaves a single filer with roughly $71,843 per year after federal tax, state tax, FICA, and SDI in 2026. That is approximately $5,987 per month before any employer benefit deductions. Run your exact numbers with our California paycheck calculator.

After 8 years helping people read their real paychecks, I have seen this number land hard. California’s effective total tax rate of 28% compounds with average Bay Area rents above $3,100, leaving less than $2,700 for everything else.

$100k is workable in California. But location determines whether you are surviving or building wealth.

The Quick Answer: How Much Is $100k After Taxes in California?

Here is the number you came here for.

A single filer earning $100,000 in California takes home roughly $71,843 per year after all taxes in 2026. That works out to about $5,987 per month. This estimate uses the California standard deduction, assumes no dependents, and includes no retirement contributions.

If you are married filing jointly, your household tax burden drops. A married couple where one spouse earns $100,000 takes home closer to $76,800 per year. The lower effective tax rate is the reason married couples often feel more financially comfortable at the same gross income.

Head of household filers land somewhere in the middle, closer to $73,200 per year, depending on qualifying dependents and deductions.

Your actual paycheck may be slightly lower. Employer benefit deductions like health insurance, dental, and 401(k) contributions come out before you even see the money. We cover those in detail below. Earning more? See how a $150k salary is taxed in California for comparison.

Your $100k Paycheck by Pay Period

Here is what $100,000 looks like broken down by pay period for a single filer in California in 2026. If you are new to reading California paychecks, our paycheck basics guide explains every line before you get to the numbers.

- Monthly: approximately $5,987

- Biweekly (every 2 weeks): approximately $2,763

- Weekly: approximately $1,382

- Hourly equivalent (after taxes, based on 40 hrs/week): approximately $34.54

These numbers assume standard withholding. Your real paycheck could vary based on your W-4 and DE-4 withholding elections, company benefits, and local city taxes (yes, some California cities have extra taxes).

Free California Tax Tool

Calculate What You’ll Actually Take Home

Stop guessing. Enter your California salary and see your real paycheck — federal tax, state tax, SDI, and all deductions included.

🧮 Calculate What You’ll Actually Take HomeUsed by thousands of California workers · FTB-verified 2026 rates

Quick Salary Snapshot Table

| Category | Amount |

|---|---|

| Gross Annual Salary | $100,000 |

| Federal Income Tax | $13,753 |

| California State Tax | $5,654 |

| Social Security (FICA) | $6,200 |

| Medicare | $1,450 |

| California SDI | $1,100 |

| Total Taxes Paid | $28,157 |

| Net Annual Income | $71,843 |

| Net Monthly Income | $5,987 |

| Effective Total Tax Rate | 28.2% |

Note: These figures are estimates for a single filer using the 2026 standard deduction. Rounding applies.

Takeaway: A $100k salary means roughly 28 to 30 cents of every dollar goes to taxes in California.

Why a $100k Salary in California Feels Smaller Than Expected

I call it the “six-figure illusion.” You earn six figures on paper but live on what is left after taxes, rent, and inflation take their cut. In California, those forces compound hard. When your rent is $3,200 and take-home is $5,900, you have $2,700 left for everything. That is thin purchasing power no matter what your salary sounds like.

The Psychological Shock of Six Figures in California

You spent years working toward six figures. Then the first paycheck arrives and you do the math on rent and groceries. Suddenly $100,000 feels like a lot less. If you have ever asked why your California paycheck feels so low, you are not alone.

Lifestyle inflation makes it worse. Many new six-figure earners upgrade their car, apartment, and social spending all at once. The salary did not change their life. Their spending did. The smarter move is to keep living like you earned $75,000 and invest the gap.

Reality Check: Location Changes Everything

A $100,000 salary does not mean the same thing in every California city.

In San Francisco, $100,000 is below the area’s median household income. Rent for a one-bedroom apartment near the office can eat $3,000 or more per month. Use our San Francisco paycheck calculator to see exactly what you keep after all deductions.

In Sacramento, Fresno, or Bakersfield, $100,000 is genuinely comfortable. Rent for a nice two-bedroom apartment might run $1,400 to $1,800. You could actually save money, build an emergency fund, and maybe buy a home.

Rent-to-Income Ratio: The Number That Tells the Real Story

Financial experts say your rent should stay under 30% of your gross income. On a $100k salary, that means keeping rent at or below $2,500 per month.

In the Bay Area, the average one-bedroom runs $3,100. That is 37% of your gross income before you spend a single dollar on anything else. In Riverside or Stockton, a one-bedroom averages $1,500. That leaves you room to breathe, save, and actually enjoy your salary.

Takeaway: Where you live in California matters as much as what you earn.

Is $100k Enough to Live Comfortably in California?

The honest answer is: it depends.

“Comfortable” means something different to a single 28-year-old renting a studio than it does to a family of four trying to afford a mortgage. Comfort is relative. But I can give you a real breakdown for the most common situations.

Surviving vs Building Wealth: Know Which Category You Are In

Surviving means bills are paid and you are not going into debt. Building wealth means you are also investing and growing your net worth every month. In expensive California cities, most $100k earners are surviving. In inland cities, they can be building wealth. Knowing the difference is step one.

Comfortable for a Single Professional?

Yes, outside the Bay Area. With roughly $5,987 monthly take-home, a single person can afford a $1,600 to $2,200 one-bedroom, cover a car payment, eat well, and still save $500 to $1,000 per month. In San Francisco or Santa Monica, a one-bedroom costs $3,200 or more and that savings cushion nearly vanishes.

Student loans make it harder. A $500 monthly payment cuts disposable income sharply. It is the most common complaint I hear from young California professionals at this salary level.

Travel, Entertainment, and the Flexibility Factor

A realistic entertainment budget of $400 to $600 per month is not extravagant for a young professional. Factor that in and your savings margin shrinks fast. In the Bay Area, a single person at $100k may only save $500 to $800 per month after living a normal social life. Still positive, but far from the lifestyle people imagine.

Comfortable for a Family?

For a family, $100,000 as a single income is genuinely difficult in California. Childcare alone runs $1,500 to $2,500 per month per child. Add healthcare, a car, groceries for four, and rent above $2,500 and you are already over your net income.

Dual-income households change the picture. Two earners at $50,000 each pay less in taxes proportionally and cover expenses with more breathing room. In inland California, a $100k single-income family can still build a good life with intentional budgeting.

Can You Buy a House on $100k in California?

In most parts of California, buying a home on a $100,000 salary alone is very difficult.

Lenders typically use a 28% front-end ratio guideline. That means your monthly mortgage payment should stay under about $1,652 based on your gross income. At current interest rates, that payment only supports a home loan of roughly $280,000 to $320,000. California’s median home price is over $800,000 statewide.

That said, ownership is still realistic in certain inland areas. Cities like Fresno, Bakersfield, Stockton, and parts of the Central Valley still have median home prices in the $350,000 to $500,000 range. A $100k salary combined with a strong down payment and a clean credit profile can get you in the door.

The Down Payment Barrier: The Biggest Obstacle Nobody Talks About

A 20% down payment on a $400,000 home is $80,000. Saving $1,000 per month gets you there in nearly 7 years. Many buyers use a 3 to 5% FHA loan to lower the barrier, but that adds private mortgage insurance. Knowing the real timeline lets you plan honestly instead of guessing.

Takeaway: Buying a home on $100k in California is possible, but only in specific inland regions.

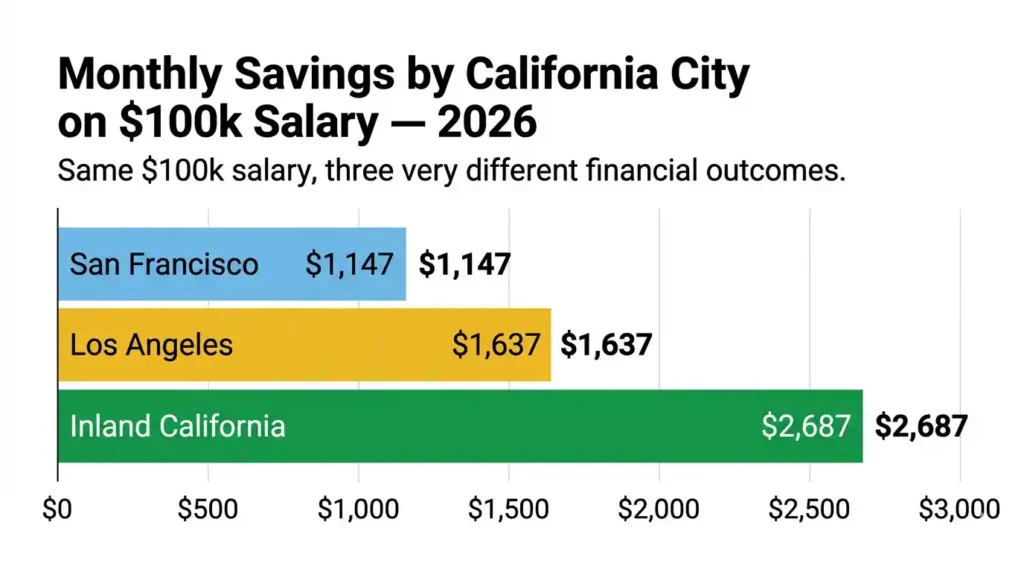

What $6,000 Per Month Actually Looks Like in California

Here are real monthly budgets for three California cities. One often-missed detail: streaming, gym, and app subscriptions quietly add $100 to $200 per month. Audit those first.

Bay Area Budget Example (San Francisco or San Jose)

| Expense | Monthly Cost |

|---|---|

| Rent (1BR apartment) | $3,100 |

| Utilities | $160 |

| Groceries | $500 |

| Transportation (car + gas or BART) | $450 |

| Health insurance (after employer) | $150 |

| Phone | $80 |

| Entertainment and dining | $400 |

| Total Expenses | $4,840 |

| Leftover to save | $1,147 |

Living in the Bay Area on $100k works, but one unexpected expense wipes your savings month.

Los Angeles Budget Example

| Expense | Monthly Cost |

|---|---|

| Rent (1BR apartment) | $2,400 |

| Utilities | $140 |

| Groceries | $480 |

| Car payment + gas + insurance | $650 |

| Health insurance (after employer) | $150 |

| Phone | $80 |

| Entertainment and dining | $450 |

| Total Expenses | $4,350 |

| Leftover to save | $1,637 |

Los Angeles requires a car. There is almost no way around it. But your rent-to-income ratio is better than San Francisco. With discipline, a single person at $100k in LA can save meaningfully and even build an investment portfolio. Use our Los Angeles paycheck calculator to verify your exact take-home for that market.

Inland California Budget Example (Sacramento, Fresno, or Riverside)

| Expense | Monthly Cost |

|---|---|

| Rent (2BR apartment) | $1,600 |

| Utilities | $120 |

| Groceries | $450 |

| Car + gas + insurance | $550 |

| Health insurance (after employer) | $150 |

| Phone | $80 |

| Entertainment and dining | $350 |

| Total Expenses | $3,300 |

| Leftover to save | $2,687 |

This is where $100k actually starts to feel like $100k. Inland California gives you real savings power. Many remote workers have discovered this. They keep their coastal salary and cut their cost of living in half. The result is genuine wealth-building speed. If Sacramento is your target, our Sacramento paycheck calculator gives you a city-specific take-home estimate.

Takeaway: The same $100k salary can produce $1,000 or $2,600 in monthly savings depending on where you live.

Real California Salary Scenarios

Here are three real-world scenarios based on actual professions and cities. Browse more occupation-based examples in our California paycheck scenarios category.

$100k as a Software Engineer in San Jose

A software engineer at $100k base in San Jose earns below the regional average. After taxes, take-home is about $5,900. Rent near major tech campuses runs $2,800 to $3,400. Saving $800 to $1,200 per month is realistic after housing and basics.

The real wealth builder is RSUs. Many tech jobs add $20,000 to $80,000 in annual RSU income on top of base pay. But RSUs are taxed as ordinary income when they vest, so expect to lose 35 to 40% to taxes immediately.

Commuting in San Jose: The Hidden Time and Money Tax

Many engineers commute from cheaper cities like Fremont or Tracy. Gas, tolls, parking, and vehicle wear add $300 to $600 per month, eating directly into the savings advantage of living further out.

$100k as a Nurse in Anaheim

Nurses benefit from shift differentials. Night and weekend shifts carry premium pay taxed as supplemental income, but it still adds up. Strong employer benefit packages also mean your actual disposable income is often higher than a calculator shows. California’s healthcare worker minimum wage rules in 2026 also set a wage floor that affects total compensation planning.

Supporting a family in Orange County on $100k as a single income is very tight. Most nursing professionals rely on a spouse’s income or extra shifts to manage comfortably.

Retirement Contributions for Healthcare Workers

Nurses often have access to 403(b) plans. Contributing 6% reduces taxable income by $6,000, saving $1,500 to $1,800 in taxes per year. Many hospital systems match up to 3 or 4%. Maxing that match is the highest-return financial move available at this salary level.

$100k as a Remote Worker in Fresno

This is the scenario I find most compelling for wealth-building. A remote worker earning $100k from a tech company while living in Fresno keeps the same take-home as a San Francisco resident but pays $1,400 instead of $3,200 in rent. That $1,800 monthly gap, invested consistently, creates life-changing wealth. Remote workers who relocate inland in their 30s often reach homeownership a decade ahead of coastal peers. If you work as a contractor rather than an employee, your tax picture changes significantly — see our worker classification category for the full breakdown.

Takeaway: Remote work arbitrage is the most underrated wealth strategy for California earners.

Full Tax Breakdown on a $100,000 Salary in California

Here is exactly how your taxes are calculated. No jargon. Just the math.

Federal Income Tax Breakdown

The federal government uses a progressive tax system. Different portions of your income are taxed at different rates. For a single filer in 2026, the standard deduction is $15,000, bringing taxable income to $85,000. The IRS publishes the official federal tax brackets each year after inflation adjustments.

- First $11,925 taxed at 10% = $1,193

- $11,926 to $48,475 taxed at 12% = $4,386

- $48,476 to $85,000 taxed at 22% = $8,036

Total estimated federal income tax: approximately $13,615. Your marginal rate is 22%, but your effective federal rate is closer to 13.6%.

Marginal Rate vs Effective Rate: The Confusion That Costs People Money

Being in the “22% bracket” does not mean you pay 22% on everything. Only your last dollars are taxed at that rate. Your first $11,925 is still taxed at just 10%. This stops people from making bad decisions like refusing a raise to “avoid a higher bracket.” A higher bracket never makes your take-home smaller.

California State Income Tax Breakdown

California’s top rate is 13.3%, but at $100,000 a single filer lands in the 9.3% marginal bracket. After the state standard deduction and lower bracket rates on earlier income, the effective California rate is about 5.5 to 6%, roughly $5,500 to $6,000 per year. See the full California income tax brackets for 2026 for every rate tier.

Why California Taxes Feel Higher Than They Actually Are

California’s rates climb faster than most states. By approximately $66,300 of taxable income, a single filer already hits the 9.3% marginal bracket. That threshold is lower than most people expect. Every pay raise above that level hits 9.3% immediately, which is why raises feel like they disappear faster in California. The California Franchise Tax Board publishes the official state tax rate schedules for every filing status.

Social Security and Medicare (FICA Taxes)

FICA taxes are flat percentages, not progressive. Social Security takes 6.2% up to the 2026 wage base of $176,100, costing you $6,200. Medicare takes 1.45% with no cap, adding $1,450. Total FICA: $7,650 per year, applied before any deductions. The Social Security Administration confirms the 2026 wage base on its official site.

The Social Security Wage Cap: What It Means for Higher Earners

Social Security only taxes income up to $176,100 in 2026. At $100k you never hit that cap, so the full $6,200 applies all year. Earners above the cap see a mid-year paycheck bump when Social Security stops withholding.

California SDI Explained

SDI stands for State Disability Insurance. California removed the SDI wage cap starting January 1, 2024, so every dollar of income is now subject to the 1.1% rate. On $100,000 that is $1,100 per year. It funds short-term disability and paid family leave and quietly reduces every paycheck. The California Employment Development Department (EDD) maintains the official SDI rate and program details. Get the full breakdown of the California SDI rate for 2026 and how it is calculated.

Takeaway: Your total California tax burden at $100k includes federal tax, state tax, FICA, and SDI. Together they reduce your paycheck by roughly 28 to 30%.

Why Online Salary Calculators Show Different Results

Different tools make different assumptions about filing status, SDI, and health insurance. Your W-4 elections also change withholding. Bonuses are not simulated by most calculators, and biweekly payroll creates rounding differences across 26 pay periods. Always treat these numbers as estimates for planning, not guarantees.

Takeaway: Always treat online calculators as estimates, not guarantees. Use them to plan, not to predict.

Hidden Deductions That Reduce Your Real Take-Home Pay

Your taxes are just one piece of the puzzle. These employer deductions come out before taxes even apply in many cases. Learning how to read your California pay stub line by line is the fastest way to spot what is actually reducing your take-home.

- Health insurance premiums: Employer plans often cost employees $150 to $400 per month depending on coverage level and family size.

- Dental and vision: Usually small, around $20 to $50 per month, but they add up.

- 401(k) contributions: If you contribute 6% of your salary, that is $500 per month gone before taxes.

- HSA contributions: Health savings account contributions reduce your taxable income but also reduce take-home cash.

- ESPP (Employee Stock Purchase Plans): Tech workers often set aside 5 to 15% of their paycheck to buy company stock at a discount.

A person contributing 6% to a 401(k) and paying $250 per month in health insurance premiums might take home $800 to $1,200 less per month than the basic tax calculator shows. Employers managing these deductions correctly must also follow strict payroll compliance and reporting rules in California.

How a 401(k) Changes Your Financial Picture

Every dollar in a traditional 401(k) reduces your taxable income. Contributing $6,000 saves roughly $1,800 in taxes at a combined 30% marginal rate. A 4% employer match on $100k adds a free $4,000 per year. That is an instant 100% return. I call the 401(k) an “invisible raise” because it cuts your taxes, earns matching funds, and builds wealth simultaneously.

Bonus Pay, RSUs, and Overtime Taxes Explained

The IRS withholds 22% from bonuses as supplemental income. California adds 10.23%. That is roughly one-third withheld upfront. But your real tax liability is settled at year-end. If withholding exceeded your actual taxes owed, you get a refund. The large deduction feels painful but is usually just a prepayment. If overtime pay is part of your income, review California overtime laws in 2026 to understand how those earnings are taxed differently.

Takeaway: High bonus withholding is not a permanent loss. It is just a prepayment that gets adjusted at tax time.

Pro Tips to Keep More of Your $100k Salary

After 8 years of watching people earn $100,000 and wondering where it goes, here are the strategies that actually work.

- Max your 401(k) contributions to cut your taxable income immediately

- Open an HSA if your employer offers a high-deductible health plan

- Review your California DE-4 withholding form annually so you are not over-withholding interest-free

- Consider relocation to an inland California city if remote work is an option

- Audit subscriptions and recurring charges every six months

Insider Insight: The Salary Compression Trap

At $100,000 you pay $28,000 in taxes and another $24,000 to $36,000 in rent. That leaves $32,000 to $48,000 for everything else. A 10% raise adds maybe $6,500 in take-home. If rent went up $200 per month, your real gain is only $4,100. Control your rent aggressively and invest every raise before lifestyle inflation absorbs it.

Insider Insight: How High Earners Quietly Build Wealth

The wealthiest $100k earners automate investments before they can spend the money. On payday, funds move automatically to a 401(k), HSA, and brokerage. What is left is spending money. They keep housing under 30% of gross income and do not upgrade lifestyle with every raise.

Remote Work Arbitrage: The Quiet Wealth Accelerator

Keep the coastal salary. Cut the coastal rent. Moving to an inland city and freeing $1,500 to $1,800 per month can fund a full home down payment in five years. It is just math, and more people are doing it every year.

Takeaway: Controlling lifestyle creep and automating savings are more powerful than chasing a higher salary.

California vs Other States: Where Does $100k Go Furthest?

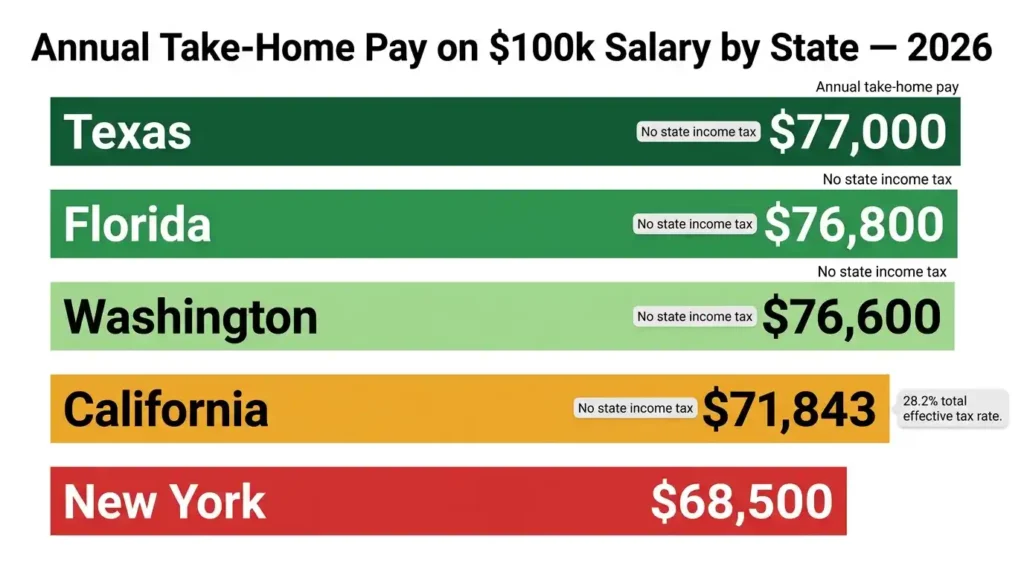

California vs Texas Take-Home Comparison

Texas has no state income tax, saving a California-level earner roughly $5,500 to $6,000 per year. Texas does carry higher property taxes of 1.5 to 2.5% annually versus California’s Prop 13 cap near 1%, and Austin housing has risen sharply. Still, a $100k earner in Dallas or Houston takes home $5,000 to $6,000 more per year. Over 10 years that is $50,000 to $60,000 in extra take-home before investment growth.

| State | Annual Take-Home | Approx Monthly | State Tax Saved vs CA |

|---|---|---|---|

| California | $71,436 | $5,953 | $0 |

| Texas | $77,000 | $6,417 | $5,564 |

| Florida | $76,800 | $6,400 | $5,364 |

| Washington | $76,600 | $6,383 | $5,164 |

| New York | $68,500 | $5,708 | -$2,936 |

Why Cost of Living Matters More Than Taxes Alone

Paying $3,200 in San Francisco rent and saving $1,000 per month is worse than paying $1,500 in Austin and saving $2,500. Even zero state tax would not close that gap. The real question is not which state has lower taxes. It is where your money produces the best quality of life and savings capacity.

Takeaway: Housing costs impact your financial future more than state income taxes for most $100k earners.

Common Myths About a $100k Salary in California

Myth vs Reality Table

| Common Belief | Actual Reality | Practical Takeaway |

|---|---|---|

| “Six figures means rich” | $100k is below median household income in SF | Budget on your $70k take-home |

| “Taxes take half your paycheck” | Effective total rate is closer to 28-30% | Significant but not 50% |

| “Everyone making $100k struggles” | Inland CA earners can thrive on this income | Location is the real variable |

| “Leaving CA automatically fixes finances” | Other states have different cost pressures | Run full cost-of-living math first |

Takeaway: $100k in California is a solid income. Understanding the real numbers lets you make it work.

Frequently Asked Questions About $100k After Tax in California

How much is $100k after taxes in California monthly?

A single filer earning $100,000 per year in California takes home roughly $5,987 per month after federal tax, state tax, FICA, and SDI. This estimate uses the 2026 standard deduction and assumes no additional benefit deductions. For a faster answer, use our annual salary calculator with your own numbers.

Is $100k considered middle class in California?

Yes, $100,000 puts you in the middle class in most of California. In the Bay Area, it is below the area median income and barely qualifies as middle class. In inland cities like Fresno or Bakersfield, it is solidly upper-middle class. The California Department of Finance uses regional income bands, and $100k lands differently depending on county. The California Department of Industrial Relations publishes official wage data that provides useful context on regional income standards.

Why is my paycheck lower than online calculators estimate?

The most common reason is benefit deductions. Health insurance, dental, vision, 401(k) contributions, and HSA contributions all reduce your paycheck before you see it. Online calculators rarely account for these. Add those deductions back in and the numbers usually line up. Our guide on why your California paycheck is lower than expected covers every cause in detail.

How much tax do you pay on $100k in California?

On a $100,000 salary in California, a single filer pays approximately:

- Federal income tax: $13,615

- California state income tax: $5,654

- Social Security: $6,200

- Medicare: $1,450

- California SDI: $1,100

- Total: approximately $28,019

That is an effective total tax rate of about 28.0%. For a complete overview of every layer, see our guide to California payroll taxes.

Can you live comfortably in Los Angeles or San Francisco on $100k?

In Los Angeles, yes. A single professional earning $100k can rent a decent one-bedroom, save $1,000 to $1,500 per month, and live comfortably with some sacrifice. In San Francisco, it is much harder. Housing costs alone can consume 50 to 55% of your net income. Comfortable is possible but requires very disciplined budgeting.

How can I reduce taxes on a $100k salary?

The four most effective strategies are:

- Contribute to a traditional 401(k) to reduce taxable income (2026 employee limit: $23,500 per the IRS 401(k) contribution limits)

- Open an HSA if you have a high-deductible health plan (2026 limits: $4,300 individual, $8,550 family per the IRS HSA contribution limits)

- Use a Flexible Spending Account (FSA) for healthcare or childcare costs

- Review your W-4 withholding on the IRS website and your California DE-4 to ensure accurate withholding

These steps can reduce your taxable income by $8,000 to $27,000+ per year depending on contribution levels, saving you $2,000 to $6,000 or more in taxes. Results vary by filing status and elections.

Note: Contribution limits are set by the IRS and adjust annually. Consult a tax professional for advice specific to your situation.

Why does $100k feel less valuable today?

Inflation, housing costs, and wage stagnation have all compressed the real value of $100,000 over the past decade. In 2015, $100,000 had roughly 25% more purchasing power than it does today after adjusting for California’s regional inflation rate. The income threshold that feels “comfortable” has risen faster than wages have for most workers.

What salary feels truly comfortable in California?

Based on what I have seen over 8 years, the number that feels genuinely comfortable for a single person in a mid-cost California city is around $120,000 to $140,000. For a family of four aiming to buy a home and save for retirement, the number climbs to $180,000 to $220,000 in household income. In the Bay Area, those numbers are even higher.

Final Verdict: What $100k in California Really Means in 2026

Earning $100,000 in California is a real achievement. But it does not automatically mean financial ease, especially in high-cost cities.

After taxes, a single filer takes home about $71,800 to $72,000 per year, roughly $5,987 per month. Whether that feels comfortable depends almost entirely on where you live and how you manage housing costs.

California rewards people who control rent, automate investments, and resist lifestyle creep. The $100k earner who lives modestly, maxes their 401(k), and moves inland can build real wealth faster than a $150k earner drowning in Bay Area rent. If you are a contractor or freelancer earning $100k, note that 1099 vs W-2 tax treatment in California significantly changes your effective take-home.

Do not chase a bigger salary. Chase a bigger gap between what you earn and what you spend. That gap is your real financial power in California. Understanding your rights under California labor laws also ensures you are never underpaid for what you have already earned.

Takeaway: $100k after tax in California is real, workable money. Spend it intentionally and it can be the foundation of a very good life.

Disclaimer: The figures in this article are estimates based on 2026 federal and California tax rates for illustrative purposes only. Individual results will vary based on filing status, deductions, employer benefits, and personal circumstances. This content is for informational purposes and does not constitute tax, legal, or financial advice. Consult a licensed tax professional or financial advisor for guidance specific to your situation.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.