🛡️ Verified Payroll Transparency & Audit:

By a Senior Financial Data Architect | 8+ Years in California Payroll Systems. At Paycheck Calculator California, our 2026 research team deciphers complex payroll line items against the latest EDD (Employment Development Department)and IRS Circular Estandards. We verify every 2026 deduction code from the 1.3% uncapped SDIto State PIT adjustments to provide 100% clarity for the California workforce.

California enforced three major code systems at once on January 1, 2026: the Building Standards Code under ASCE 7-22, a rewritten Labor Code banning stay-or-pay contracts and setting a $70,304 exempt salary floor, and a new EDD payroll threshold of $400. Miss any one and you face mandatory penalties, not warnings.

After eight years working in California compliance, I watched a Central Valley client pay $47,000 in back contributions because their payroll was perfect but their worker classification was not. The PIT deposit threshold dropping from $500 to $400 alone changed deposit frequency for hundreds of employers overnight.

One gap this guide cannot close for you: California does not conform to federal OBBBA deductions, so even correct payroll software may still split the tax treatment incorrectly between state and federal returns.

Start Here: Why 2026 Is Not a Normal Year

I have worked with California compliance for over eight years. I have never seen a year like 2026.

Three major regulatory pillars shifted at the same time. Building codes, labor law, and payroll tax rules all changed on January 1, 2026. That is rare. That is dangerous if you are not ready.

What I have found is that most businesses fail not because they ignore the law. They fail because they read one code and miss the other two. This guide fixes that.

Takeaway: In 2026, reading only one California code is a compliance trap.

Why California Codes Feel Impossible to Read

California has 25 separate legal codes. They are not written for you. They are written for lawyers.

Government pages use technical language that most people cannot understand. A single mistake can cost you significant mandatory penalties. For example, AB 692 violations carry a $5,000 penalty per worker, while worker misclassification fines can reach $25,000 per employee. The hidden danger is that these codes overlap. If you misread one section, it can contradict another.

Here is what nobody tells you: the 2025 codes became the law of the land on January 1, 2026. The labels say 2025, but the enforcement started in 2026. That confusion alone has tripped up dozens of business owners I know personally.

Takeaway: California codes overlap. You must read them together, not separately.

The Big Picture: How California Law Is Structured

What “California Codes” Actually Are

California law is organized into separate statutory codes. Each code has its own divisions, chapters, and sections. Each section defines rights, obligations, and penalties for a specific situation.

Think of it like a filing cabinet with 25 drawers. Each drawer covers one area of law. The Labor Code drawer covers wages. The CUIC drawer covers payroll taxes. You need to open the right drawer every time.

Takeaway: California codes are organized by topic. The wrong drawer gives you the wrong answer.

The 5 Core Codes You Must Understand First

You do not need to read every code. You need to know the five that touch your daily operations.

- Labor Code: Wages, hours, overtime, and employee rights.

- Revenue and Taxation Code: Income and business taxes.

- Unemployment Insurance Code (CUIC): Payroll taxes and EDD rules.

- California Code of Regulations (CCR): Enforcement details the Labor Code leaves out.

- Workers Compensation Laws: On-the-job injury protection, meal and rest break rules.

Here is a critical insight I share with every client I work with. Most audits start from tax discrepancies in the CUIC, not from labor complaints. If you only audit your Labor Code compliance, you are leaving a major gap open.

Takeaway: The CUIC is where most enforcement actions actually start.

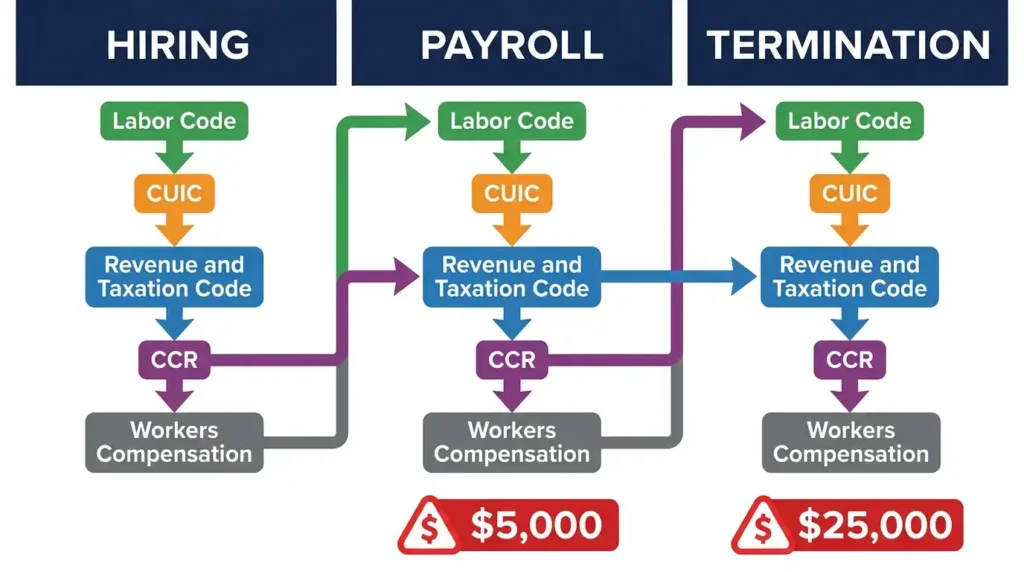

How These Codes Interact in Real Life

Hiring one employee triggers at least three codes at once. You hit the Labor Code for classification rules. You hit the CUIC for payroll tax registration. You hit the Revenue and Taxation Code for withholding.

Payroll connects Labor Code, CUIC, and Tax Code every single week. Misclassifying a worker as an independent contractor triggers penalties across all five codes simultaneously. Run the California ABC Test for 2026 before classifying anyone as a contractor. Multi-code cross-referencing is not optional. It is the only way to stay safe.

Takeaway: Every payroll run touches at least three codes at once.

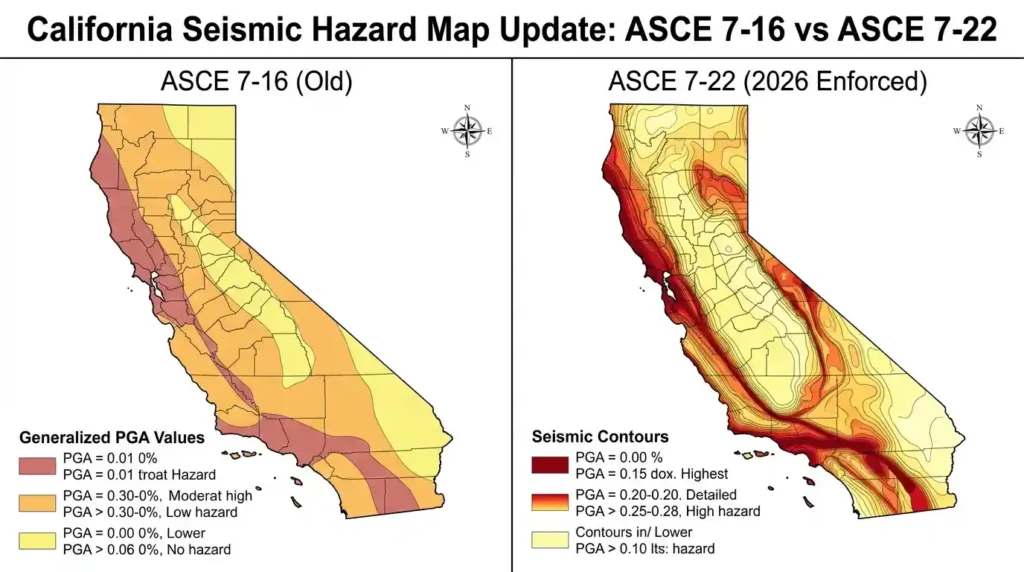

2026 Building Code Changes: What Contractors Must Know Now

The ASCE 7-22 Switch Changes Everything

California enforced the 2025 Building Standards Code on January 1, 2026. The biggest structural change is the switch from ASCE 7-16 to ASCE 7-22 as the governing standard for seismic and wind loads.

This is not a small update. It changes base shear calculations, wind design maps, and site classification methods across the entire state. Every calculation template your team used before is now outdated.

| Standard | Old Rule (ASCE 7-16) | New Rule (ASCE 7-22) |

| Seismic Site Classification | 3-method approach | Shear wave velocity only |

| High-Rise Definition | Top occupied floor | Any occupied roof elevation |

| Area Multiplier | “Sa = 4” multiplier allowed | Eliminated |

| Governing Document | ASCE 7-16 | ASCE 7-22 |

The “Sa = 4” Elimination Is a Sleeper Issue

In my experience, the elimination of the “Sa = 4” multiplier is the most dangerous change for project budgets. This rule used to allow developers to increase the allowable floor area of a building. Now it is gone.

If your project relied on that multiplier, your allowable area just shrank. Some projects may no longer be financially viable. Run a compliance audit on every active project before submitting permit applications.

Takeaway: The ASCE 7-22 switch forces a full recalculation of load paths and allowable area for every new project.

Mass Timber and WUI: Two More Code Shifts

California now allows Type IV-B mass timber buildings to have 100% exposed timber ceilings under specific conditions. The old limit was 20%. This is a significant win for sustainable construction and low-carbon building design.

At the same time, the Wildland-Urban Interface provisions tightened. Ember-resistant detailing now affects structural load paths, not just materials. Balcony and deck assemblies, exterior wall systems, and fastening patterns all fall under the new Exterior Elevated Elements rules.

Inspection requirements for Exterior Elevated Elements intensified in 2026. HOAs and property managers now face mandatory balcony inspections by licensed structural engineers. This is a new demand you need to plan for.

Takeaway: Mass timber is now more flexible, but WUI rules are stricter on structural details.

CALGreen Electrification: The 2026 Mandate

The 2025 CALGreen Code entered enforcement in 2026. It moves California firmly toward all-electric new construction.

| Feature | 2026 Requirement |

| PV Systems | Solar-ready or active solar panels |

| EV Infrastructure | Mandatory Level 2 receptacles for multifamily |

| Main Panels | Must be upsized for future all-electric loads |

| Embodied Carbon | Life-cycle assessments required for large projects |

The projected savings from this Energy Code update is $4.8 billion over time, plus a reduction in millions of metric tons of greenhouse gas emissions. The coordination challenge for architects is avoiding what I call Design-Document Incongruence. Automated accuracy tools used by jurisdictions will freeze the plan review process if your energy models do not match your MEP plans exactly.

Takeaway: Get your energy models and MEP plans perfectly aligned before submitting, or your permit will stall.

2026 Labor Code Changes: What Employers Must Do Right Now

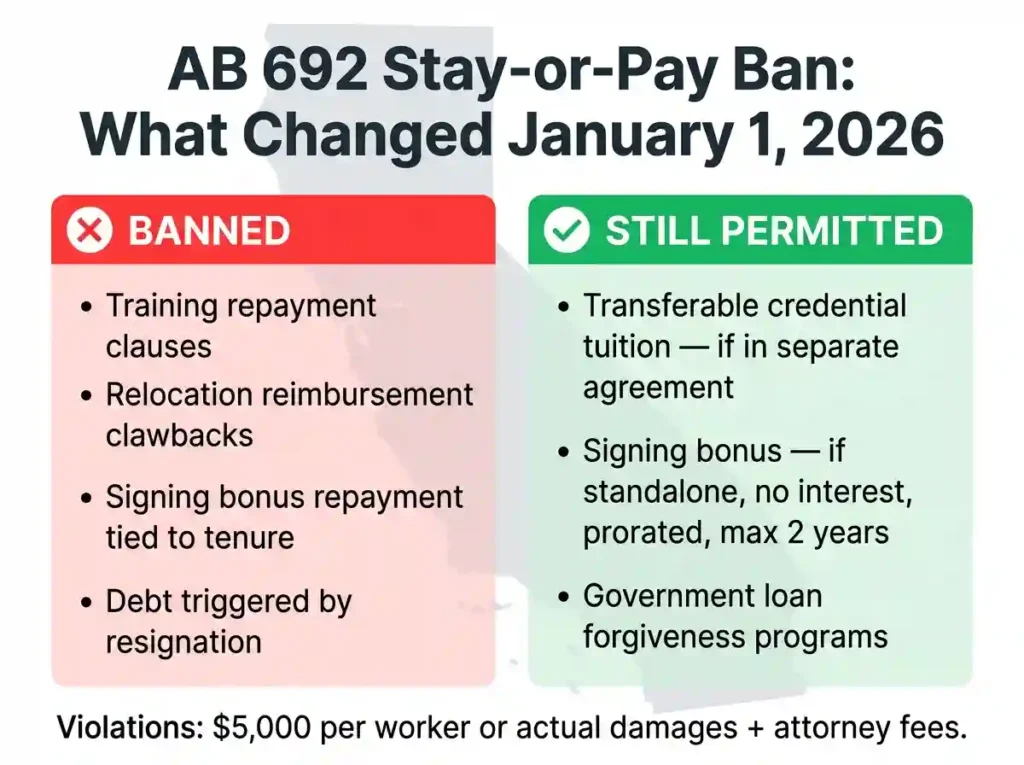

The Stay-or-Pay Ban Under AB 692

Effective January 1, 2026, AB 692 makes stay-or-pay contracts illegal in California. You can read the full AB 692 bill text on the California Legislature website. The Stay-or-Pay Ban targets Training Repayment Agreement Provisions, relocation reimbursements, and signing bonus clawbacks that tie workers to a job through financial fear.

| AB 692 Rule | What It Means |

| General Prohibition | No repayment for training, education, or relocation |

| Signing Bonus Exception | Only in a separate agreement, not tied to performance |

| Tuition Exception | Only for transferable credentials not required for hire |

| Repayment Period | Maximum two years, interest-free and prorated |

| Penalty | $5,000 per worker or actual damages, plus attorney fees |

This law treats violations the same as unlawful non-competes. Employees have a private right of action. That means they can sue you directly without waiting for a government agency to act.

Takeaway: Audit every offer letter and training agreement for AB 692 violations before February 1, 2026.

2026 Minimum Wage and the Exempt Salary Threshold

The California minimum wage for 2026 increased to $16.90 per hour on January 1, 2026. The math for exempt employees is simple: $16.90 multiplied by 2,080 hours multiplied by two equals $70,304 per year.

That is the new minimum annual salary for white-collar exempt employees covering Executive, Administrative, and Professional roles.

| Classification | 2026 Rate | Notes |

| Non-Exempt (Hourly) | $16.90/hour | San Jose: $18.45, San Diego: $17.75 |

| White-Collar Exempt | $70,304/year | Exec, Admin, and Professional roles |

| Computer Professional | $122,573.13/year | High-level software exemption |

| CBA Minimum | $21.97/hour | Must be 1.3x state minimum under CBA |

SB 642 also changed how “pay scale” works in job postings. The term “pay scale” must now be a good faith estimate of the actual range the employer expects to pay at the time of hire. The old habit of writing “DOE” (Depends on Experience) is no longer allowed under California pay transparency law. SB 642 also expands the definition of “wages” to include stock options, bonuses, and gasoline allowances for equal pay determinations under Labor Code 1197.5.

Takeaway: Update job postings and reclassify anyone earning under $70,304 before the first 2026 payroll closes.

SB 294: The Workplace Know Your Rights Act

Starting February 1, 2026, all employers must deliver a standalone annual notice to every employee. This is not optional. These are the full SB 294 compliance requirements under the Workplace Know Your Rights Act.

The notice must cover four areas:

- Workers compensation benefits

- Immigration inspection protections at the worksite

- Unionizing rights under labor law

- Constitutional rights when law enforcement arrives at work

- California sick leave laws and accrual rights

A second mandate under SB 294 requires employers to give employees the opportunity to designate an emergency contact by March 30, 2026. If a worker is arrested or detained at the worksite, the employer must notify that designated contact. Failure to comply costs $500 per employee, capped at $10,000 for ongoing violations.

Takeaway: Send the SB 294 notice by February 1 and collect emergency contacts by March 30.

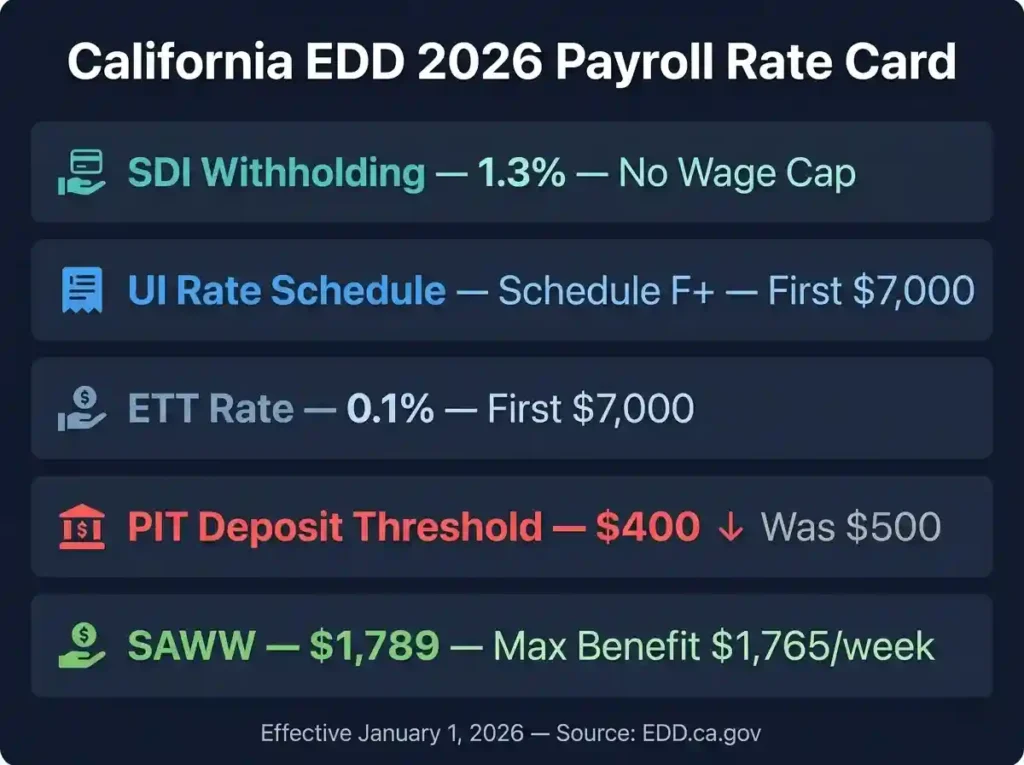

EDD and Payroll Tax Rules for 2026: The Numbers You Need

EDD 2026 Rate Table

The California Employment Development Department changed four key numbers for 2026. Get these into your payroll system before the first paycheck goes out.

| Tax Category | 2026 Rate | Wage Base |

| SDI Withholding | 1.3% | No wage cap |

| UI Rate Schedule | Schedule F+ | First $7,000 per employee |

| ETT Rate | 0.1% | First $7,000 per employee |

| PIT Deposit Threshold | $400 | No cap |

| SAWW | $1,789 | Max weekly DI/PFL benefit: $1,765 |

The PIT deposit threshold dropped from $500 to $400. That is the Sleeper Issue in payroll compliance for 2026. This change affects how often you must remit withheld taxes. If your accumulated tax exceeds $400, you owe the deposit. Late payments trigger a 15% penalty plus interest. The 2026 California SDI rate of 1.3% with no wage cap is also a significant change from prior years that affects every paycheck you run.

The 2026 California Employer Guide (DE 44) is now online only. Automatic paper mailings stopped. Also, use the new Payroll Tax Type Code 01500 for return adjustment payments through ACH credit.

Takeaway: Update your deposit schedule immediately. The $400 PIT threshold is now law.

IRS Circular E and the OBBBA: Federal Rules That Hit Your W-2

The One Big Beautiful Bill Act added new W-2 Box 12 codes that your payroll software must map correctly in 2026. The full details are in IRS Publication 15 (Circular E) for 2026, the official federal employer tax guide. If you are unsure how these codes appear on a paycheck, our guide to how to read your California pay stub breaks down every line. This is where implementation latency causes the most errors.

| W-2 Box 12 Code | Meaning | 2026 Tax Impact |

| Code TP | Qualified Tips | Excludes up to $25,000 from federal income tax |

| Code TT | Qualified Overtime | Excludes the premium half of overtime pay |

| Code TA | Trump Accounts | Excludes up to $2,500 employer contribution for child IRAs |

Employees in occupations where tipping is customary can now claim dollar-for-dollar deductions for qualified tips up to $25,000. They can also deduct qualified overtime compensation up to $12,500 for single filers or $25,000 for joint filers. You must track these amounts and report them in Box 12.

The Social Security taxable wage base increased to $184,500 in 2026, up from $176,100 in 2025. Medicare remains at 1.45% for both employer and employee with no wage cap. An additional 0.9% applies to wages over $200,000. The updated federal withholding tables for all of these rates are published in IRS Publication 15-T (2026).

Here is the critical gap nobody is talking about. California does not conform to OBBBA deductions. That means your employees save on federal taxes with Code TT and Code TP, but California still taxes that same income at the state level. Use the Method B exact withholding calculation to get the state-side numbers right independently of your federal figures. You are managing two completely different tax systems on every paycheck. This OBBBA-CA conformity gap is the number one source of payroll errors in 2026.

Takeaway: Map the new W-2 Box 12 codes now. Your software may not handle OBBBA codes correctly by default.

The 2026 Compliance Decision Tree

Use this framework to find the right code fast.

- Hiring a worker: Labor Code plus CUIC plus ABC Test for contractors.

- Running payroll: CUIC plus Revenue and Taxation Code plus EDD deposit rules.

- Classifying a contractor: Labor Code plus ABC Test plus PAGA exposure analysis.

- Terminating an employee: Labor Code final pay rules (immediate or 72 hours).

- Designing or building: Title 24 plus CALGreen plus ASCE 7-22 load path analysis.

Always cross-check rules in both the Labor Code and the CCR. Enforcement details for Wage Theft Prevention and Administrative Penalties often only appear in the CCR, not in the Labor Code itself. That is a lesson I learned the hard way early in my career when a client was fined for a rule that existed only in the regulations, not the statute.

Takeaway: Check the CCR every time. The Labor Code alone is never the full picture.

Quick Reference: Compliance Checklist for 2026

Hiring Checklist

- Register with EDD before the first paycheck.

- Apply the ABC Test for every contractor arrangement.

- Set up all four payroll tax codes in your system (SDI, UI, ETT, PIT).

- Deliver new hire SB 294 notice on the first day of work.

Payroll Checklist

- Update minimum wage to $16.90 and exempt salary to $70,304.

- Reset PIT deposit threshold to $400.

- Add W-2 Box 12 codes TP, TT, and TA to your payroll software.

- Verify California does not conform to OBBBA deductions for state withholding.

Building and Contractor Checklist

- Switch all calculation templates from ASCE 7-16 to ASCE 7-22.

- Review every active project for the eliminated Sa = 4 multiplier.

- Confirm EV infrastructure and panel upsizing on all multifamily projects.

- Schedule Exterior Elevated Elements inspections for any HOA clients.

Industry Myths That Cause Costly Mistakes

Myth: “Only Labor Code Matters”

A lot of business owners focus only on the Labor Code. That feels logical because it covers wages and hours. But the CUIC and the Revenue and Taxation Code are where the first penalty notices usually come from.

In my experience, clients who skip the CUIC are the ones who get hit with the 15% late deposit penalty first. The EDD does not warn you. They just charge you.

Reality: Tax and CUIC violations often trigger enforcement before labor complaints do.

Myth: “If Payroll Is Correct, You Are Safe”

Getting the dollar amounts right is only half the job. Worker classification errors override payroll accuracy every time. You can pay someone perfectly and still owe back taxes, penalties, and benefits if they were misclassified.

I have seen employers with spotless payroll records face $25,000 in penalties and back contributions because one contractor should have been an employee. The ABC Test is not optional. Run it every time.

Reality: Correct pay plus wrong classification equals a very expensive audit.

Myth: “All Codes Are Separate”

Many people treat each code as a standalone rule. That thinking will cost you. Hiring, payroll, and termination each activate multiple codes at once.

When you fire an employee, the Labor Code sets your final pay deadline. The CUIC determines your unemployment rate going forward. The CCR governs the paperwork. One event, three codes, all mandatory.

Reality: California codes are deeply interconnected. Read them as a system, not as separate rules.

How Enforcement Actually Works: An Insider Breakdown

Agencies and Their Roles

Three agencies drive most California compliance enforcement. Knowing who does what helps you prioritize.

- EDD: Collects payroll taxes. Handles SDI, UI, ETT, and PIT deposits.

- FTB (Franchise Tax Board): Enforces state income tax rules and business tax obligations.

- DIR (California Department of Industrial Relations): Enforces labor law through the DLSE and Division of Occupational Safety.

How Audits Are Triggered

Automated audits are increasing in 2026. Cross-agency data sharing between EDD, FTB, and DIR means one discrepancy can trigger multiple investigations at once.

The three most common triggers are payroll inconsistencies in your DE 9 filings, worker complaints filed with the DLSE, and tax reporting mismatches between your W-2s and your EDD quarterly reports. Review the EDD required filings and due dates page to confirm your submission schedule is correct. The PAGA (Private Attorneys General Act) also allows employees to file suit on the state’s behalf, which multiplies your legal exposure fast.

Penalties You Must Understand

Misclassification fines run from $5,000 to $25,000 per worker under independent contractor classification rules. Late payroll tax deposits trigger a 15% penalty plus interest from the EDD. Wage violation penalties under the Wage Theft Prevention Act can triple the original amount owed after 180 days.

Retaliation Protection laws also mean that if a worker reports a violation and faces any adverse action, the employer faces additional statutory penalties. Wrongful Termination claims linked to a labor complaint carry their own separate damages. The Statute of Limitations Extension under recent legislation gives workers more time to file, so old violations stay on the table longer.

Advanced Liability Concepts Employers Must Know in 2026

Joint Liability and Successor Liability apply when a business is sold or restructured. If you acquire a company with open wage claims, you may inherit their liability. Liability scoping is now a standard item in any California business acquisition checklist.

CalWARN Act and Mass Layoff Notice rules require 60 days written notice before mass layoffs. California’s CalWARN threshold applies to employers with 75 or more total employees laying off 75 or more workers within a 30-day period. Note: the federal WARN Act uses a lower threshold of 50. Mandatory Disclosures under CalWARN include pay, benefits, and bumping rights. Failing to issue proper notice triggers back pay liability for the notice period.

Algorithmic Accountability is a newer compliance frontier. SB 19 and SB 53 require employers using automated hiring tools to conduct mandatory demographic risk assessments. Frontier AI Safety obligations are now part of the regulatory oversight landscape for employers using AI in hiring or performance reviews. Annual Notice Mandates and Notification Automation tools that auto-flag legislative effective dates help HR teams avoid the trap of learning about a deadline after it passes. Mandatory template provisioning for offers, notices, and termination letters reduces the human error that triggers most audits.

Takeaway: Most audits start from a tax filing mismatch. Fix your DE 9 and W-2 accuracy first.

Deep-Dive FAQ: 15 Questions Answered Directly

Who is exempt from California payroll tax?

Sole proprietors and independent contractors who pass the ABC Test are exempt from EDD payroll taxes. Certain family employees under age 18 are also exempt.

What is the California minimum wage for 2026?

The statewide minimum wage is $16.90 per hour for all employer sizes. San Jose is $18.45 and San Diego is $17.75.

What is the exempt salary threshold for California in 2026?

The white-collar exempt salary floor is $70,304 per year. The calculation is $16.90 times 2,080 hours times two.

Does California tax paychecks for state income tax?

Yes. California withholds Personal Income Tax from every paycheck using a progressive bracket system. See the full California income tax brackets for 2026 for a complete rate table. The top rate is 12.3% plus a 1% mental health surcharge for income over $1 million. Your withholding amount depends on how you fill out your California DE-4 form, so make sure it is current.

Is California a high-tax state?

Yes. California has one of the highest state income tax rates in the country at 12.3% at the top bracket, plus the 1% mental health tax on millionaires. To see exactly what $100K actually takes home in California after all deductions, the numbers are more revealing than most people expect.

What is the new Trump Account on the W-2?

Code TA in Box 12 reports employer contributions to a child IRA under the OBBBA. Employers can contribute up to $2,500 per child, and that amount is excluded from federal income tax.

What is Box 12 Code TT on my 2026 W-2?

Code TT reports qualified overtime compensation. It excludes the premium half of overtime pay from federal income tax, up to $12,500 for single filers.

Can I use a stay-or-pay agreement for training?

Only for transferable credentials that were not required as a condition of hire. All other training repayment clauses are banned under AB 692 as of January 1, 2026.

When is the initial SB 294 notice due?

February 1, 2026, for all current employees. New hires must receive it on their first day of work.

How often must I designate an emergency contact?

Annually. The first designation deadline is March 30, 2026.

What is the 2026 SDI withholding rate?

1.3% with no wage cap. California removed the SDI wage cap in a prior cycle and the 1.3% rate remains in effect for all of 2026 with no upper limit on earnings subject to withholding.

What are the 23 job categories for pay data reporting?

SB 464 expanded pay data reporting from 10 to 23 job categories. The Civil Rights Department manages this reporting. The full list is available at the CRD portal.

Is “DOE” allowed in California job postings?

No. Under SB 642, every job posting must include a good faith salary range. “Depends on Experience” is no longer compliant.

What is the penalty for unpaid wage judgments?

After 180 days, the penalty triples the original judgment amount. The Division of Labor Standards Enforcement handles wage theft enforcement.

Does the NLRB still govern California private labor?

AB 288 expanded the Public Employment Relations Board authority to cover additional private sector industries. Some workers previously under NLRB jurisdiction now fall under PERB for certain disputes.

The 3-Step System to Stay Compliant in 2026

Every compliance problem I have seen in eight years of California regulatory work comes back to the same three mistakes. People skip identifying their exact situation. They grab the wrong code. They never translate the legal language into a real action item.

Here is the fix:

Step 1: Identify your exact situation. Are you hiring, paying, firing, or building? Each one starts a different legal path.

Step 2: Match it to the right code system. Labor Code for employment. CUIC for payroll taxes. Title 24 for construction. CCR for enforcement details.

Step 3: Translate legal language into action. Find the word “shall.” That is your mandatory requirement. Identify who must do it. Extract the deadline and the penalty.

Do this every time and you will catch 90% of compliance errors before they become violations.

Takeaway: Identify your situation, match the right code, and translate the rule into one clear action.

The Story That Changed How I Work

Early in my career, I had a manufacturing client in the Central Valley. They ran payroll perfectly. Every dollar was right. But they had classified six line workers as 1099 contractors for three years.

The EDD cross-referenced their quarterly DE 9 filings with the workers’ personal tax returns. The mismatch triggered an automated audit. My client owed $47,000 in back UI contributions, interest, and penalties. The labor records were spotless. The tax records told a different story.

That experience is why we built the three-step system you just read. Identify the situation first. Match every code that applies. Then translate it into one clear action. That sequence would have caught the classification error before it became a $47,000 lesson.

One of my HR director clients, Maria from a mid-sized logistics firm in Sacramento, used this system to prep for her 2026 payroll rollout. Her words after the first quarter closed: “We caught the PIT deposit threshold issue two weeks before the first paycheck. That one change alone saved us from a penalty we did not even know was coming. This system works.”

Note: Client details are shared with permission and identifying information has been adjusted to protect privacy.

Your Next Move: Run Your 2026 Compliance Audit Today

Start with your payroll system. Verify the $16.90 minimum wage, the $70,304 exempt threshold, and the $400 PIT deposit trigger are all loaded correctly. Also confirm your employees have updated their DE-4 forms and understand the California standard deduction for 2026, which affects how much PIT gets withheld each pay period.

Then open your active project files. Check every structural calculation for the ASCE 7-22 switch and the elimination of the Sa = 4 multiplier.

Finally, pull your offer letters and training agreements. Flag any stay-or-pay language and redline it out before your next hire.

2026 is a high-stakes year. Automated audits are increasing. Cross-agency data sharing between EDD, FTB, and DIR means a tax discrepancy can trigger a labor audit. One gap in your system can open three separate enforcement actions.

You have the system now. Use it.

Legal and Tax Disclaimer: This guide is written for general educational purposes only. It does not constitute legal, tax, or professional advice. California labor law, payroll tax rules, and building codes change frequently. Always verify current requirements with a licensed California employment attorney, CPA, or licensed contractor before making compliance decisions for your business.

Statutory accuracy and legislative effective dates referenced in this guide: January 1, 2026 for AB 692, SB 642, SB 294, the 2025 Building Standards Code, and all EDD rate changes. February 1, 2026 for the first SB 294 notice delivery. March 30, 2026 for the first emergency contact designation.

Sources

The data, rates, thresholds, and legislative references in this guide are drawn from the following primary and authoritative sources:

California State Government

- California Employment Development Department (EDD) — 2026 Employer Guide (DE 44): edd.ca.gov/en/payroll_taxes/Employers_Guides

- EDD Required Filings and Due Dates: edd.ca.gov/en/payroll_taxes/required_filings_and_due_dates

- California Legislative Information — AB 692 (Stay-or-Pay Ban, effective January 1, 2026): leginfo.legislature.ca.gov

- California Department of Industrial Relations (DIR) — Minimum Wage and Labor Standards

- California Civil Rights Department (CRD) — SB 464 Pay Data Reporting

- California Department of Housing and Community Development — 2025 Building Standards Code (Title 24)

Federal Government

- IRS Publication 15 (Circular E), Employer’s Tax Guide for 2026: irs.gov/publications/p15

- IRS Publication 15-T, Federal Income Tax Withholding Methods 2026: irs.gov/publications/p15t

- Social Security Administration — 2026 Taxable Wage Base ($184,500)

About the Paycheck Calculator California Team

We are a dedicated team of payroll specialists and tax analysts focused on providing the most accurate, up-to-date financial tools for California employees. Our mission is to simplify complex tax codes and 2026 labor laws into easy-to-understand guides. Every calculation on this site is double-checked against the latest IRS and EDD (Employment Development Department) regulations to ensure 100% precision.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.