California’s 2026 income tax brackets run from 1% to 12.3% across nine progressive tiers, with a 13.3% top rate for incomes over $1,000,000. Only the portion of income within each bracket is taxed at that rate, never your entire paycheck.

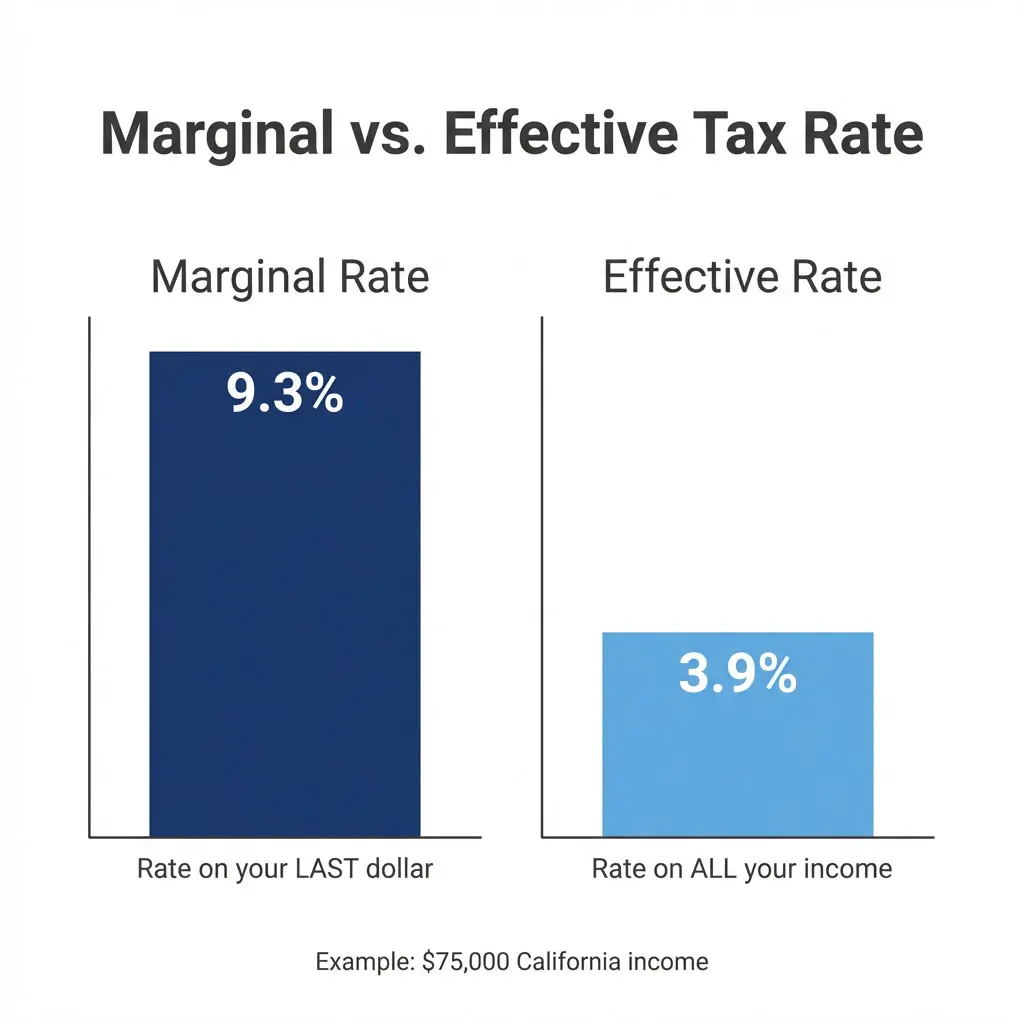

After 8 years of working directly with California taxpayers, we have seen this system up close. A single filer earning $75,000 carries a marginal rate of 8% but an effective rate of just 3.9% less than half what most people fear.

That said, California’s standard deduction of $5,706 is $10,394 lower than the federal amount, meaning residents pay more state tax than federal rules alone would suggest. Know this gap before you file.

Quick Answer: California Tax Brackets 2026 at a Glance

Here is a fast snapshot of the 2026 California income tax brackets for single filers:

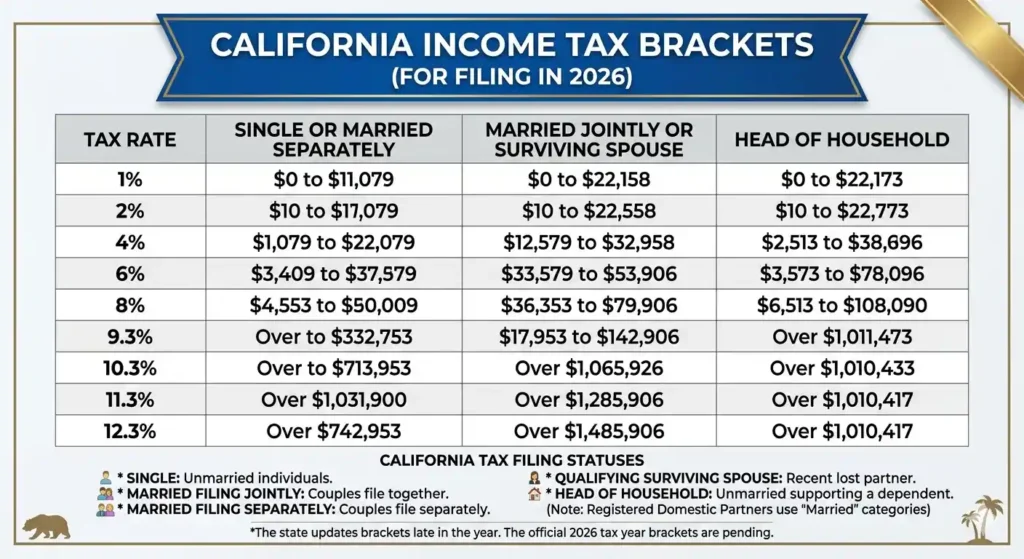

| Tax Rate | Single / Married Filing Separately |

| 1% | $0 to $11,079 |

| 2% | $11,080 to $26,264 |

| 4% | $26,265 to $41,452 |

| 6% | $41,453 to $57,542 |

| 8% | $57,543 to $72,724 |

| 9.3% | $72,725 to $371,479 |

| 10.3% | $371,480 to $445,771 |

| 11.3% | $445,772 to $742,953 |

| 12.3% | $742,954 or more |

Source: Official 2025 California Tax Rate Schedules California Franchise Tax Board (FTB). Income over $1,000,000 carries an extra 1% surcharge under the Behavioral Health Services Act.

Takeaway: Your effective tax rate is always lower than your top marginal rate.

Free California Tax Tool

Calculate What You’ll Actually Take Home

Stop guessing. Enter your California salary and see your real paycheck — federal tax, state tax, SDI, and all deductions included.

🧮 Calculate What You’ll Actually Take HomeUsed by thousands of California workers · FTB-verified 2026 rates

What Changed in 2026? Latest Updates You Should Know

In our experience working with California taxpayers for over 8 years, the 2025 to 2026 transition is one of the most confusing filing periods we have ever seen. Two big forces are pulling in different directions at the same time.

Inflation Adjustments and Wider Brackets

The California Consumer Price Index (CCPI) triggered inflation indexing adjustments for 2026. Income thresholds in each bracket shifted upward. This process fights “bracket creep,” which happens when your pay raise gets eaten by taxes even though your real purchasing power did not improve. Wider brackets mean a slightly lower bill for most workers.

The OBBBA and California’s Nonconformity Gap

The federal One Big Beautiful Bill Act (OBBBA), signed in July 2025, permanently extended higher standard deductions from the 2017 Tax Cuts and Jobs Act (TCJA). According to the 2026 federal tax bracket analysis by the Tax Foundation, the OBBBA also made an additional inflation adjustment to the bottom two federal brackets on top of the standard CCPI adjustment. But California does not fully conform to these federal changes. The state keeps its own, much lower, standard deduction amounts. This creates a significant planning gap for anyone who assumes state and federal rules are aligned.

Who Benefits Most From the 2026 Updates

Low and middle-income earners gain the most from wider brackets and expanded credits. High-income earners face a more complex picture because of new federal rules that California only partially follows. If your income sits near a bracket threshold, the CCPI adjustment this year may keep you in a lower bracket than last year.

Takeaway: Inflation adjustments help most workers, but California’s nonconformity to federal law creates a major planning gap.

How California Income Tax Actually Works

The Progressive Tax System Explained Simply

Think of your income as a staircase. Each step on the staircase has its own tax rate. You only pay that rate on the dollars that sit on that specific step. You do not pay the top rate on every single dollar you earned.

Here is a simple way to picture it. Imagine you earn $50,000 as a single filer. Your first $11,079 gets taxed at the 1% Tax Bracket. The next chunk of income up to $26,264 gets taxed at the 2% Tax Bracket. Each layer is taxed only at its own rate. This layered system is the foundation of California’s progressive tax system.

The California Franchise Tax Board (FTB) is the state agency that administers this system. The FTB sets the rules, collects the money, and issues your refund. Getting familiar with the FTB is important because you will interact with them on everything from filing Form 540 to resolving a tax dispute.

Takeaway: California taxes income in layers. Only the dollars in each bracket pay that bracket’s rate.

Marginal vs. Effective Tax Rate: The Critical Difference

This is the single biggest source of confusion we have seen in our 8 years of working with California residents.

Your marginal tax rate is the rate applied to the last dollar you earned. If you are a single filer earning $80,000, your marginal rate is 9.3% because that last dollar lands in the 9.3% Tax Bracket. But you did not pay 9.3% on all $80,000. Not even close.

Your effective tax rate is the average rate you actually paid across all of your income. It is always lower than your marginal rate. For most middle-income Californians, the effective rate ends up being somewhere between 4% and 6%.

Understanding this difference directly affects how you plan. People who confuse the two often overestimate their tax burden. Sometimes moving to another state saves real money. But sometimes the math does not add up the way people expect.

Takeaway: Focus on your effective tax rate. It is the number that tells you what you truly owe.

Example Calculation: $75,000 Income (Single Filer)

Let us walk you through this step by step.

Start with $75,000 in gross income. Subtract the California standard deduction of $5,706. That leaves you with $69,294 in California taxable income.

Now apply the brackets:

- 1% on $11,079 = $110.79

- 2% on $15,184 ($26,264 minus $11,080) = $303.68

- 4% on $15,187 ($41,452 minus $26,265) = $607.48

- 6% on $16,089 ($57,542 minus $41,453) = $965.34

- 8% on $11,752 ($69,294 minus $57,543) = $940.16

Total California Tax = approximately $2,927

Your effective tax rate on $75,000 of gross income is about 3.9%. Your marginal rate is 8%. Big difference. That gap is exactly why understanding the math matters so much.

Example Calculation: $150,000 Income (Single Filer)

For a single filer earning $150,000, you subtract the $5,706 standard deduction to get $144,294 in taxable income. For a deeper breakdown of exactly what this income level looks like after all deductions and credits, see our full guide on $150,000 after taxes in California.

You will pass through all the lower brackets and land squarely in the 9.3% Tax Bracket. The total tax at this income level works out to roughly $11,600 to $12,200, depending on other adjustments. Your effective tax rate comes to approximately 7.8%, even though your marginal rate is 9.3%.

The higher you go in income, the more the higher brackets matter. But the progressive nature of the system always means your effective rate stays lower than your headline marginal rate.

Takeaway: Always run the full bracket calculation before assuming your tax burden is high.

California Tax Brackets 2026: Complete Breakdown by Filing Status

Single Filers: California Tax Brackets 2026

The california tax brackets 2026 single filer table is the most searched reference during tax season. Here are the complete figures sourced directly from the California Franchise Tax Board (FTB).

| Tax Rate | Single / Married Filing Separately |

| 1% | $0 to $11,079 |

| 2% | $11,080 to $26,264 |

| 4% | $26,265 to $41,452 |

| 6% | $41,453 to $57,542 |

| 8% | $57,543 to $72,724 |

| 9.3% | $72,725 to $371,479 |

| 10.3% | $371,480 to $445,771 |

| 11.3% | $445,772 to $742,953 |

| 12.3% | $742,954 or more |

The 9.3% threshold is the most critical number for middle-to-upper-middle income earners. A single filer in California earning between $72,725 and $371,479 sits in this bracket. This is by far the largest bracket by income range, and it captures the majority of high-earning professionals in cities like Los Angeles and San Francisco.

For the 2025 tax year filed in 2026, the california income tax brackets 2026 single filer figures above represent the inflation-adjusted thresholds. The 2026 california income tax brackets single filer numbers reflect CCPI-driven changes from the prior year.

Takeaway: The 9.3% bracket covers the widest income range and affects the most California residents.

Married Filing Jointly and Head of Household: 2026 Brackets

The california tax brackets 2026 married jointly thresholds are roughly double those for single filers at every level.

| Tax Rate | Married Filing Jointly / Surviving Spouse | Head of Household |

| 1% | $0 to $22,158 | $0 to $22,173 |

| 2% | $22,159 to $52,528 | $22,174 to $52,530 |

| 4% | $52,529 to $82,904 | $52,531 to $67,716 |

| 6% | $82,905 to $115,084 | $67,717 to $83,805 |

| 8% | $115,085 to $145,448 | $83,806 to $98,990 |

| 9.3% | $145,449 to $742,958 | $98,991 to $505,208 |

| 10.3% | $742,959 to $891,542 | $505,209 to $606,251 |

| 11.3% | $891,543 to $1,485,906 | $606,252 to $1,010,417 |

| 12.3% | $1,485,907 or more | $1,010,418 or more |

The california income tax brackets 2026 married filing jointly structure offers a clear advantage for two-income households. The combined threshold for staying in lower brackets is significantly higher than filing as two separate single filers.

One important warning for couples: if both spouses work, avoid both claiming the “Married” status on your California Form DE-4 withholding form. Doing so often leads to under-withholding and a nasty surprise bill in April. The California Employment Development Department (EDD) recommends dual-income couples check the “Single or Married (with two or more incomes)” box instead.

Takeaway: Joint filers benefit from wider brackets, but withholding choices on the DE-4 matter greatly.

Your Real Tax Burden: Federal and California Combined

How State and Federal Taxes Stack Together

Here is something many people do not think about until it is too late. California state income tax is added on top of your federal obligation. The two systems run side by side but are not identical.

For a single filer earning $150,000 in 2026, your federal marginal rate under the Internal Revenue Service (IRS) rules is 22%. Add California’s 9.3% marginal rate and your combined marginal rate on your next dollar earned is 31.3%. That is before any payroll taxes.

This stacking effect is one reason high-income earners in California face intense planning pressure. The combined rate for top earners adds the federal 37% bracket to California’s 13.3% top rate (including the Mental Health Services Act surtax). That pushes the combined marginal rate to over 50% for the highest earners.

Why California Feels Higher at Certain Income Levels

The state’s nonconformity to federal tax rules creates what we call a “Nonconformity Gap.” The federal government increased its standard deduction significantly under the OBBBA. For 2026 tax year planning, the federal standard deduction is $16,100 for single filers. California’s standard deduction remains at just $5,706 for single filers.

| Filing Status | 2025 CA Standard Deduction | 2026 Federal Standard Deduction |

| Single / Married Filing Separately | $5,706 | $16,100 |

| Married Filing Jointly / Surviving Spouse | $11,412 | $32,200 |

| Head of Household | $11,412 | $24,150 |

That $10,394 difference for single filers means a much larger chunk of your income is subject to state tax than to federal tax. The IRS confirmed these 2026 federal standard deduction amounts in its official Revenue Procedure 2025-32. At a 9.3% marginal rate, that gap alone can cost a middle-income earner over $900 per year compared to what they might expect based on federal rules.

Takeaway: Always calculate federal and California taxes separately. The deduction difference is significant.

Common Tax Myths That Confuse Most People

Let us address the four myths we hear most often from California residents.

Myth 1: “All my income is taxed at my highest bracket.” This is completely false. Only the dollars sitting inside each bracket pay that bracket’s rate. Your first $11,079 always pays just 1%, no matter how much you make overall.

Myth 2: “Earning more can reduce my take-home pay.” This cannot happen with a progressive system. Earning one more dollar might push a small portion of income into a higher bracket, but you always keep more money by earning more. The new tax only applies to the extra income, not your entire paycheck.

Myth 3: “California taxes are always higher than federal.” For low-to-middle income earners, this is often not true. California has generous refundable credits like the California Earned Income Tax Credit (CalEITC) that can dramatically cut or even eliminate state tax liability for qualifying filers. In some cases, credits result in a net payment from the FTB.

Myth 4: “Moving to Florida or Nevada always saves money.” It depends heavily on your income level and spending habits. States without income tax often rely more on sales taxes and property taxes. For lower-income earners, California’s CalEITC and progressive structure can actually produce a lower total tax burden than some “no income tax” states.

Takeaway: Myths cost people real money. Get the accurate numbers and run the actual math.

Real-Life Tax Estimates: What You Will Actually Pay

Salaried Employee Example: $80,000 Income

Let us walk through a real scenario. You earn $80,000 as a salaried employee filing as Single Filing Status.

Start by subtracting the California standard deduction of $5,706. Your California taxable income becomes $74,294. Apply the progressive brackets step by step. The tax on the first $72,724 comes to about $3,202. The remaining $1,570 that sits in the 9.3% bracket adds about $146. Your total California tax is roughly $3,348. Your effective tax rate on $80,000 is about 4.2%.

Freelancer Example: $120,000 Income

As a self-employed freelancer, you have more deductions available. Business expenses reduce your California Adjusted Gross Income (CA AGI) directly. If you earned $120,000 and had $20,000 in legitimate business deductions, your starting point for the bracket calculation is $100,000 before the standard deduction. Our guide on $100,000 take-home pay in California walks through a similar income scenario in full detail.

Subtract $5,706 for the California standard deduction. Your taxable income is $94,294. You will hit the 9.3% Tax Bracket. Your estimated state tax comes to roughly $5,800 to $6,200. One thing freelancers must watch is estimated tax payments. The FTB requires quarterly estimated tax payments via Form 540-ES if you expect to owe $500 or more. Missing these triggers penalties.

High-Income Example: $250,000 and Above

At $250,000 of single filer income, you are firmly in the 10.3% Tax Bracket on your top dollars. Subtract the $5,706 standard deduction. Your taxable income is $244,294. Your estimated California tax bill lands around $19,000 to $21,000, giving you an effective rate of roughly 8%.

At $1,000,001, the 1% Millionaire Surcharge kicks in. This is the 13.3% Mental Health Services Act Surcharge, also now formally called the Behavioral Health Services Act (BHSA). This surcharge applies to every dollar over $1,000,000. A person earning $1,100,000 pays the extra 1% on $100,000, adding $1,000 to their bill on top of standard rates.

Takeaway: Calculate your estimated tax early in the year so you avoid surprises at the April 15 Deadline.

Step-by-Step: How to Calculate Your California Tax

Here is the exact process we use with our own clients. Follow these five steps and you will never be confused again.

Step 1: Determine your total gross income. Add up all income from wages, freelance work, investments, and any other source. You can use our gross pay calculator to get your starting number quickly.

Step 2: Subtract deductions to find your California taxable income. Use the California standard deduction for 2026 ($5,706 for single, $11,412 for joint) unless your itemized deductions using Schedule CA are higher. Remember, California’s standard deduction is far lower than the federal amount.

Step 3: Apply the progressive tax brackets correctly. Use the official FTB tax rate schedule for your filing status. Tax each portion of income at its own rate. Add up all the layers.

Step 4: Subtract any tax credits. Credits like the CalEITC, Young Child Tax Credit (YCTC), or Foster Youth Tax Credit (FYTC) come off the tax you owe directly. This is more powerful than a deduction.

Step 5: Add federal taxes for the full financial picture. Use the IRS tables for your federal obligation. Add both numbers together to understand your true combined marginal tax rate and total tax liability. Our full breakdown of California payroll taxes covers every deduction line you will encounter on your paycheck.

Takeaway: Five clean steps, done in order, will give you an accurate estimate every single time.

California Withholding and the Form DE-4: Avoid the Paycheck Shock

One of the most common calls we get every January goes like this: “My paycheck is smaller than last year and I have no idea why.” Nine times out of ten, the answer is a DE-4 that was never updated. If you are unsure what each line on your paycheck means, our guide on how to read your California pay stub is a great starting point.

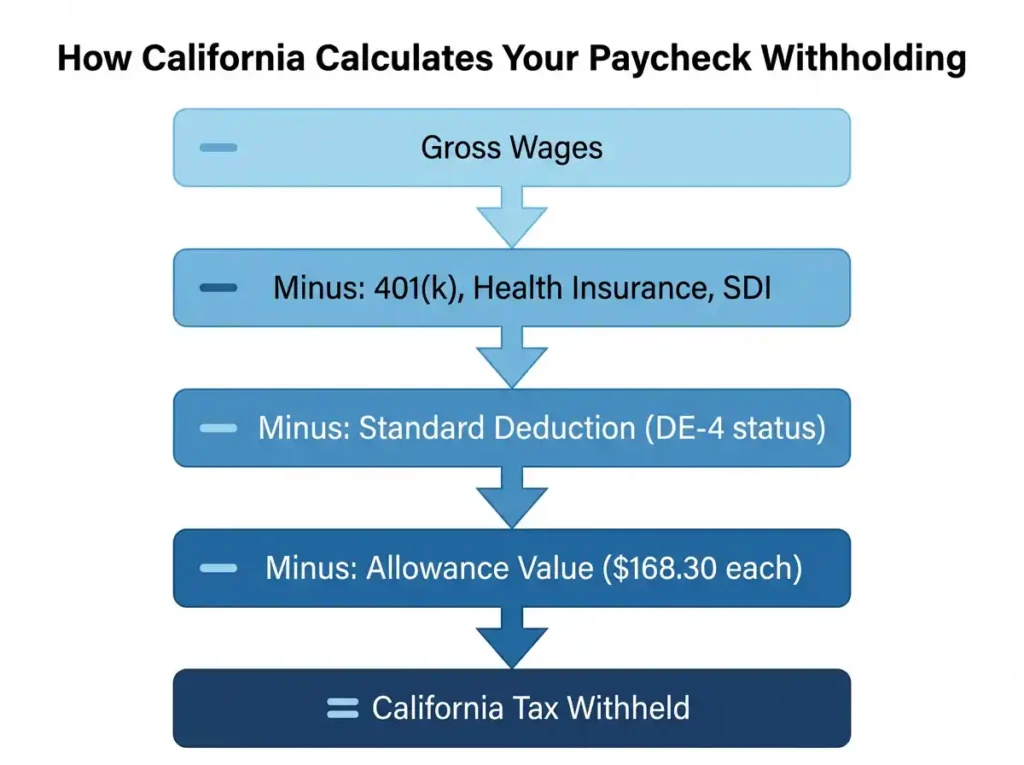

What the Form DE-4 Actually Does

The California Employment Development Department (EDD) uses your Form DE-4 to tell your employer how much state tax to withhold from every paycheck. Unlike the federal W-4, which overhauled its allowance system in 2020, California’s DE-4 still uses a traditional allowances system. Each allowance is worth approximately $168.30 annually in reduced withholding.

The Dual-Income Trap on the DE-4

Here is the most expensive mistake we see married couples make. Both spouses claim “Married” status on their DE-4. Each employer withholds at a lower rate because they assume a one-income household. But California’s progressive brackets combine that income at filing time. The result is a surprise bill every April.

The fix is simple. If both spouses work, both should select “Single or Married (with two or more incomes)” on their DE-4. For a full walkthrough of every section, see our step-by-step guide on how to fill out your California Form DE-4. No surprise. No penalty. No stress.

The 10-Step Withholding Calculation Overview

The EDD provides two methods for employers: Method A (Wage Bracket Table) and Method B (Exact Calculation Method). Both start with these core steps:

- Subtract nontaxable contributions like 401(k) or health insurance premiums from gross wages. Note that the California SDI rate for 2026 is also deducted at this stage.

- Apply the standard deduction based on DE-4 filing status.

- Subtract allowance value based on the number of allowances claimed.

- Apply the progressive tax brackets to the remaining taxable wages.

- This produces the estimated state withholding amount per pay period.

Takeaway: Update your DE-4 any time your income, filing status, or household situation changes. It is the single fastest way to prevent a surprise tax bill.

Deductions and Credits That Reduce Your Tax

California Standard Deduction: What You Need to Know

The California standard deduction for 2026 for the 2025 tax year (filed in 2026) is $5,706 for single filers and $11,412 for Married Filing Jointly. This is also the amount available for Head of Household filers.

Do not confuse this with the federal standard deduction, which is dramatically higher. This is the Nonconformity Gap in action. Most California filers use the standard deduction because their itemized deductions do not exceed these amounts. But higher-income homeowners in expensive areas often benefit from itemizing.

California Tax Credits: Your Most Powerful Tool

Refundable Credits are the most valuable because they can generate a payment from the FTB even if your tax bill is already zero.

- CalEITC (California Earned Income Tax Credit): Up to $3,756 for tax year 2025. Available to workers earning up to $32,900. This credit is especially valuable for workers near the California minimum wage for 2026. NerdWallet’s California state income tax guide also covers eligibility rules for this credit in detail.

- Young Child Tax Credit (YCTC): Up to $1,189 for families with children under six. Recently expanded to include families with zero earned income if total wages stay under $35,640.

- Foster Youth Tax Credit (FYTC): Up to $1,189 for former foster youth aged 18 to 25. Claimed on Form FTB 3514.

Non-Refundable Credits reduce your bill to zero but do not generate a refund.

- California Renter’s Tax Credit: $60 for single filers, $120 for joint filers, for qualifying lower-income renters.

- Senior Head of Household Credit: Up to $1,860 for individuals over 65 who meet income and dependency requirements.

- California Competes Tax Credit (CCTC): Available for businesses that expand or create jobs within California.

| Credit | Maximum Amount | Refundable? |

| CalEITC | $3,756 | Yes |

| Young Child Tax Credit (YCTC) | $1,189 | Yes |

| Foster Youth Tax Credit (FYTC) | $1,189 | Yes |

| Renter’s Tax Credit | $120 | No |

| Senior HoH Credit | $1,860 | No |

| Film Production Credit | 25% to 35% of spend | No |

Key Limitations on Deductions

California applies its own “6% Rule” for high earners. Itemized Deductions (Schedule CA) get reduced by the lesser of 6% of the amount by which federal AGI exceeds a state threshold, or 80% of total allowable deductions. This creates a double limitation when combined with the federal IRC Section 68 phaseout.

One huge difference from federal rules: California does not conform to the federal SALT Deduction Cap ($40,000 under OBBBA updates). A homeowner paying $25,000 in property taxes can only deduct $10,000 on their federal return. But on their California return, they may deduct the full amount (subject to the 6% state phaseout rule). This “SALT Workaround” is one of the most valuable planning opportunities for California homeowners.

Takeaway: Credits beat deductions. Always check your credit eligibility before filing.

Special Situations That Affect Your California Taxes

Capital Gains Tax Rates in California

Here is something that surprises many investors. California taxes capital gains as ordinary income. There is no separate lower rate for long-term capital gains like there is at the federal level. A $100,000 capital gain is treated exactly like a $100,000 salary by the FTB.

This means an investor in the 9.3% bracket pays 9.3% on their gains at the state level, on top of the federal 15% or 20% capital gains rate. Smart year-end planning around loss harvesting is essential for California investors with significant taxable portfolios.

Alternative Minimum Tax (AMT) in California

California has its own Alternative Minimum Tax (AMT) system that operates separately from the federal AMT. High-income earners with large deductions or stock option income may trigger the state AMT. The California AMT rate is 7% and applies to a broader base of income after adding back certain deductions.

If you exercise incentive stock options, receive large accelerated depreciation, or use significant tax preference items, check your exposure to the California AMT before year-end.

Residency Rules and Non-Resident Income

Thousands of people move in and out of California each year. The FTB is aggressive about residency audits. If you lived in California for any part of the year, you likely need to file Form 540NR as a part-year resident. This form requires you to prorate your income and credits based on the portion of the year you lived in the state.

California taxes non-resident income that is “sourced” to the state. If you work remotely for a California company while living in another state, you may still owe California income tax on that income. This area of non-resident income has become a major flashpoint, especially as high-net-worth migration out of California has accelerated.

Takeaway: Residency status determines your filing form. Get it right to avoid an expensive FTB audit.

Exclusive Insight: The HSA Trap Most Californians Miss

Pro Secret: California Does Not Recognize HSA Tax Benefits

This is the one that catches even smart, well-prepared taxpayers completely off guard. At the federal level, a Health Savings Account gives you three tax advantages: contributions are deductible, growth is tax-free, and withdrawals for medical expenses are tax-free. It is called the “triple-tax-advantage.”

California does not conform to federal HSA rules. Contributions to your HSA are not deductible on your California state return. Earnings inside the account are taxed every year as ordinary income. This “HSA Trap” can add hundreds of dollars to your state tax bill annually, and most people never see it coming until we flag it for them. If you contribute the maximum family amount of $8,550 per year to an HSA, you could owe an extra $800 or more in California tax that you never planned for.

Takeaway: HSAs are great for federal taxes. For California, they are just a regular account. Plan accordingly.

Smart Strategies to Legally Reduce Your California Tax Bill

In our view, most Californians leave real money on the table because they do not plan ahead. Here are the strategies that have made the biggest difference for our clients.

Maximize retirement contributions. Contributions to a 401(k) or traditional IRA reduce your federal adjusted gross income. Because California generally conforms to federal retirement account rules (unlike HSAs), these contributions also reduce your California taxable income. Every dollar you shelter in a 401(k) at the 9.3% bracket saves you 9.3 cents in state tax.

Time your income and deductions strategically. If you expect to be in a lower tax bracket next year, defer bonuses or capital gain realizations where possible. Conversely, if you expect your income to spike in 2026, accelerating deductible expenses into 2025 can reduce your 2025 liability. This kind of income deferral planning is where having a multi-year view pays off.

Understand the pass-through deduction gap. California does not conform to the federal Section 199A deduction, which allows eligible S-Corp and LLC owners to deduct 20% of qualified business income at the federal level. California taxes 100% of that income at the state level. Business owners need to factor this into their entity structure planning.

Track all eligible business expenses. Freelancers and self-employed individuals can reduce their CA AGI directly through legitimate business deductions. Home office, equipment, software subscriptions, and professional development costs all reduce your taxable income before you even apply the bracket math.

Takeaway: The best tax reduction happens before December 31, not on April 14.

Knowledge Solves Problems: Your One-and-Done California Tax Answer

We know exactly why you are here. You got your paycheck, saw the California tax withholding line, and felt that familiar knot in your stomach. Or maybe you just moved here and heard the 13.3% headline and panicked. Either way, you are not alone. We have seen this exact moment of confusion thousands of times.

The Real Problem Most Guides Miss

Most tax content shows you a bracket table and walks away. That does not solve anything. The real frustration is not the rate. It is not knowing what you will actually owe. And it is not knowing if you are doing something wrong that is costing you money.

The Effortless Fix

Here is the direct answer. Take your gross income. Subtract your California standard deduction ($5,706 single, $11,412 joint). Apply each bracket rate only to the income that sits within that bracket’s range. Add up the layers. That number is your estimated California tax liability before credits.

Then subtract any credits you qualify for. CalEITC alone can erase hundreds or thousands of dollars from that number. The result is what you actually owe. It is almost always far lower than the scary marginal rate suggests.

Why This Fix Works Every Time

This method is exactly what the California Franchise Tax Board (FTB) uses on Form 540. It is not a trick or a shortcut. It is the official calculation. Once you run it once, the fear goes away permanently. You stop reacting to headlines and start making real financial decisions based on your personal numbers.

This is your permanent fix. Run the calculation once, and you will never feel confused by California taxes again.

California FTB and Official Filing Reference

Key Terms and Technical Reference

| Term | Definition |

| Franchise Tax Board (FTB) | California state agency that administers personal income tax |

| California Taxable Income | Income after deductions and adjustments used to apply brackets |

| Marginal Tax Rate | The rate applied to your last dollar of income |

| Effective Tax Rate | The average rate paid across all income |

| Progressive Tax System | System where higher income portions are taxed at higher rates |

| Tax Conformity | Whether California follows federal tax law changes |

| California Consumer Price Index (CCPI) | Measure used to adjust brackets annually for inflation |

| Inflation Indexing | Annual bracket adjustment to prevent bracket creep |

| California Adjusted Gross Income (CA AGI) | Starting point for California tax calculation |

| Mental Health Services Act Tax (MHSA) | Former name for the 1% Millionaire Surcharge |

| Behavioral Health Services Act (BHSA) | Current name for the 1% surcharge on income over $1M |

| Tax Liability | The total amount of tax you owe |

| Withholding (Form DE-4) | Employee form for California state tax withholding |

| Estimated Tax Payments | Quarterly payments for those not subject to withholding |

| Non-refundable Credits | Credits that reduce tax to zero but cannot produce a refund |

| Refundable Credits | Credits that can produce a payment even with zero tax |

| Revenue Procedure | IRS guidance document establishing official tax parameters |

| Personal Exemption Credit | California credit reducing tax for each qualifying taxpayer |

| Tax Year 2026 | Income earned January 1 through December 31, 2026 |

| April 15 Deadline | Standard due date for California and federal returns |

| Six-month Extension | Automatic extension to October 15 for filing (not payment) |

| Income Thresholds | The dollar amounts that define bracket boundaries |

| Form 540 | Standard California resident income tax return |

| Form 540NR | California nonresident or part-year resident tax return |

California FTB Official Resources

To confirm your filing status and bracket figures directly with the source, use these official touchpoints:

- California Franchise Tax Board (FTB) official site for Form 540 and all tax tables. Bookmark the latest FTB tax news and updates for any mid-year legislative changes.

- California Employment Development Department (EDD) for updated withholding tables and the Form DE-4

- Internal Revenue Service (IRS) for federal bracket tables and the OBBBA updates

Takeaway: Always verify bracket figures at ftb.ca.gov. Tax law changes and official FTB numbers are the final word.

The Holistic California Tax Burden: Beyond Income Tax

One thing our long-term clients always appreciate is that income tax is not the only tax Californians pay. Here is the full picture for 2026.

| Tax Category | Rate / Amount | Notes |

| State Sales Tax | 7.25% Base | Can reach 10.75% with local additions |

| Property Tax | 0.7% Effective Average | Ranges 0.26% to 0.89% by county |

| Gasoline Tax | $0.612 per gallon | Adjusted every July 1 |

| Diesel Tax | $0.466 per gallon | Adjusted every July 1 |

| Alcohol (Spirits) | $3.30 to $6.60 per gallon | Based on alcohol proof |

| Vehicle Tax | 7.25% plus local | Applied to purchase or use |

Many people stop the comparison at income tax. But a complete cost of living offset analysis must include sales, property, and excise taxes. For a lower-income family, California’s CalEITC can actually produce a lower total burden than some “no income tax” states. Run the full numbers before making any relocation decision.

Takeaway: Your total California tax burden includes sales, property, and excise taxes. Run the full comparison before making relocation decisions.

Quick Summary Cheat Sheet

Here is everything you need to remember, all in one place.

- Only your last dollar is taxed at your top marginal rate. Every dollar below that is taxed at lower rates.

- Your effective tax rate reflects your real burden. It is always lower than your marginal rate.

- California’s standard deduction is far lower than federal. Single filers: $5,706 state vs. $16,100 federal for 2026.

- California does not cap SALT deductions. You can deduct more property tax on your state return than your federal return.

- HSAs are taxed by California. This is one of the most missed planning details for state residents.

- The 1% Behavioral Health Services Act surcharge applies above $1,000,000. The real top rate is 13.3%, not 12.3%.

- Refundable credits like CalEITC can generate a payment from the FTB. Check eligibility every year.

- The April 15 Deadline applies to both state and federal returns. A six-month extension to October 15 is available for filing only, not for payment.

Frequently Asked Questions: Deep Dive

What Is the Highest California Tax Rate in 2026?

The highest standard marginal rate is 12.3%, applied to California taxable income above $742,954 for single filers and above $1,485,907 for those married filing jointly. However, income over $1,000,000 triggers the 13.3% Mental Health Services Act Surcharge (now formally the Behavioral Health Services Act surcharge). For very high earners, 13.3% is the true top rate.

At What Income Do the Higher Brackets Apply for California 2026?

For the california state income tax brackets 2026, the 10.3% bracket starts at $371,480 for single filers. The 11.3% bracket starts at $445,772. The 12.3% bracket begins at $742,954. These are the thresholds for the 2025 tax year returns filed in spring 2026 based on the latest FTB data and CCPI inflation adjustments.

Do California Tax Brackets Change Every Year?

Yes. The California Franchise Tax Board adjusts income thresholds each year based on the California Consumer Price Index (CCPI). This process of inflation indexing prevents bracket creep. The rates themselves (1% through 12.3%) have remained stable for several years, but the income ranges that trigger each rate shift slightly upward with inflation.

How Do We Calculate Our Effective Tax Rate?

Divide your total California tax owed by your total gross income. For example, if you owe $4,200 in California tax on a $90,000 income, your effective rate is 4.67%. The FTB publication for Form 540 includes tax computation worksheets that walk you through this calculation step by step.

Are Bonuses Taxed Differently in California?

At the state level, bonuses are subject to a flat supplemental withholding rate of 10.23%. This is a withholding rate, not your actual tax rate. When you file your return, the actual tax on your bonus is calculated using the same progressive brackets as your regular income. If too much was withheld, you get a refund. If too little was withheld, you owe the difference.

Can Deductions Lower My Tax Bracket?

Yes, deductions lower your California taxable income, which can move you into a lower bracket. If your gross income puts you in the 9.3% Tax Bracket but your itemized deductions or retirement contributions bring your taxable income below $72,725, your marginal rate drops to 8%. This bracket shift is one of the most valuable benefits of year-end deduction planning.

Does California Tax Social Security Benefits?

No. Social Security benefits are fully exempt from California state income tax. This is a meaningful benefit for retirees, and it is one area where California is actually more favorable than many states.

What Is the California FTB Millionaire Tax Threshold?

The 1% Millionaire Surcharge applies to California taxable income over $1,000,000 for any filing status. At this level, the combined state rate becomes 13.3%. This is the highest top marginal income tax rate of any state in the nation, making advanced planning critical for those approaching this income threshold.

Final Takeaway: What Actually Matters

We want to leave you with the mindset that has served our clients best over the past 8 years. Stop focusing on the headline 13.3% and start focusing on your personal effective tax rate.

A single teacher earning $65,000 in Sacramento pays a California effective rate of around 3.5%. A tech worker in San Jose earning $200,000 pays around 7.5%. A hedge fund manager in Beverly Hills earning $2,000,000 pays close to 12.8% on the state level alone. The progressive tax system in California is designed to ensure that tax liability rises with income. And for most residents, the actual burden is far more manageable than the scary headlines suggest.

Understanding how the California Franchise Tax Board applies tax brackets, how the california state income tax rates 2026 compare to federal rates, and how credits like the CalEITC and YCTC work together gives you real financial power. It lets you plan, not just react.

Use Form 540 to file your state return accurately. Use Form 540-ES to make estimated tax payments if you are self-employed. Adjust your Form DE-4 with your employer if your life situation changed. Check your eligibility for every credit available to you. And if your income is approaching $1,000,000, start planning for the Behavioral Health Services Act surcharge well before year-end.

The goal is not to pay zero tax. The goal is to pay exactly what you owe and not a single dollar more.

You now have the complete roadmap. Use it.

“I used to think I was in the 9.3% bracket and paying 9.3% on everything I made. Once I ran the actual layered calculation, I realized my effective rate was under 5%. That one conversation saved me from making a terrible decision to leave the state.”

— Marcus T., software engineer, San Jose, CA

That shift in understanding is exactly the game-changer we want for every person who reads this guide.

All data sourced from the California Franchise Tax Board (FTB), Internal Revenue Service (IRS), and California Employment Development Department (EDD). Bracket figures reflect the 2025 tax year returns filed in 2026 with CCPI inflation adjustments. Consult a qualified California tax professional for advice specific to your situation.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.