The California standard deduction for 2026 is $5,706 for single filers and $11,412 for married filing jointly. California sets its own deduction independently from the IRS, so federal increases do not apply to your state return.

In 8 years of reviewing California returns, I have watched that $10,394 gap between the state and federal single-filer deduction silently inflate taxable income for thousands of filers. One client lost an expected $800 refund entirely because of it.

California’s deduction is far lower than the federal amount and excludes the senior bonus. Most itemizers must recalculate from scratch for the state return.

2026 California Standard Deduction Amounts (Your Quick Answer)

California Standard Deduction by Filing Status for 2026

| Filing Status | California Standard Deduction 2026 |

| Single | $5,706 |

| Married Filing Jointly | $11,412 |

| Married Filing Separately | $5,706 |

| Head of Household | $11,412 |

| Qualifying Surviving Spouse | $11,412 |

These numbers come directly from the California Franchise Tax Board (FTB). They apply to the 2025 tax year, which is the return you file in 2026. The FTB adjusts these amounts each year for inflation.

Takeaway: Your California standard deduction in 2026 is either $5,706 or $11,412, depending on your filing status.

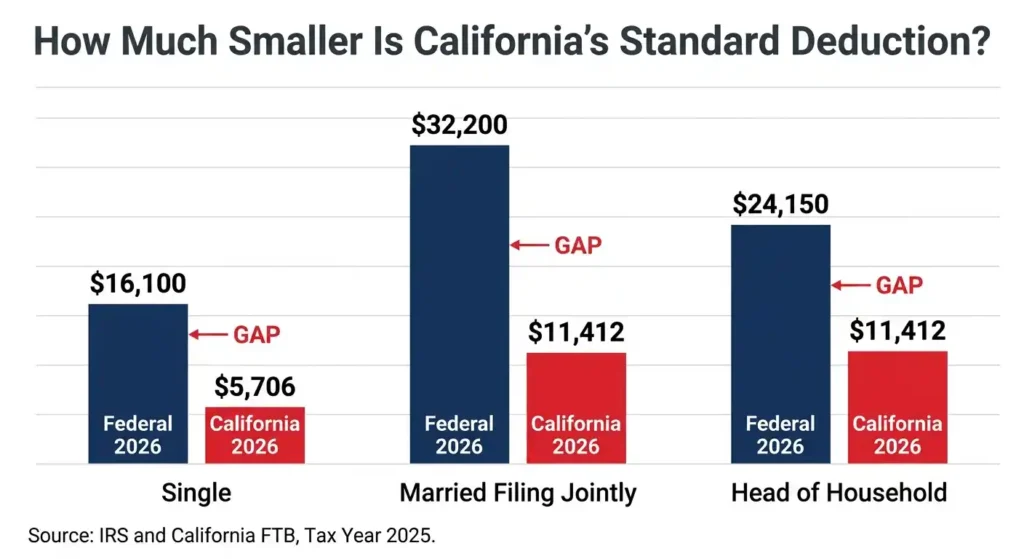

2026 California vs Federal Standard Deduction: Side-by-Side Comparison

California and the federal government use completely different deduction amounts.

| Filing Status | California 2026 | Federal 2026 | Difference |

| Single | $5,706 | $16,100 | $10,394 less |

| Married Filing Jointly | $11,412 | $32,200 | $20,788 less |

| Head of Household | $11,412 | $24,150 | $12,738 less |

California’s deduction is dramatically smaller. A single filer gets $10,394 less protection from California taxes. That means more of your income is taxable on your state return than on your federal return. The IRS standard deduction rules explain the federal side of this calculation in full.

Takeaway: California taxes more of your income because its standard deduction is far smaller than the federal amount.

Why California Uses Different Deduction Rules

California does not follow federal tax law automatically. When Congress changes the federal tax code, California decides separately whether to adopt those changes.

The federal standard deduction jumped significantly in recent years. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently increased the federal deduction. It raised the single filer amount to $16,100 for tax year 2026. California did not adopt that increase. California uses its own lower deduction, adjusted only for inflation by the FTB each year.

California also taxes things the federal government does not. For example, California taxes Social Security income for some earners. California does not conform to the federal Health Savings Account (HSA) exclusion. California also has its own payroll deductions, including the California SDI rate, which further reduces take-home pay beyond what the standard deduction affects. These differences add up fast. They are why your California taxable income often looks higher than your federal taxable income.

Takeaway: California writes its own tax rules. Federal tax changes rarely apply to your California return automatically.

What the California Standard Deduction Actually Does

How the Deduction Lowers Your Taxable Income

The standard deduction blocks a portion of your income from being taxed. Here is the formula.

California Gross Income minus Standard Deduction equals California Taxable Income.

If you earn $65,000 and file as single, your California taxable income becomes $59,294 after the $5,706 deduction. The state then applies its tax rates only to that $59,294 amount. The deduction does not directly lower your tax bill dollar for dollar. It lowers the income that gets taxed first. Then the tax rates apply.

This affects your paycheck withholding too. If your actual deduction situation differs from your employer’s estimate, you may get a refund or owe money at filing. Use a California paycheck calculator to see exactly how your withholding is being estimated.

Takeaway: The standard deduction lowers your taxable income, which then lowers how much tax you owe.

Simple Real-World Examples

Example 1: Single W-2 Employee Earning $60,000

- California Gross Income: $60,000

- Standard Deduction: $5,706

- California Taxable Income: $54,294

- Estimated California Tax (at roughly 6% effective rate): approximately $3,258

Without the deduction, you would owe tax on the full $60,000. The deduction saves this person roughly $342 in California taxes. That is real money back in your pocket.

Example 2: Married Couple Earning $95,000 Combined

- California Gross Income: $95,000

- Standard Deduction: $11,412

- California Taxable Income: $83,588

- Estimated California Tax Savings from Deduction: approximately $1,027

The married couple saves about $1,027 in California taxes by claiming the standard deduction.

Takeaway: For most middle-income Californians, the standard deduction saves between $300 and $1,500 in state taxes annually.

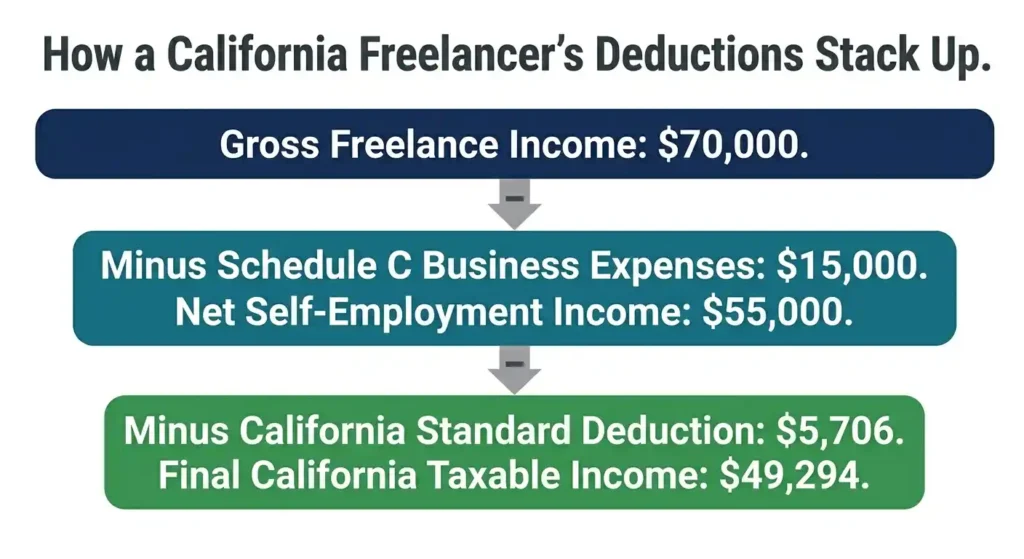

Freelancer and Gig Worker Example

Freelancers often confuse business expense deductions with the standard deduction. They are two different tools used at different stages. If you are weighing 1099 vs W-2 status in California, the tax treatment of deductions is one of the biggest differences to understand.

If you file Schedule C as a self-employed person, you deduct your business expenses directly from your business income. That happens before the standard deduction even enters the picture. After your net self-employment income is calculated, you then apply the standard deduction to reduce your personal taxable income further.

A freelancer earning $70,000 with $15,000 in business expenses has a net Schedule C income of $55,000. Then the $5,706 standard deduction reduces that further to $49,294 of California taxable income. The standard deduction still helps. It just works at a different stage of the calculation.

Takeaway: Freelancers benefit from both business expense deductions and the standard deduction. They are separate tools used at different steps.

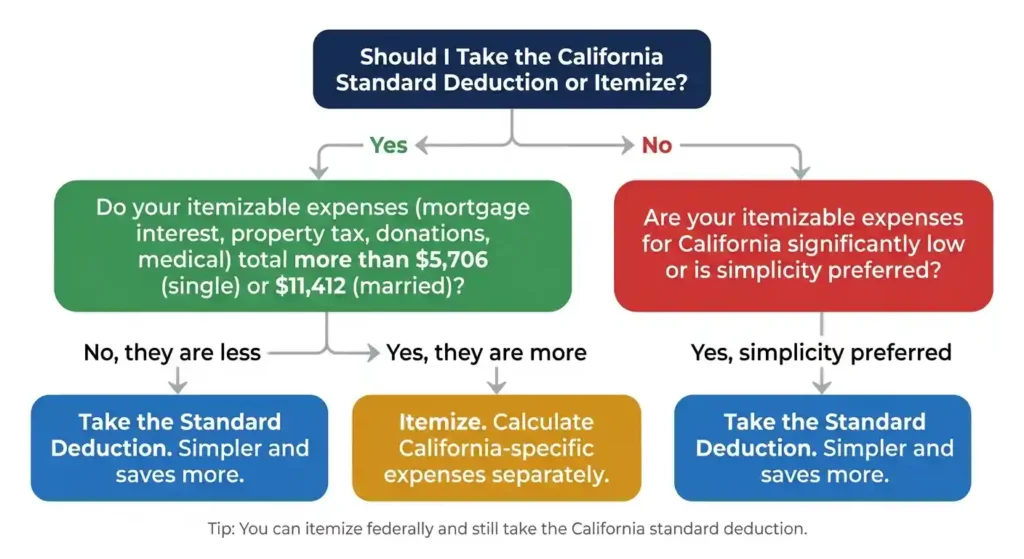

Should You Take the Standard Deduction or Itemize?

When the Standard Deduction Usually Saves More

Most California taxpayers benefit more from the standard deduction. Here is who typically wins with it.

- Renters who have no mortgage interest to deduct

- Young workers in their first jobs without major deductible expenses

- People with straightforward W-2 income and few financial complications

- Anyone whose itemizable expenses total less than $5,706 (single) or $11,412 (married)

The standard deduction is automatic. No receipts, no year-long tracking. You claim it and move on.

Takeaway: Renters and W-2 employees usually come out ahead by taking the California standard deduction.

When Itemizing May Be Better

Some Californians have enough deductible expenses to beat the standard deduction. These are the common situations where itemizing wins.

- Homeowners with significant mortgage interest payments

- People with large charitable donations to eligible organizations

- Individuals with qualifying medical expenses exceeding 7.5% of their AGI

- Those paying substantial property taxes on California real estate

If your total eligible expenses top your standard deduction amount, itemizing saves more money.

Takeaway: Homeowners with big mortgages and high property taxes should always compare itemized totals against the standard deduction before filing.

California Itemized Deduction Rules Most People Miss

California does not allow you to deduct state and local taxes (SALT) paid to other states. That federal SALT deduction concept works differently at the state level.

Also, California does not allow the qualified business income (Section 199A) deduction that federal filers with pass-through income may claim. Business owners who get a federal break from that deduction get nothing from California for it. Your federal and California returns can look very different because of these gaps.

Tax software sometimes displays your federal itemized deduction total and applies it to your California return without flagging the difference. Always verify your California-specific itemized amount separately.

Takeaway: California has its own itemized deduction rules. Federal itemized amounts do not automatically transfer to your California return.

Pro Tip: Itemize Federally While Taking California Standard Deduction

You can itemize on your federal return and take the California standard deduction on your state return at the same time. These are completely independent calculations. If your federal itemized deductions are high but your California-specific expenses fall below $5,706 (single) or $11,412 (married), itemize federally and take the California standard deduction. Many filers assume they must make the same choice on both returns. That assumption costs real money.

Takeaway: Always calculate your California deductions separately from your federal deductions. They can and often should differ.

How the 2026 California Standard Deduction Affects Your Refund

Refund Impact by Income Level

Your refund depends on whether enough tax was withheld during the year. The deduction affects taxable income, but your refund is about the gap between withholding and what you actually owe.

Under $40,000 Income: The standard deduction removes a larger percentage of your taxable income. This group often sees the biggest relative benefit. The 2026 California Earned Income Tax Credit (worth up to $3,756 for tax year 2025) can also boost refunds significantly for earners up to $32,900. You can check eligibility directly on the FTB CalEITC page.

$40,000 to $90,000 Income: This is the middle zone. The deduction helps, but California’s progressive brackets still take a noticeable bite. Withholding accuracy matters most here. Under-withholding is common in this range, especially for people with multiple income sources.

Over $90,000 Income: The standard deduction saves less as a percentage of total income. High earners in California face rates up to 12.3% on income over certain thresholds. Income over $1 million triggers an additional 1% mental health services tax. For this group, itemizing often becomes more valuable. If you earn around six figures, see our detailed breakdown of $100k after tax in California to understand the full picture.

Takeaway: The lower your income, the bigger the relative impact of the standard deduction on your California tax bill.

Why Refunds Sometimes Shrink

The standard deduction is not always the reason your refund shrinks. Here are the real culprits. If your take-home pay also looks unexpectedly low, see why your California paycheck might be smaller than expected for a full breakdown of common causes.

- Payroll withholding set too low on California Form DE-4 (California’s withholding form)

- Side income from freelance work or gig platforms with no tax withheld

- Loss of tax credits from the prior year (like credits that phased out as income grew)

- Changes in filing status after marriage, divorce, or a new dependent

If your income situation changed during the year, the estimates built into withholding may not match your actual tax bill.

Takeaway: A shrinking refund is usually a withholding problem, not a deduction problem. Check your DE-4 every time your income changes.

Quick Refund Estimation Formula

Here is the back-of-envelope calculation I use with clients before filing day.

- Start with your total California wages (W-2 Box 16). If you are hourly, use a gross pay calculator to confirm your annual figure first.

- Subtract your standard deduction ($5,706 single or $11,412 married).

- Apply California’s tax rate for your income level (roughly 4% to 9.3% for most people).

- Compare that estimated tax to your total California withholding (W-2 Box 17).

- The difference is your estimated refund or amount owed.

Credits and other adjustments affect the final number, but this gives you a ballpark before filing day. Once you file, you can track your California tax refund status directly through the FTB.

Takeaway: Estimate your California tax liability before filing to avoid refund shock. The formula takes less than five minutes.

Who Qualifies for the California Standard Deduction?

General Eligibility Rules

Almost every California taxpayer qualifies for the standard deduction. The FTB allows all filing statuses to claim it with no income test or special criteria required.

The main exception is if someone else claims you as a dependent. In that case, your deduction calculation is limited. You also cannot claim the standard deduction if you are married filing separately and your spouse itemizes.

Takeaway: Almost every California filer qualifies for the standard deduction. Dependents and some separately filing spouses are the main exceptions.

Special Rule for Dependents

If your parents or another person claims you as a dependent, you cannot claim the full California standard deduction. Your deduction is limited to the greater of $1,100 or your earned income (wages), up to the regular limit. A student who earned $4,000 gets a $4,000 deduction, not $5,706. Check with whoever claims you before filing.

Takeaway: Dependents get a smaller California standard deduction based on their earned income, not the full amount.

Part-Year Residents and Nonresidents

If you moved into or out of California during 2025, you file Form 540NR. You pay California tax only on income earned while living in California, plus any California-source income earned while living elsewhere. Your standard deduction is prorated based on the percentage of income that is California-source. Residency errors are one of the most common audit triggers the FTB looks for.

Takeaway: Part-year residents and nonresidents use Form 540NR and receive a prorated version of the California standard deduction.

How to Claim the California Standard Deduction Correctly

Which California Tax Forms Use the Deduction

Full-year residents enter the standard deduction on Line 18 of Form 540. Part-year residents and nonresidents use Form 540NR, which involves the California Adjusted Gross Income calculation and proration rules. Dependents use the “Standard Deduction Worksheet for Dependents” in the Form 540 instruction booklet.

Takeaway: Full-year residents use Form 540, Line 18. Part-year residents and nonresidents use Form 540NR. Dependents use the special worksheet.

Filing Through Tax Software

TurboTax, FreeTaxUSA, and H&R Block all handle the California standard deduction automatically. What software does not always do well is flag the federal versus California difference clearly. Always open the California summary screen before submitting and confirm the deduction amount matches the table in this guide.

Takeaway: Tax software calculates the California deduction automatically, but always verify the amount on the California summary screen before you file.

Common Filing Mistakes That Cost Californians Money

These are the errors I see most often in 8 years of reviewing California returns.

- Wrong filing status: Using “Single” when “Head of Household” applies. Head of Household gets $11,412 instead of $5,706. That is a $5,706 mistake that costs real money.

- Residency errors: Claiming a full-year deduction when you only lived in California part of the year.

- Mixing federal and California rules: Applying the federal $16,100 deduction to your California return. California only allows $5,706 for single filers.

- Dependent deduction errors: Claiming the full standard deduction as a dependent instead of the limited amount from the worksheet.

Each mistake either underpays or overpays California taxes. The FTB bills you for underpayments. Overpayments are just a free loan to the state.

Takeaway: Double-check your filing status and residency first. These two errors cause the most expensive standard deduction mistakes.

Pro Tip: Compare California Itemized Totals Before Submitting

Before you click submit, add up your California-eligible itemized deductions: mortgage interest, property taxes, charitable donations, and medical expenses above 7.5% of your AGI. If that total beats $5,706 (single) or $11,412 (married), itemize. If it falls short, take the standard deduction. This five-minute check has saved clients several hundred dollars in a single year.

Takeaway: Always manually compare your California itemized total against the standard deduction before filing. It takes five minutes and can save you real money.

Why California Taxable Income Looks Different from Federal Income

Separate Federal and California Tax Systems

California and the federal government calculate taxable income completely independently. Your federal return may reflect HSA contributions, Section 199A deductions, or a higher standard deduction that California simply ignores. Your California taxable income is almost always higher than your federal taxable income, even if your gross income is identical. The FTB also adjusts brackets and deductions for inflation separately from the IRS.

Takeaway: California taxable income is almost always higher than federal taxable income because California does not adopt most federal deduction increases.

Common TurboTax and Refund Confusion

People see a large federal refund and expect a proportional California refund. It rarely works that way. Your federal return benefits from the $16,100 single standard deduction. Your California return only gets $5,706. That $10,394 gap is fully taxable in California. At a 6% rate, that gap alone costs about $624 more in California taxes than most people expect. California also does not give taxpayers over 65 the extra $1,600 federal senior deduction.

Takeaway: Expect your California taxable income and tax bill to be higher than your federal amounts. That is normal. It is not a software error.

Reality Check: The Biggest California Deduction Myths

Myth 1: A lower standard deduction always means higher taxes. Not necessarily. Credits like CalEITC can offset the impact for lower-income earners.

Myth 2: The standard deduction is always worse than itemizing. For most Californians, especially renters and people without large mortgages, the standard deduction is the better option.

Myth 3: California’s tax brackets work the same as federal brackets. They do not. California has nine rates from 1% to 12.3%, with different income thresholds than the federal system.

Takeaway: California taxes are complex but manageable once you separate the state rules from federal rules in your mind.

California Tax Brackets and Deduction Interaction

How Progressive Tax Brackets Work

California uses a progressive tax system. You pay a lower rate on the first portion of income and higher rates only on income above certain thresholds. For 2025 (filed in 2026), California income tax brackets range from 1% up to 12.3% on income above $625,369 for single filers. Income over $1 million triggers an additional 1% surcharge. Most middle-income Californians pay effective rates in the 4% to 7% range, not the headline top rate.

Takeaway: California’s tax rates are progressive. You pay higher rates only on the income above each threshold, not on your total income.

Example Tax Bracket Calculation for a Middle-Income Californian

Here is a realistic example. A single Californian earns $75,000 from a W-2 job in 2025.

- Start with $75,000 gross income.

- Subtract $5,706 standard deduction.

- California taxable income: $69,294.

- The first $10,756 is taxed at 1% = $108.

- The next $15,481 (up to $26,237) at 2% = $310.

- The next $6,978 (up to $33,215) at 4% = $279.

- And so on up through the brackets.

The total California income tax on $69,294 is roughly $3,000 to $3,500, an effective rate of about 4.3% to 5%. That is far lower than the 9.3% headline rate people fear. If you want to see exactly how these calculations show up line by line, learning how to read a California pay stub makes the numbers much clearer.

Takeaway: Most Californians pay an effective California tax rate of 4% to 7%, far below the top marginal rate people often fear.

Hidden Situations Most Articles Ignore

F1 Visa Students and International Taxpayers

F1 students are typically treated as federal nonresident aliens for their first five years and use Form 1040-NR without a standard deduction. However, California has its own residency rules. If California classifies you as a state resident based on your domicile and intent to stay, you may qualify for the California standard deduction even while filing as a federal nonresident. California also does not honor most federal tax treaties, which can create large gaps between state and federal tax bills.

Takeaway: International students should consult a tax professional familiar with both California residency rules and federal treaty provisions before filing.

Married Filing Separately in California

California is a community property state. Most income earned during marriage must be split 50/50 between spouses for tax purposes, even if only one spouse earned it. Each spouse gets the $5,706 standard deduction. But the income-splitting requirement means both spouses often report similar taxable income regardless of actual earnings. Also, if one spouse itemizes, the other must itemize too. This filing status rarely saves taxes in California.

Takeaway: Married filing separately in California is complicated by community property rules. Most couples save more by filing jointly.

Remote Workers Moving Into or Out of California

California taxes all income earned while you were a resident, plus California-source income earned before you moved in. If you moved out mid-year, the FTB may still claim taxes on income connected to California work done while you were a resident. Remote workers doing California-based work from another state have faced FTB tax claims. Your standard deduction as a part-year resident is prorated. Getting your move dates exactly right on Form 540NR is critical.

Takeaway: California aggressively taxes income connected to the state. Moving dates must be documented carefully for part-year residents.

Seniors and Federal Bonus Deduction Differences

Federal law gives taxpayers 65 or older an extra $1,600 added to their standard deduction (making the total $17,700 for a single senior in 2026). California does not provide this bonus. A 70-year-old filing single in California still gets just $5,706. California offers a small senior exemption credit ($158 for 2025), but it is far smaller than the federal bonus deduction seniors receive.

Takeaway: California does not give seniors an extra standard deduction. A small senior exemption credit partially compensates, but the gap is significant.

Self-Employed and Side Hustle Workers

If you run a business in California, deduct all legitimate Schedule C expenses first. These reduce net self-employment income before the standard deduction applies. California generally conforms to federal Schedule C rules. After Schedule C, the standard deduction still reduces your overall taxable income. But self-employed people must also make quarterly estimated payments. A large deduction at filing time does not prevent FTB penalties for under-withholding throughout the year. Understanding your full California payroll tax obligations is essential if you pay yourself or run a team.

Takeaway: Self-employed Californians benefit from both business deductions and the standard deduction, but quarterly estimated payments are a separate and equally important obligation. If you do not have a retirement plan through an employer, the CalSavers mandate may apply to you and can also affect your taxable income planning.

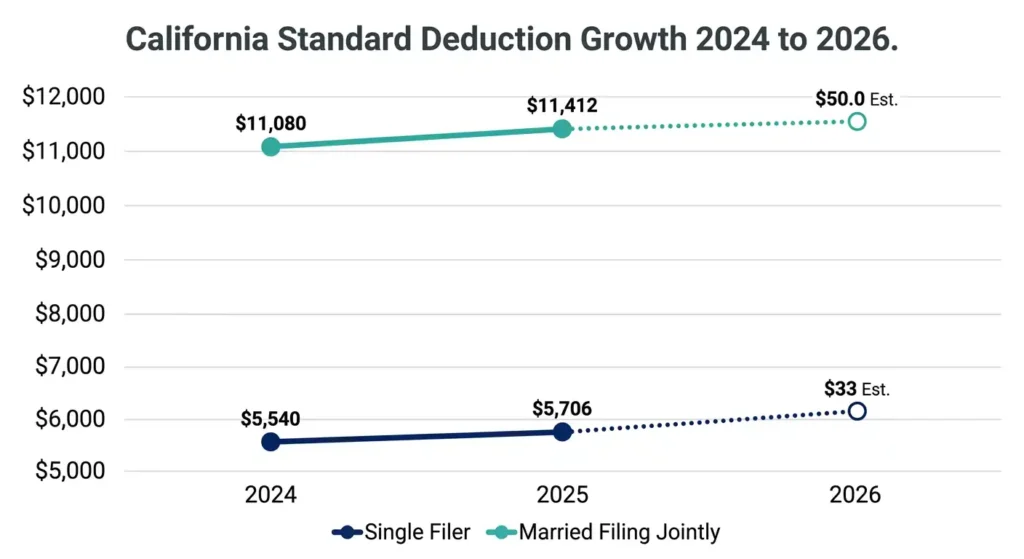

2026 California Standard Deduction Historical Trends

2024 vs 2025 vs 2026 Deduction Changes

California adjusts its standard deduction for inflation each year. The changes are modest.

| Tax Year | Single Filer Deduction | Married Filing Jointly |

| 2024 | $5,540 | $11,080 |

| 2025 (filed 2026) | $5,706 | $11,412 |

| 2026 (estimated) | Expected modest increase | Expected modest increase |

The increase from 2024 to 2025 was $166 for single filers, saving roughly $10 in taxes at a 6% effective rate. The adjustments are real but rarely change your filing strategy.

Takeaway: California increases its standard deduction slightly each year for inflation, but the increases are modest and rarely change filing strategy.

Could California Increase the Deduction Significantly in 2027?

A bill introduced in February 2026 (AB 2591) proposes allowing taxpayers to elect a standard deduction equal to the federal poverty level starting July 1, 2027. For a single person, that could mean roughly $15,000, far above today’s $5,706. The bill is in early stages and may not pass. For 2026 filing, the current amounts are firm. Watch for FTB announcements in late 2026 for any 2027 changes.

Takeaway: California’s deduction could increase significantly after 2027 if pending legislation passes, but for 2026, the current amounts are fixed.

Deep-Dive FAQ

What is the California standard deduction for 2026?

$5,706 for single filers and married filing separately. $11,412 for married filing jointly, head of household, and qualifying surviving spouses.

Is the California standard deduction different from the federal deduction?

Yes. The federal deduction is $16,100 (single) and $32,200 (married jointly) for 2026. California’s amounts are $5,706 and $11,412. California does not adopt federal increases automatically.

Should I itemize or take the standard deduction in California?

Add up your California-eligible itemized expenses. If they exceed $5,706 (single) or $11,412 (married), itemize. If not, take the standard deduction.

Why is my California taxable income higher than my federal taxable income?

California uses a smaller standard deduction and does not conform to federal deductions like HSA exclusions or Section 199A, so more of your income is taxable at the state level.

Can freelancers take the California standard deduction?

Yes. Business expenses reduce net Schedule C income first, then the standard deduction reduces taxable income further. They are separate steps.

Do dependents get a California standard deduction?

Yes, but limited. Dependents deduct the greater of $1,100 or their earned income, up to $5,706. A student earning $3,500 gets a $3,500 deduction.

Does California follow IRS deduction rules?

Not automatically. California adopts federal tax changes selectively, which is why state and federal taxable income amounts routinely differ.

How much money does the California standard deduction save?

At a 6% effective rate, roughly $342 for single filers and $685 for married couples. Actual savings depend on your tax bracket.

Can I itemize federally and take the California standard deduction?

Yes. Federal and California returns are independent. You can itemize federally and take the California standard deduction on the same return.

What happens if I move into California mid-year?

You file Form 540NR as a part-year resident. Your deduction is prorated to California-source income, and you owe state taxes on all income earned after your move-in date.

Which California tax form includes the standard deduction?

Form 540, Line 18 for full-year residents. Form 540NR for part-year residents and nonresidents. Dependents use the worksheet in the Form 540 instructions.

Does California allow extra standard deductions for seniors?

No. California does not offer the federal $1,600 senior bonus deduction. A small senior exemption credit ($158 for 2025) partially offsets the gap.

Final Summary: What Most Californians Should Actually Do

Confirm your filing status first. Head of Household filers get $11,412 instead of $5,706. Many people miss this status when they qualify.

Compare your California itemized expenses separately from your federal ones. The five minutes you spend on this can save you $300 to $600.

Expect your California taxable income to be higher than your federal amount. That is by design. California’s system taxes more income.

If you are self-employed, make quarterly estimated payments. The deduction helps at filing time, but it does not cancel under-withholding penalties the FTB charges throughout the year.

Finally, verify your tax software’s California deduction number matches the table in this guide before you submit. If you want to model your full annual tax liability before filing, the California annual salary calculator can give you a fast estimate based on your income and filing status.

You now have everything you need to file your California taxes with confidence in 2026.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.