On a $150,000 salary in California, most single filers take home between $97,000 and $103,000 per year after federal income tax, California state income tax, Social Security, Medicare, and SDI. That is roughly 65 to 69 cents kept for every dollar earned. California alone costs $14,800 to $15,800 in state income tax, one of the highest burdens in the country. That said, your actual take-home depends on filing status, pretax contributions, and payroll deductions, which can shift the number by thousands in either direction. Use the California paycheck calculator to run your specific numbers.

Quick Answer — What Is $150K After Taxes in California?

Estimated Net Income at a Glance

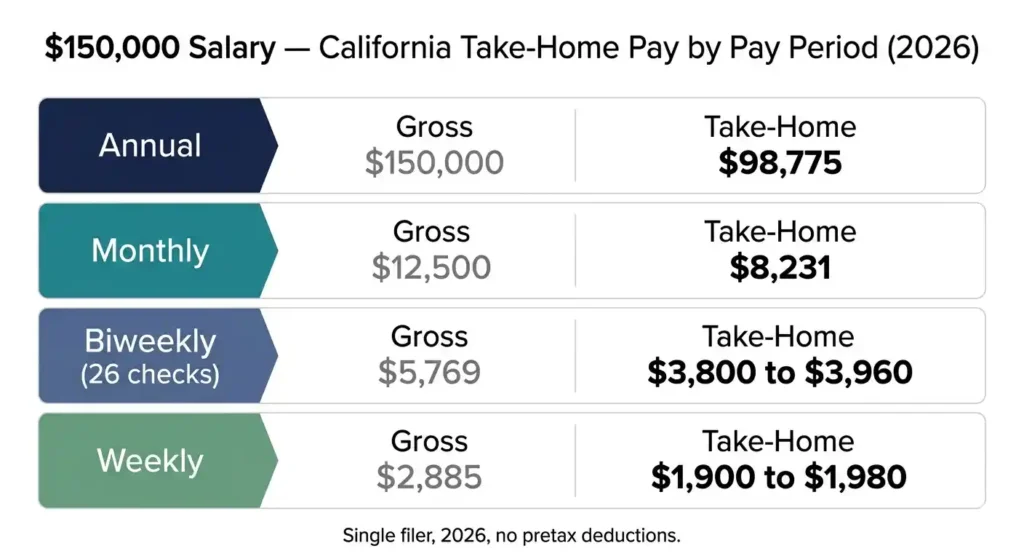

For a single filer using the 2026 standard deduction and no retirement contributions: annual take-home is $99,000 to $103,000, monthly is $8,250 to $8,580, biweekly is $3,800 to $3,960, and weekly is $1,900 to $1,980.

Why Your Results May Be Different

Filing status, pretax 401(k) or HSA contributions, health insurance payroll deductions, and W-4 withholding choices all shift your net pay, sometimes by thousands per year. These estimates are a baseline. Your real paycheck reflects your specific situation. If you want to understand every line on your stub, this guide on how to read a California pay stub in 2026 breaks down exactly what each deduction means.

How Taxes Reduce a $150,000 Salary in California

Four separate taxes hit your paycheck: federal income tax, California state income tax, FICA, and SDI. For a full breakdown of every California payroll tax rate in 2026, the state EDD publishes official figures each December.

Federal Income Tax Breakdown

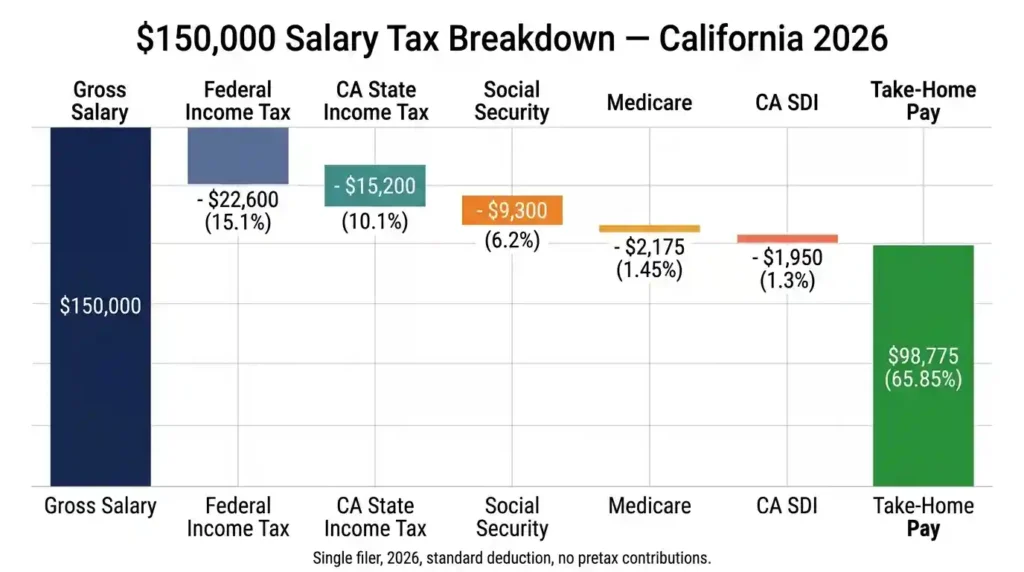

The U.S. tax system is progressive, meaning only income inside each bracket gets taxed at that rate. For 2026, a single filer subtracts the $16,100 standard deduction from $150,000, leaving $133,900 in taxable income (AGI). Brackets: 10% on the first $11,925, 12% up to $48,475, 22% up to $103,350, then 24% on the rest. Total federal tax runs $22,600 to $24,200. Effective federal rate: 15.6 to 16.1%. The 24% marginal rate applies only to the top slice. The IRS withholding estimator at irs.gov helps you verify your own withholding is accurate.

Overtime dollars stack on top of your existing income and get taxed at your highest marginal rate, 24% federal plus 9.3% to 10.3% California, putting overtime near 35% combined or higher. For a detailed look at how California handles overtime pay rules, see California overtime laws 2026.

California State Income Tax

California runs 10 brackets from 1% to 13.3%. At $150,000, most income falls in the 9.3% bracket with a portion in the 10.3% bracket. After the $5,540 California standard deduction, taxable state income is roughly $144,460. State tax owed: $14,800 to $15,800. Every dollar of income gets taxed at something, no rate applies only to income above a threshold. For the full rate schedule, see the California tax brackets 2026 guide.

Social Security and Medicare Taxes

Social Security is 6.2% on wages up to $184,500 in 2026, per the Social Security Administration. On $150,000, that is $9,300. Medicare is 1.45% on all wages, adding $2,175. The Additional Medicare Tax of 0.9% kicks in above $200,000 for single filers, below that threshold here. Total FICA: $11,475.

California SDI Contributions

SDI is 1.3% on all wages with no cap in 2026, per the California EDD. On $150,000 that is $1,950 per year, or roughly $75 per biweekly paycheck. It funds short-term disability and Paid Family Leave coverage. For the complete rate history and benefit details, read the CA SDI rate 2026 guide.

$150K Salary to Paycheck Conversion

Some employers run semimonthly payroll, 24 paychecks instead of 26. On that schedule, gross per check is $6,250 and after-tax net is approximately $4,085 to $4,245. The annual salary calculator converts any salary to monthly, biweekly, weekly, and hourly net figures automatically.

Annual to Monthly Pay

Gross monthly: $12,500. After-tax monthly for a single filer: $8,250 to $8,580.

Annual to Biweekly Pay

Gross biweekly: $5,769. After-tax biweekly for a single filer: $3,800 to $3,960.

Annual to Weekly Pay

Gross weekly: $2,885. After-tax weekly: $1,900 to $1,980.

Annual to Hourly Equivalent

Gross hourly on a 40-hour week: $72.12. Net hourly after all taxes: $47 to $50. For comparison, see what a lower wage looks like after taxes. The 40 an hour is how much a year post shows the full breakdown at $83,200 gross.

How Retirement Contributions Change Take-Home Pay

Pretax contributions lower your taxable income, cutting both federal and California state tax bills. Browse the full paycheck scenarios category for more contribution comparison examples.

No Retirement Contributions

Federal taxes: $22,600. California state taxes: $15,200. FICA: $11,475. SDI: $1,950. Total: $51,225. Annual take-home: $98,775, or $8,231 per month.

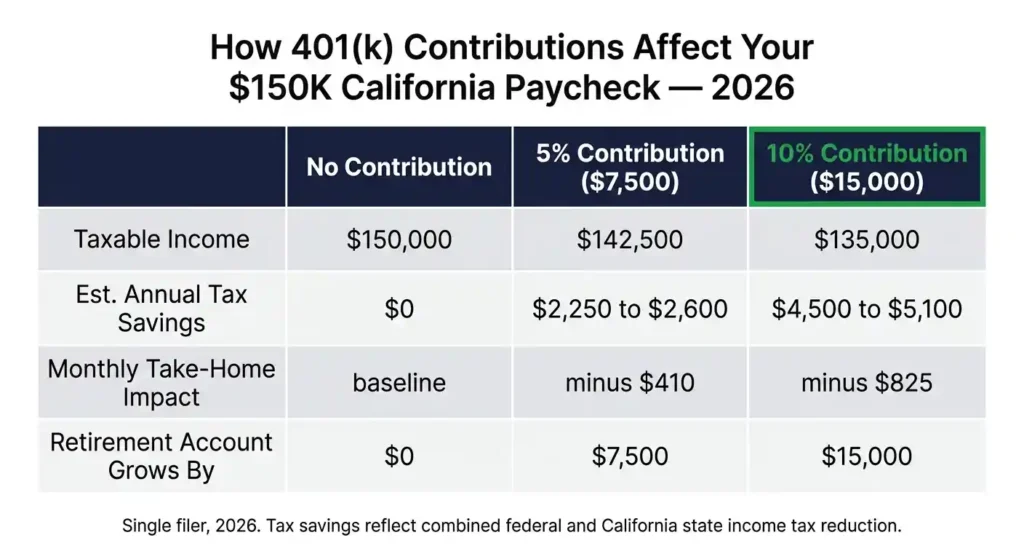

Contributing 5% to a 401(k)

A $7,500 pretax contribution saves $2,250 to $2,600 in combined income taxes. Monthly net pay drops about $410, but $7,500 goes into retirement. The real cost to your paycheck is far less than the contribution.

Contributing 10% to a 401(k)

A $15,000 contribution saves $4,500 to $5,100 in income taxes. Monthly take-home drops roughly $825. The 2026 employee limit is $24,500 for workers under 50, so a 10% contribution still leaves room to contribute more.

HSA and FSA Contributions

HSA limits in 2026: $4,400 individual, $8,750 family. Healthcare FSA: $3,400. Dependent care FSA: $5,000. All reduce taxable income like a 401(k). The HSA contribution limits 2026 guide shows exactly how the tax savings stack up by income level. The IRS publishes official HSA limits annually through IRS Notice 2025-19.

A Traditional IRA allows up to $7,500 per year ($8,500 if 50 or older). At $150,000 with a workplace 401(k), the deduction phases out between $81,000 and $91,000 of modified AGI, so most earners at this level cannot deduct it. A Roth IRA is fully available at $150,000: the 2026 phase-out for single filers starts at $153,000 and ends at $168,000, so a full $7,500 contribution is allowed.

RSUs vest as ordinary income in the year they vest, taxed at your full marginal rates. A $20,000 RSU tranche stacks on top of $150,000, pushing more income into the 24% federal and 10.3% California brackets. Bonuses follow the same logic. For a full breakdown of how California taxes bonus income, see the California bonus tax rate guide. Employers withhold 22% on supplemental wages by default, and the actual rate at filing depends on your total income.

Is $150K a Good Salary in California?

Short Answer

Yes, $150,000 places you in roughly the top 15 to 18% of individual earners statewide. But purchasing power depends heavily on where you live.

For a Single Person

After taxes, take-home is about $8,250 per month. In Sacramento or Fresno, a two-bedroom runs $1,600 to $2,000, leaving $4,000 to $4,500 for savings and lifestyle. An emergency fund is buildable within one to two years, and student loan payments are manageable alongside retirement contributions.

For a Couple

One income at $150,000 gives a couple solid footing, a mortgage in lower-cost areas, retirement savings, and manageable expenses. Strain increases if one partner stays home, especially in high-cost metros.

For a Family

Childcare averages $1,500 to $2,500 per child per month. Two kids can cost $3,000 to $5,000 monthly in childcare alone. Add a mortgage, car, and healthcare in LA or the Bay Area and $150,000 feels tight. In lower-cost cities, it is more workable.

Can You Live Comfortably on $150K in California?

Comfort depends almost entirely on your city and housing situation.

Housing Costs

Renting

San Francisco one-bedroom: $3,100 to $3,500. Los Angeles: $2,200 to $2,800. Sacramento or Fresno two-bedroom: $1,500 to $2,000. The 30%-of-gross rule puts your ceiling at $3,750. Most California cities stay under that. San Francisco is the exception.

Buying a Home

California median home price: $800,000 to $900,000. A 20% down payment on $800,000 is $160,000. The mortgage on $640,000 at 6.5% runs about $4,045 per month, nearly half of take-home pay for a single filer. Most lenders cap total debt payments at 43% of gross monthly income, or about $5,375. Buying solo is tight without a larger down payment or second income.

Transportation Costs

Gas averages $4.50 to $5.00 per gallon in California in 2026. Car payment, insurance, and fuel combined: $900 to $1,400 per month. Transit in San Francisco and parts of LA can cut that significantly.

Healthcare Costs

Employee-only coverage: $200 to $500 per month after employer contributions. Family coverage adds $600 to $1,200 per month. Out-of-pocket costs vary by plan and usage.

Savings and Investing

After housing, transportation, and healthcare, a single earner can realistically save $2,000 to $3,500 per month, enough to max a 401(k), build an emergency fund, and still invest in a brokerage account.

$150K Salary Across California Cities

San Francisco Bay Area

Median one-bedroom rent is $3,200. After housing, food, and transportation, $150,000 is comfortable but not lavish. Homeownership requires a second income or a very large down payment. The San Francisco paycheck calculator can model your exact net pay in the Bay Area.

Los Angeles

More varied than San Francisco. The Valley and Long Beach are affordable; West Hollywood and Culver City are not. Renting is manageable. Buying solo requires planning and flexibility. Use the Los Angeles paycheck calculator to see how local costs affect your real take-home.

San Diego

One-bedroom rents: $2,400 to $2,700. Median home prices around $800,000. Strong job market in defense, biotech, and tech. Cost is high but quality of life offsets it for many earners.

Sacramento

Most affordable major California city at this income. Two-bedroom rents: $1,600 to $1,900. Median home prices: $450,000 to $500,000. Homeownership is within reach. $150,000 goes significantly further here than in the Bay Area. The Sacramento paycheck calculator shows the exact difference.

Orange County

Median home prices: $900,000 to $1 million. One-bedroom in Irvine or Newport Beach: $2,500 to $3,200. Comfortable as a renter, demanding as a buyer.

California vs Other States on a $150K Salary

Moving out of California is not always the financial win people expect.

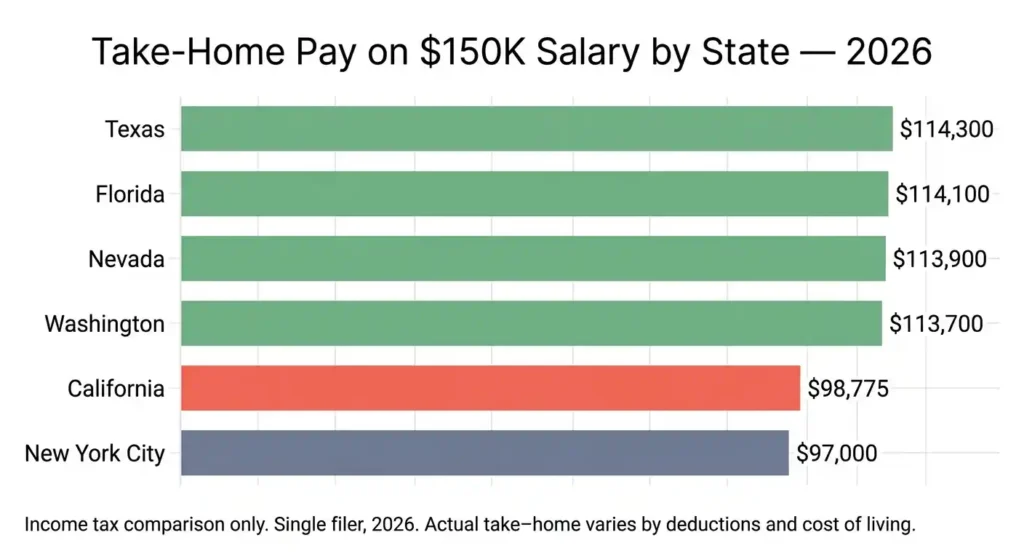

California vs Texas

Texas has no state income tax, saving $14,800 to $15,800 annually versus California. But Texas property taxes average 1.6 to 2.0% of home value, versus California’s 1.1% under Proposition 13. The gap narrows over time for homeowners.

California vs Florida

Florida has no state income tax, same savings as Texas. Housing costs have risen sharply since 2021, and home insurance premiums in hurricane zones are significant. Net savings after cost of living may be less than the tax difference suggests.

California vs Nevada

Nevada has no state income tax, saving about $14,800 per year. Lower home prices and modest property taxes. Works well for remote workers who no longer need to be in California physically.

California vs Washington

Washington has no income tax, saving $14,800 to $15,800 per year. Seattle home prices are high but below San Francisco. A common move for tech workers.

New York state tax on $150,000 runs about 6.8%, plus NYC tax of up to 3.876% for city residents. A California earner actually keeps slightly more than a NYC resident at this income. Purchasing power in both cities is similarly strained by housing costs.

Real Paycheck Examples for Different Tax Situations

Single Filer with Standard Deduction

Federal: $22,600. California: $15,200. FICA: $11,475. SDI: $1,950. Total taxes: $51,225. Take-home: $98,775 per year, or $8,231 per month. For a side-by-side look at how this compares at a lower income level, see 100k after tax in California and 120k after taxes California.

Married Filing Jointly

The 2026 federal standard deduction for married filers is $32,200. Federal tax drops to $15,800 to $16,500. Total taxes fall to roughly $41,000 to $43,000. Annual take-home: $107,000 to $109,000.

Married filing separately is almost always worse. It eliminates certain credits, disqualifies the student loan interest deduction, and typically raises the combined tax bill. File jointly unless a specific situation makes separate filing necessary.

Head of Household

Standard deduction: $24,150 in 2026. Applies to unmarried individuals supporting a qualifying child. Federal tax: $19,500 to $21,000. Annual take-home: $101,000 to $103,500.

Employee with Dependents

The Child Tax Credit is $2,200 per qualifying child in 2026. Two children can reduce tax owed by $4,400. Claiming dependents on your W-4 reduces withholding throughout the year instead of waiting for a refund. The California Earned Income Tax Credit is another credit worth checking at this income level.

Real-World Scenarios People Face at $150K

Evaluating a Job Offer

Net pay after California taxes runs $97,000 to $103,000, that is the number that matters, not the gross. A $150,000 offer with a 4% 401(k) match and full benefits beats a $155,000 offer with neither.

If one offer is a 1099 contract, the math changes significantly. A contractor pays self-employment tax of 15.3%, covering both sides of FICA. That is roughly $21,195 versus $11,475 for a W-2 employee. A contractor needs $160,000 to $165,000 to match a $150,000 salaried employee’s take-home. For a full comparison of what each classification actually costs you, see 1099 vs W-2 tax California. The worker classification category covers all related topics.

Relocating to California

Moving from a no-income-tax state cuts take-home by $1,230 to $1,315 per month. Negotiate salary before your start date, California employers in tech, finance, and healthcare typically factor this in.

California taxes income earned while working physically in the state, regardless of where your employer is based. Remote workers splitting time between states may need to file in both. Consult a tax professional before any mid-year move.

Deciding Between Two Job Offers

A $10,000 401(k) match is worth nearly $7,000 after accounting for taxes you would have paid on that money. A fully remote role that eliminates a $600 monthly commute adds $7,200 in annual value. Gross salary is a starting point, not the whole picture.

Planning a Home Purchase

At $150,000, lenders typically approve $450,000 to $550,000 using a 43% debt-to-income limit. That buys in the Central Valley, Inland Empire, and parts of Sacramento, not most coastal markets. To buy an $800,000 to $900,000 home, you need a larger down payment, minimal debt, or a co-borrower.

Common Mistakes People Make When Estimating Take-Home Pay

Assuming Tax Brackets Tax All Income

Only income inside each bracket is taxed at that rate. The 24% bracket applies to the top slice above $103,350 of taxable income, not to all $150,000. Effective federal rate at $150,000: about 15.6%.

Ignoring Payroll Deductions

Calculators show income taxes. Your actual paycheck also loses health insurance premiums, dental, vision, life insurance, and parking benefits. A worker paying $400/month for family coverage takes home $4,800 less per year than someone on individual coverage. Learning why your paycheck is so low can help identify which deductions are the culprit.

Confusing Tax Refunds with Taxes Owed

A refund means you overpaid, not that you paid less. Adjusting your W-4 puts that money in your paychecks year-round instead. The total tax bill does not change. Only the timing does. You can also check your California tax refund status directly through the FTB.

Using Generic Salary Calculators

Many calculators use outdated SDI rates, miss California-specific brackets, or ignore the Additional Medicare Tax. Use a California paycheck calculator with 2026 IRS tax tables. Two coworkers at $150,000 can take home $1,500 more or less per month depending on their 401(k) elections, W-4 claims, and health plan choices.

Ways to Increase Your Take-Home Pay Legally

Optimize W-4 Withholding

If you get large refunds, you are over-withholding. A revised W-4 takes five minutes and raises every paycheck immediately. Use the IRS Tax Withholding Estimator at irs.gov. California also requires a separate DE-4 form for state withholding. The California DE-4 form guide walks through every field.

Maximize Pretax Contributions

The 2026 401(k) limit is $24,500 for workers under 50. At a combined 33% marginal rate, maxing it saves $8,085 in taxes. Add a $4,400 HSA and save another $1,452. Combined savings: over $9,500. The CalSavers mandate is another retirement option for workers whose employer does not offer a 401(k).

Review Employer Benefits

Commuter benefits cover $325/month pretax. Employer life insurance up to $50,000 is tax-free. Dependent care FSA covers $5,000 pretax. Unused benefits are unclaimed tax savings. The paycheck basics category covers pre-tax and post-tax deductions in more depth.

Strategic Tax Planning

Bunching charitable deductions in alternating years can push you above the standard deduction, creating a larger itemized deduction. Time major deductible expenses before year-end to cut California tax liability.

Side income and commission add to your taxable base. Earnings above a few thousand dollars may require quarterly estimated tax payments to the IRS and California Franchise Tax Board (FTB). Use a 2026 tax estimator mid-year to avoid an April surprise.

Frequently Asked Questions

What is $150K after taxes in California per month?

Single filers take home $8,150 to $8,580 per month. The typical annual range is $98,000 to $104,000, based on 2026 IRS and FTB rates.

What is $150K after taxes in California biweekly?

Each biweekly paycheck runs $3,800 to $3,960 after all taxes, based on 26 pay periods and no pretax deductions.

Is $150K considered upper middle class in California?

By percentile, yes, top 15 to 18% of individual earners statewide. In San Francisco or Los Angeles, it can feel squarely middle class given housing costs.

Can a family live comfortably on $150K in California?

In Sacramento or Fresno, yes. In San Francisco or coastal LA, it is tight, especially with two children in childcare at $1,500 to $2,500 each per month.

How much tax do you pay on $150K in California?

Federal: $22,600. California: $15,200. Social Security: $9,300. Medicare: $2,175. SDI: $1,950. Total: $51,225. Effective total tax rate: 34.2%.

How can I reduce taxes on a $150K salary?

Max your 401(k) at $24,500, saves over $8,000 in combined taxes. An HSA saves another $1,450. Adjust your W-4 to stop over-withholding.

Why is my paycheck lower than online calculators show?

Calculators model taxes only. Your paycheck also deducts health, dental, vision, life insurance, and 401(k) contributions, easily $500 to $2,000 per month extra.

Is $150K enough to buy a house in California?

In the Central Valley and Sacramento, yes. In San Francisco, LA, and San Diego, where prices run $750,000 to over $1 million, you typically need a co-borrower or a down payment well above 20%.

Final Takeaway — What $150K Really Means in California

Your real take-home is $98,000 to $103,000 per year, not $150,000. Federal taxes, California state tax, FICA, and SDI take roughly $51,000 off the top.

Inflation has cut the purchasing power of that number since 2020. Disposable income at $150,000 in Sacramento is genuinely strong. In San Francisco, the same salary leaves far less cost-adjusted income after housing and transportation.

Filing status, retirement contributions, and city of residence are the three variables that move the needle most. A married Sacramento renter maxing a 401(k) keeps meaningfully more than a single San Francisco renter who contributes nothing. Your gross sets the ceiling. Your choices determine what stays.

At $175,000, more income hits California’s 10.3% bracket and the federal 24% bracket deepens. At $200,000, the Additional Medicare Tax of 0.9% applies to income above that threshold. Every raise makes pretax planning more valuable. For a detailed look at what changes at higher salaries, the California payroll taxes category covers every rate and threshold that applies to California workers.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.