The CA SDI rate for 2026 is 1.3% of all gross wages, with no taxable wage ceiling. Every covered California employee pays this rate on every dollar earned, funding both Disability Insurance and Paid Family Leave.

After eight years working directly with HR teams and payroll systems across California, I have seen firsthand how the Senate Bill 951 wage cap removal blindsided high earners, turning a $1,602 annual cap-limited deduction into $3,250 or more overnight. Use our California paycheck calculator to see exactly how SDI affects your take-home pay.

High earners and multi-job workers carry the biggest burden here. Always verify your deduction math and consult a tax professional for your situation.

Free California SDI Tool

See Exactly How Much SDI Is Cut From Your Paycheck

The 2026 SDI rate is 1.3% — but the dollar amount depends on your salary and pay frequency. Enter your numbers and see it instantly.

🧮 Calculate My Exact SDI Deduction2026 rate confirmed · EDD-verified · No sign-up needed

CA SDI 2026 At a Glance: The Quick Facts You Need

Here is everything in one place. No hunting required.

| Detail | 2026 Value |

|---|---|

| SDI withholding rate | 1.3% |

| Taxable wage ceiling | None |

| Maximum weekly benefit | $1,765 |

| Who pays SDI | Employees (withheld from paycheck) |

| What it funds | Disability Insurance and Paid Family Leave |

The formula is simple. Take your gross wages and multiply by 0.013. That is your SDI deduction for that pay period. If you earn $1,000 in a week, you pay $13.00. It shows up on your pay stub as CASDI, SDI, or VPDI depending on your payroll software. SDI is just one piece of the bigger California payroll taxes picture every employee should understand.

Takeaway: Gross wages x 1.3% = your CA SDI deduction every single pay period.

What Is the Official 2026 CA SDI Rate?

The California Employment Development Department (EDD) sets the SDI contribution rate each year. For 2026, the rate increased from 1.2% to 1.3%, effective January 1, 2026.

This is a statewide rate. Every covered employer uses the exact same number. There is no negotiation and no regional difference. The EDD confirms this rate in its annual General Release Letter, published December 31, 2025.

What makes 2026 different from older years is the wage cap. California removed the taxable wage ceiling starting in 2024. Before that, SDI only applied to wages up to a set limit. Now it applies to every dollar you earn, all year long.

Takeaway: The official 2026 SDI rate is 1.3%, set by the EDD, with zero wage ceiling.

Is There a CA SDI Wage Limit in 2026?

No. There is no wage limit in 2026. This is the third straight year with no maximum contribution cap.

Senate Bill 951 changed everything. Before 2024, the SDI tax stopped once you hit the annual wage ceiling. A high earner might have stopped seeing SDI deductions in October or November. That no longer happens. If you earn $500,000 a year, you pay SDI on all $500,000. You can read the full text of Senate Bill 951 on the California Legislative Information site.

I personally watched multiple HR teams scramble when this change hit. High earners were calling payroll departments demanding to know why the “error” was not fixed. It was not an error. It was the new law.

Takeaway: Senate Bill 951 removed the wage cap permanently. SDI applies to 100% of your wages in 2026.

How Much CA SDI Will You Pay in 2026?

Let me show you exactly what this looks like in real paychecks.

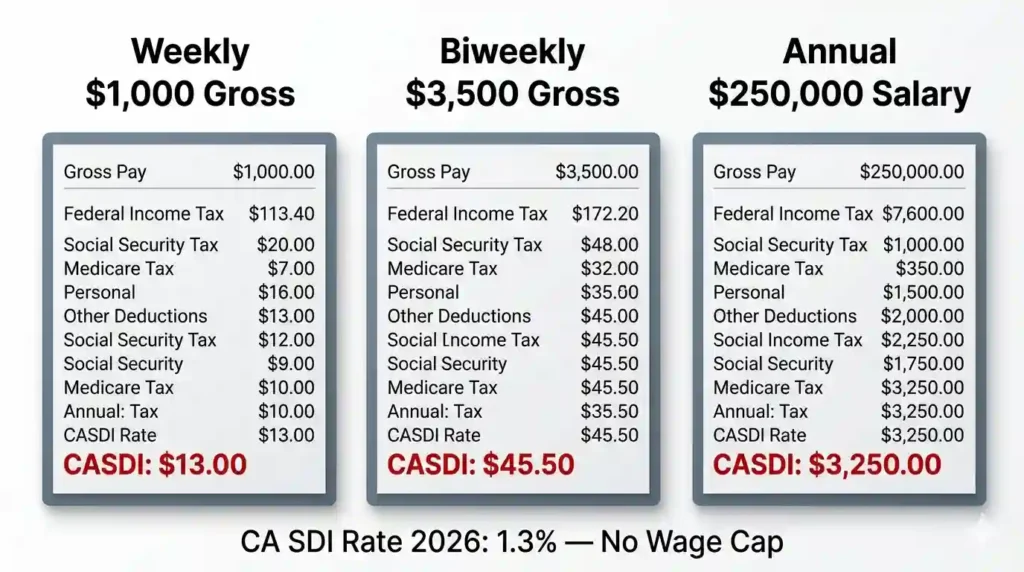

Weekly Paycheck Example: $1,000 Gross

- Gross wages: $1,000

- SDI deduction: $1,000 x 1.3% = $13.00

- Your pay stub will show: CASDI $13.00

That $13 funds your right to collect disability benefits or paid family leave if you ever need it. Think of it as very affordable insurance.

Biweekly Paycheck Example: $3,500 Gross

- Gross wages: $3,500

- SDI deduction: $3,500 x 1.3% = $45.50

- Annual total (26 pay periods): approximately $1,183

Most employees on a biweekly schedule barely notice the deduction at this income level. The shock comes at higher incomes.

High-Income Example: $250,000 Salary

- Annual SDI deduction: $250,000 x 1.3% = $3,250

- Under the old capped system (2022): 1.1% x $145,600 wage base = approximately $1,602 max per year

- Difference: over $1,600 more per year for a $250,000 earner

That is not a typo. The removal of the wage cap created a massive change for high earners. In my experience, this is the single biggest source of payroll confusion I have seen in the past three years.

Takeaway: The higher your income, the more dramatically your SDI deduction changed after 2024.

Why Your CA SDI Deduction Increased

You are not imagining it. Your deduction went up. There are two reasons.

Reason 1: The Rate Increased from 1.2% to 1.3%

The EDD adjusted the contribution rate upward. The SDI fund needs more revenue to pay growing disability and family leave claims. The rate has risen steadily. It was 1.1% in 2022, 1.2% in 2025, and 1.3% in 2026. You can verify current and prior year rates directly on the EDD Contribution Rates and Benefit Amounts page.

Reason 2: The Wage Cap Is Gone

This is the bigger deal. Many employees never hit the old wage ceiling. But if you did, you used to get a “holiday” from SDI deductions partway through the year. That break no longer exists. SDI now runs from your first paycheck to your last, every single year.

What I have found is that most employees understand the rate increase once I explain it. What takes longer to accept is the idea that high earners no longer get a mid-year reprieve. That is just the new reality under California law. If you are also wondering about other reasons your take-home has dropped, read our guide on why your California paycheck is so low.

Takeaway: Your deduction increased because both the rate and the wage scope expanded starting in 2024.

What Does CA SDI Mean on Your Pay Stub?

Your pay stub might show different labels depending on your employer’s payroll system. Here is what they all mean:

- CASDI = California State Disability Insurance (most common)

- SDI = State Disability Insurance (same thing, shorter label)

- VPDI = Voluntary Plan Disability Insurance (employer-run alternative plan, same legal protection)

CASDI and SDI are two labels for the same mandatory state withholding. VPDI appears when your employer runs an EDD-approved private disability plan instead of the standard state plan. The deduction purpose is the same, but the plan administration differs.

One thing I always tell new employees: do not confuse this with California state income tax. They are completely separate deductions with separate purposes and separate line items on your pay stub. If you want a full breakdown of every line on your check, our guide on how to read a California pay stub in 2026 walks through each field step by step.

Takeaway: CASDI, SDI, and VSDI on your pay stub all mean the same California disability contribution.

What Benefits Does SDI Actually Fund?

Your 1.3% SDI contribution funds two California programs.

Disability Insurance (DI) pays you when you cannot work due to illness, injury, or pregnancy. You can receive between 60% and 90% of your weekly wages, depending on your income level. The maximum weekly benefit in 2026 is $1,765.

Paid Family Leave (PFL) pays you when you need to bond with a new child or care for a seriously ill family member. The same 60% to 90% wage replacement applies, with the same $1,765 weekly maximum.

Many employees think PFL is a separate deduction. It is not. PFL is funded through the same SDI withholding. You do not pay extra for it. The EDD manages both programs from the same fund. You can review full eligibility details on the EDD Paid Family Leave official page.

Takeaway: Your SDI deduction covers both Disability Insurance and Paid Family Leave with no extra cost.

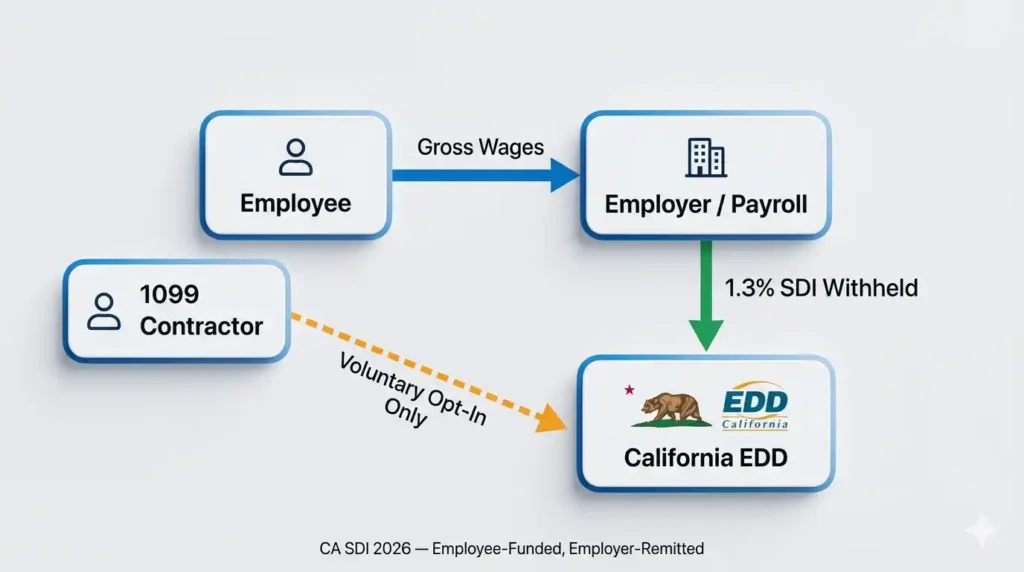

Who Pays CA SDI in 2026?

The employee pays SDI. Not the employer. The employer withholds it from your paycheck and sends it to the EDD. But the money comes out of your gross wages.

Here is how the roles break down:

- Employee: Contributes 1.3% of wages, has no choice in the matter

- Employer: Withholds the amount from payroll and remits it to the EDD

- 1099 contractors: Not automatically covered. Must elect voluntary coverage separately.

If you are a freelancer or gig worker, you do not automatically pay into SDI. That also means you cannot automatically claim SDI benefits. Some self-employed Californians choose to opt in through the EDD elective coverage program. But most do not know it exists. For a full comparison of how tax obligations differ, see our 1099 vs W-2 guide for California workers.

Takeaway: W-2 employees pay SDI through automatic paycheck withholding. Freelancers must opt in voluntarily.

CA SDI vs California State Income Tax: What Is the Difference?

These are two completely different deductions. I see employees mix them up constantly.

California State Income Tax is based on your income bracket. It funds general California government services. The amount varies widely based on your earnings and allowances. See the full California tax brackets for 2026 to understand how your income tier affects withholding.

CA SDI is a flat 1.3% of all wages. It funds only disability and family leave programs. The same rate applies to everyone, regardless of income. Your California state income tax withholding, on the other hand, is controlled by how you fill out the California DE 4 form.

Both appear on your pay stub. Both reduce your take-home pay. But they serve completely different purposes and go to completely different places. California uses a specific calculation method for state income tax withholding that differs from the federal system. See how California Method B exact calculation works if you want to verify your state income tax deduction independently.

Takeaway: SDI and California income tax are separate. SDI is a flat 1.3%. Income tax varies by bracket.

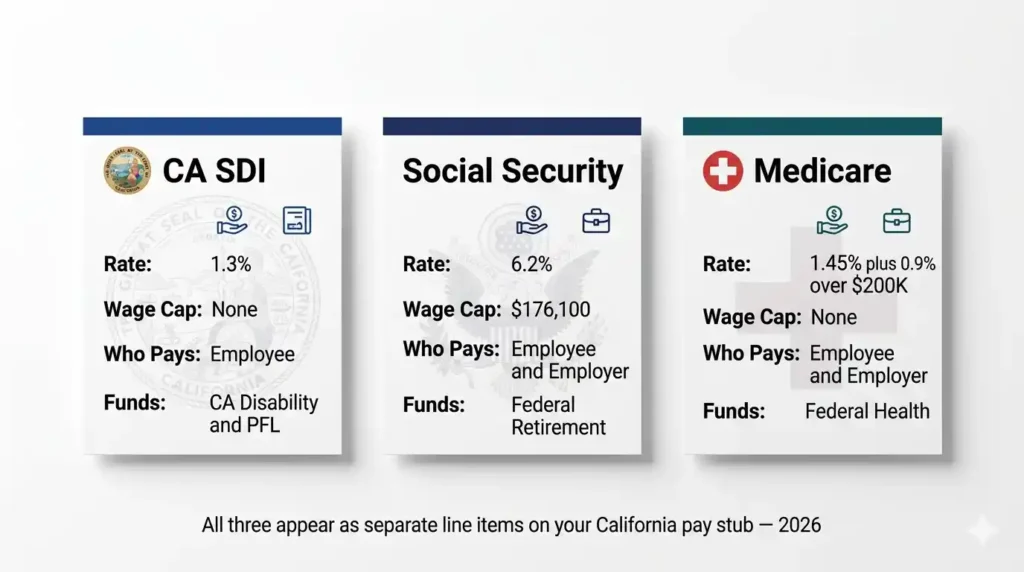

CA SDI vs Social Security and Medicare

Social Security and Medicare are federal payroll taxes. SDI is a state payroll tax. They do not overlap.

Here is a quick side-by-side:

| Feature | CA SDI | Social Security | Medicare |

|---|---|---|---|

| Level | State (California only) | Federal | Federal |

| 2026 rate | 1.3% | 6.2% | 1.45% (plus 0.9% over $200K) |

| Wage cap | None | $176,100 | None |

| Who benefits | California workers | All U.S. workers | All U.S. workers |

You pay all three from the same paycheck. They show up as separate line items. None of them replaces the others.

Takeaway: SDI, Social Security, and Medicare are three separate deductions with three separate purposes.

SDI vs Paid Family Leave (PFL)

Why Employees Expect a Separate PFL Line

Many new employees come from other states where disability and family leave are funded separately. They look at their California pay stub and ask where the PFL deduction is. It is not missing. It is already included.

How the Unified Funding Actually Works

PFL is funded entirely through SDI contributions. The EDD pulls from the same fund to pay both disability claims and family leave claims. You never see a separate PFL deduction because there is none. Your single 1.3% SDI withholding covers both programs from day one.

Takeaway: PFL is not a separate tax. It is funded through your existing SDI contribution.

The Biggest Myths About CA SDI in 2026

Let me bust the four myths I hear most often.

Myth 1: “There Is Still a Wage Cap”

Why This Myth Refuses to Die

Outdated articles from 2022 and 2023 still rank well in search results. Many employees read them and assume the old wage ceiling still applies. It does not. The cap was permanently removed starting January 1, 2024.

What the Rule Actually Is

If you read that SDI stops at $153,164 or any similar number, that article is describing an old year. There is no wage ceiling in 2026. SDI applies to every dollar you earn, full stop.

Myth 2: “The Employer Pays SDI”

Where This Confusion Comes From

Employers handle payroll. They send the SDI payment to the EDD. So employees sometimes assume the employer is footing the bill. That is not what happens.

The Real Story

Your employer withholds the money from your gross wages before you ever see it. The money was yours. The employer is simply the collection agent. The cost falls entirely on you.

Myth 3: “SDI and PFL Are Separate Taxes”

Why It Looks That Way

Some employees expect to see two separate deduction lines. One for SDI. One for PFL. When they only see one line, they assume PFL is not being funded.

The Actual Structure

Paid Family Leave is funded through the same SDI withholding. You pay one contribution. You get access to both programs. Your pay stub will never show a separate PFL deduction line.

Myth 4: “CA SDI Is Optional”

The Opt-Out Myth

Some employees believe they can refuse SDI withholding or request a refund of contributions. This idea circulates in online forums and causes real confusion during onboarding.

Why You Cannot Opt Out

If you are a W-2 employee under a covered California employer, SDI is mandatory by law. The only recognized exception is employees covered under an EDD-approved Voluntary Plan Disability Insurance program. That decision belongs to your employer, not you.

Takeaway: All four of these myths cause real payroll confusion. The facts above are the correct 2026 rules.

VPDI vs SDI: The Payroll Topic Most Articles Ignore

What Is VPDI?

The Alternative Plan Most Employees Never Hear About

VPDI stands for Voluntary Plan Disability Insurance. It is an employer-sponsored alternative to the standard EDD state plan. Large companies can apply to the EDD for approval to run their own disability insurance program.

If your pay stub says VPDI instead of CASDI, your employer has one of these plans. You are still covered. The benefits must be at least equal to standard SDI under California law. Your employee rights are fully protected.

Can VPDI Rates Be Different?

How Employer Plans Are Structured

VPDI rates can differ from the standard 1.3% rate. Employers with strong claims histories and favorable actuarial data sometimes negotiate lower employee contribution rates. In some plans the employer absorbs a portion of the cost entirely.

The key protection is benefit equivalency. Whatever the contribution structure looks like, your disability and family leave benefits cannot be less generous than what the state SDI plan provides. If you are also weighing whether to itemize vs take the standard deduction when filing, see how the California standard deduction for 2026 compares to itemizing.

Multiple Employers and Excess Withholding Issues

The Two-Job Trap

Each employer withholds SDI separately. They do not coordinate with each other. If you earn enough between two employers, you might overpay your SDI for the year. This happens silently and most employees never notice it.

How to Get Your Money Back

Excess SDI withholding is refundable. You claim it on your California state tax return using FTB Form 540. The FTB processes the overpayment as a credit. What I have found is that people with two W-2 jobs often do not realize they overpaid until a tax professional catches it during filing season. Always check your SDI totals if you hold multiple California jobs. You can check your California tax refund status directly through the FTB once your return is filed.

Takeaway: VPDI is a legal alternative to state SDI. Two-job workers may overpay and can claim a refund on Form 540.

Do You Qualify for SDI Benefits After Paying In?

Does Paying SDI Automatically Qualify You?

Wage History Requirements

Paying SDI does not automatically mean you can collect benefits. You must meet specific requirements. The EDD checks your base period wages before approving any claim.

What the Base Period Actually Means

The base period is typically the 12 months ending five months before your claim date. You need at least $300 in covered wages during that window. Many new hires get surprised when they cannot file because they just started a job. Wage history must exist in the EDD system first.

To qualify for Disability Insurance, you need:

- A valid medical condition that prevents you from working

- Wages in the prior 5 to 18 months (your base period)

- Earned at least $300 in wages during your base period

- A doctor’s certification of your disability

Takeaway: You must have prior California wages and a certified medical condition to receive SDI benefits.

How Much Does SDI Pay in 2026?

Benefit Calculation and Weekly Amounts

How the 60% to 90% Range Works

Your weekly benefit is between 60% and 90% of your average weekly wages. Lower earners receive the higher percentage. The maximum any claimant can receive is $1,765 per week in 2026. If you are a lower-income worker, also check whether you qualify for the California Earned Income Tax Credit in 2026 to further reduce your tax burden.

A Simple Real-World Example

If your average weekly wages are $1,500, you might receive around $900 to $1,050 per week on SDI. The EDD calculates this using your highest quarter of earnings in the base period. For most workers, SDI replaces a meaningful portion of lost income without covering it fully.

Takeaway: SDI pays 60% to 90% of your wages, up to $1,765 per week in 2026.

Real Problems Employees Face When Filing SDI Claims

After eight years watching people navigate the EDD system, here are the issues I see most often.

Payroll Errors That Trigger SDI Problems

“I Paid SDI But Got Denied”

Some small employers forget to deduct SDI or deduct it under the wrong worker classification. When you file a claim, the EDD finds no wages on file. Your claim gets delayed or denied. Always verify your CASDI deductions appear on every pay stub from day one.

Wrong Worker Classification

Misclassified workers are one of the most painful SDI situations I encounter. If your employer treated you as a 1099 contractor but should have classified you as a W-2 employee, you may have zero covered wages in the EDD system. Fixing this requires an employment determination filing and takes months. Our worker classification resources explain how California defines employees vs contractors under the ABC test.

Why Employees Panic During SDI Claims

Delayed Certifications and Processing Confusion

The EDD processes claims manually. Delays are common. Employees who expect a fast approval often panic when they hear nothing for two to three weeks. The certification window is strict. Missing it can pause your benefits entirely.

Benefit Calculation Misunderstandings

Many employees expect to receive their full salary on SDI. They do not. The 60% to 90% replacement rate surprises people who did not read the rules beforehand. This is one of the most common calls HR teams receive during open enrollment season.

W-2 to 1099 Transition Confusion

Contractor Eligibility Confusion

An employee goes on contract right before needing disability leave. Suddenly they have no SDI coverage. If you are considering a contractor switch, understand the timeline before making the move. There is no retroactive coverage once you leave W-2 status.

Gig Worker Limitations

Gig workers and platform contractors in California face a unique trap. They may assume AB 5 protections give them SDI access. In practice, most platform workers still need to elect voluntary coverage separately through the EDD to be protected. The California ABC test guide for 2026 explains exactly how the state determines whether you are an employee or independent contractor.

Insider Insight: What HR Teams See Every January

The Real Pattern Nobody Talks About

Here is something I have never seen written anywhere else. Every January, HR teams at mid-size California companies receive a spike in payroll complaints. In my experience, a large share of those complaints come from employees who had a raise in the prior year. Their SDI deduction jumped not just because of the rate increase but because their base wages grew. They see a bigger deduction and assume something broke. Nothing broke. Their earnings went up and their SDI went up with it.

The One Check That Saves Hours of Back-and-Forth

Pull the prior December pay stub and the first January pay stub side by side. Calculate 1.3% of each gross pay figure. If the numbers match, the system is working correctly. This single two-minute check resolves most employee complaints before they become HR tickets.

Takeaway: SDI claim problems usually trace back to employer setup errors, missing wage history, or earnings growth misunderstood as a payroll error.

Employer and HR Compliance Guide for 2026

If you run payroll or manage HR, here is your checklist for 2026. For a broader view of all California employer obligations this year, browse the full payroll compliance and reporting category.

What Employers Must Do in 2026

Core Withholding Requirements

- Update payroll software to use the 1.3% SDI rate effective January 1, 2026

- Confirm no wage ceiling is being applied in your system

- Verify all W-2 employees are enrolled in SDI withholding

- Check that SDI amounts appear correctly on W-2 Box 14 or Box 19

- Remit withheld SDI funds to the EDD on schedule

Every one of these steps needs a manual verification. Do not rely on your payroll vendor to catch every setting automatically.

Common Employer Mistakes

The Four Errors I See Most Often

- Payroll systems still using a wage cap that no longer applies

- Employees misclassified as contractors who should be W-2 workers

- SDI labeled incorrectly on pay stubs, causing employee confusion

- Vendors who did not push the 2026 rate update automatically

The misclassification issue is particularly costly. An audit that finds improperly classified workers can trigger back SDI liability plus penalties for every pay period the error existed. Review the full list of California pay stub codes in 2026 to ensure your labels and deduction lines are set up correctly.

Pro Tip for Payroll Teams

The January Audit That Saves the Whole Year

Audit your first January paychecks every year. Pull ten random employee records and manually verify the SDI deduction equals gross wages multiplied by 1.3%. If any record shows a different calculation or a deduction that stopped mid-year, you have a system configuration problem that needs immediate correction.

What I have found is that even major payroll platforms occasionally carry forward outdated wage cap settings until someone manually checks. That five-minute audit protects your company from an EDD compliance notice months later.

Takeaway: Audit your first 2026 payroll run to confirm the 1.3% rate and no wage cap are both applied correctly.

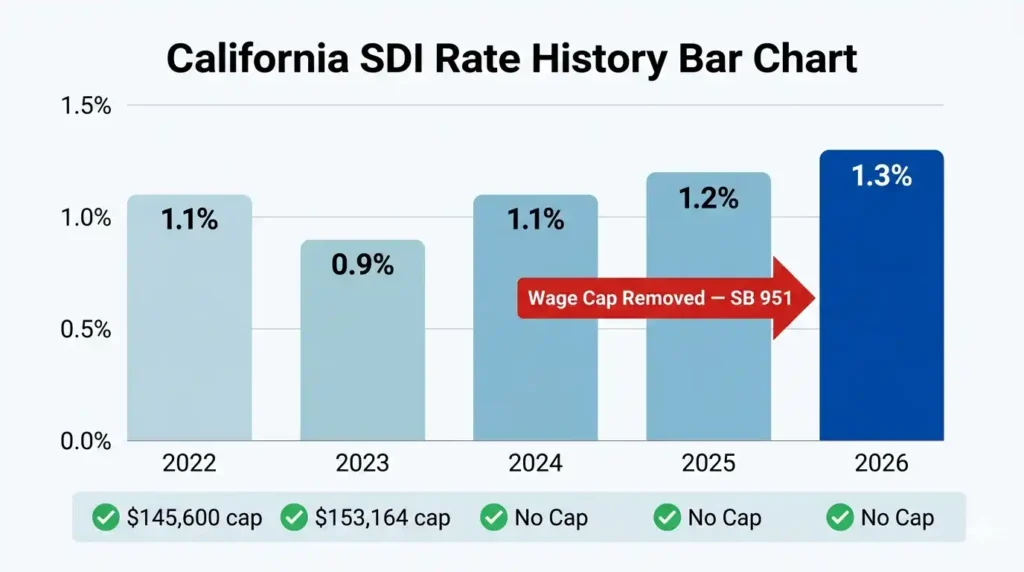

Historical CA SDI Rates: How We Got to 1.3%

Seeing the trend helps you understand where things are going.

| Year | SDI Rate | Wage Cap |

|---|---|---|

| 2022 | 1.1% | $145,600 |

| 2023 | 0.9% | $153,164 |

| 2024 | 1.1% | None (SB 951) |

| 2025 | 1.2% | None |

| 2026 | 1.3% | None |

The 2023 rate looks lower, but that was temporary. The real shift came in 2024 when the wage cap disappeared. That single change affected high earners far more than any rate adjustment ever did.

Senate Bill 951 was signed to make SDI more equitable. Low and middle-income workers now receive a higher wage replacement percentage. The trade-off is that high earners contribute much more than before. Browse our paycheck basics guides to understand how all California deductions fit together.

Takeaway: The rate has increased steadily since 2024, and the wage cap removal was the biggest structural change in SDI history.

Frequently Asked Questions About CA SDI Rate 2026

What is the CA SDI rate for 2026?

The CA SDI rate for 2026 is 1.3% of gross wages. There is no maximum wage limit. The rate applies to every dollar earned by covered California employees.

Is there a CA SDI wage limit in 2026?

No. Senate Bill 951 eliminated the taxable wage ceiling starting January 1, 2024. The no-cap rule continues in 2026.

Why did my CASDI deduction increase?

Two reasons. The rate went up from 1.2% to 1.3%. Also, if you are a high earner, you no longer stop paying SDI mid-year because the wage cap is gone.

Is CA SDI refundable on taxes?

SDI withheld from California wages may be deductible on your federal income tax return as a state and local tax, but only if you itemize deductions on IRS Schedule A. It is not an automatic deduction for everyone. If you overpaid because you had two employers, claim the excess as a credit on your California Form 540. Consult a tax professional for your specific situation.

Do freelancers pay CA SDI?

Not automatically. Independent contractors are not covered unless they elect voluntary coverage through the EDD. Check the EDD website for elective coverage options.

What does VPDI mean on a paycheck?

VPDI means Voluntary Plan Disability Insurance. Your employer runs an EDD-approved private disability plan instead of the standard state SDI plan. Benefits must be at least equal to state SDI.

Is SDI taxable federally?

SDI contributions you pay may be deductible as a state and local tax on federal Schedule A, but only if you itemize. SDI benefits you receive are generally not subject to federal income tax unless the EDD determines they are replacing unemployment compensation. Tax treatment depends on individual circumstances. Always verify with a licensed tax professional.

Can you opt out of CA SDI?

No, not for standard W-2 employees under covered employers. SDI is mandatory. The only exception is workers under an approved VPDI plan.

Why does my pay stub say CASDI instead of SDI?

CASDI is the full California-specific label. SDI is the shorter version. Both mean the same deduction. The label depends on which payroll software your employer uses.

How much SDI will I pay on a $100,000 salary?

At 1.3% with no wage cap, you will pay $1,300 in SDI contributions for the full year on a $100,000 salary. Want to see the full picture? Our breakdown of $100k after taxes in California shows exactly what you take home after SDI, state income tax, and federal deductions combined.

Final Takeaway: What You Must Remember About CA SDI in 2026

Here is the short version for both employees and employers.

The 2026 CA SDI rate is 1.3%. There is no wage cap. The deduction runs all year on every dollar you earn. It funds Disability Insurance and Paid Family Leave. You pay it. Your employer withholds it. And if you need it, it replaces 60% to 90% of your wages up to $1,765 per week.

Check your January paycheck. Confirm the math. If something looks wrong, speak to your payroll team with these numbers in hand. You now have everything you need to verify your own withholding and understand exactly where your money goes.

The SDI system works when people understand it. Now you do. For more guides covering employee rights, pay rules, and deduction laws, explore our full California labor laws resource library.

Information sourced from the California Employment Development Department (EDD) General Release Letter effective January 1, 2026, and California Unemployment Insurance Code section 984(a)(1). This content is for informational purposes only and does not constitute legal, tax, or financial advice. Consult a licensed tax professional or employment attorney for guidance specific to your situation.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.