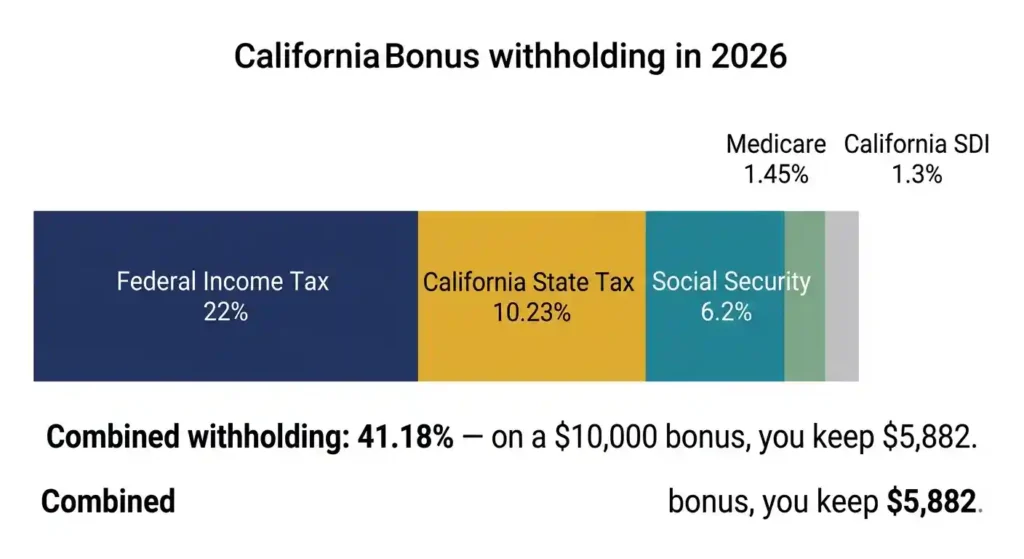

In California, a separately paid bonus is withheld at a combined rate of roughly 41.18% in 2026. That includes 22% federal, 10.23% state, 6.2% Social Security, 1.45% Medicare, and 1.3% SDI — all hitting the same check at once. A $10,000 bonus nets approximately $5,882 after withholding. That is not your final tax bill, though. It is a payroll estimate. Your actual liability gets settled when you file, and many employees get some of that withholding back as a refund. To see exactly how your regular paychecks are taxed alongside any bonus income, use the California paycheck calculator.

Quick Answer — How Much of Your Bonus Will You Actually Keep?

Typical California Bonus Withholding Breakdown

Federal: 22%. California: 10.23%. Social Security: 6.2% (on wages up to $184,500). Medicare: 1.45%. California SDI: 1.3%. Combined: roughly 41.18% before any voluntary deductions.

Estimated Net Bonus by Bonus Size

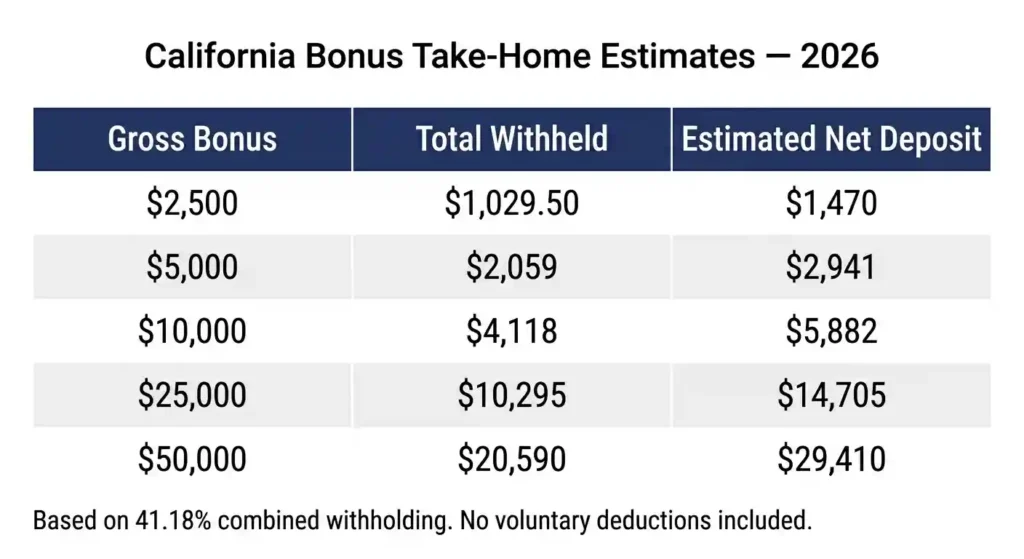

At a combined withholding rate of about 41%: a $1,000 bonus nets approximately $589. A $5,000 bonus nets $2,941. A $10,000 bonus nets $5,882. A $25,000 bonus nets $14,705. Actual deposits vary based on your W-4 elections, year-to-date wages, and employer payroll setup.

Timing matters too. A bonus paid in December 2026 lands on your 2026 Form W-2. One paid in January 2027 is 2027 income. If you are near a bracket threshold, that timing can shift your tax bill.

Are Bonuses Taxed Differently in California?

No. Your bonus is ordinary income, taxed exactly like your salary. What changes is how your employer withholds — and that is where the confusion starts. Withholding is just a deposit against what you will owe when you file, typically by the April deadline. Your actual tax is calculated then, based on your full-year income, deductions, and credits. Overpay and you get a refund. Underpay and you owe.

Bonus Tax vs Bonus Withholding

Withholding is what your employer sends to the IRS and California Franchise Tax Board on your behalf. Your actual tax liability is calculated later when you file. If you are in the 12% federal bracket and your employer withheld 22%, you overpaid. You get the difference back as a refund.

Also worth clearing up: a bonus does not push all your income into a higher bracket. Only the dollars above a threshold get taxed at the higher rate. Your effective tax rate — total tax divided by total income — stays well below your top marginal rate. For a full breakdown of how California income tax brackets work in 2026, see the guide to California tax brackets 2026.

Why So Much Tax Comes Out of Bonus Checks

When a bonus is paid separately, employers apply flat supplemental wage rates instead of the standard withholding tables used for your salary. California requires this flat-rate approach on separately identified bonuses. The rate feels higher, but your actual tax rate has not changed.

California Bonus Withholding Rates for 2026

California classifies bonuses as supplemental wages under the California Employer’s Guide (DE 44), published by the California Employment Development Department. The federal rules come from IRS Publication 15. Both require employers to withhold at set flat rates when bonuses are paid separately.

California Bonus Withholding Rate

California withholds 10.23% on bonuses and stock options paid separately in 2026. It applies to every separately paid bonus regardless of income level. Other supplemental wages that are not bonuses or stock options use a lower rate of 6.60%.

Federal Bonus Withholding Rate

The federal flat rate is 22% on supplemental wages up to $1 million per year. Above $1 million, anything over that threshold is withheld at 37%. Employers can also use the aggregate method — combining bonus and regular wages and applying standard tables — but most pay bonuses separately and use the flat rate.

Social Security and Medicare Taxes

Social Security is withheld at 6.2% on wages up to $184,500 in 2026. If you have already hit that cap before your bonus arrives, no Social Security is withheld from the bonus. Medicare is withheld at 1.45% with no cap. If your total wages exceed $200,000, an additional 0.9% Medicare tax applies to amounts above that threshold, pushing Medicare withholding to 2.35%. The IRS overview of FICA taxes explains both components in detail.

California SDI Withholding

SDI (State Disability Insurance) is withheld at 1.3% in 2026 with no wage cap, a rule in place since January 1, 2024. On a $5,000 bonus, that is $65. Small individually, but it adds to the combined total. For a deeper look at how SDI works and what it covers, see the full breakdown of the California SDI rate for 2026.

Why Your Bonus Check May Look Smaller Than Expected

Even after accounting for taxes, your deposit may still be lower than you expect. The reason is usually how the bonus was paid or what other deductions applied to that check.

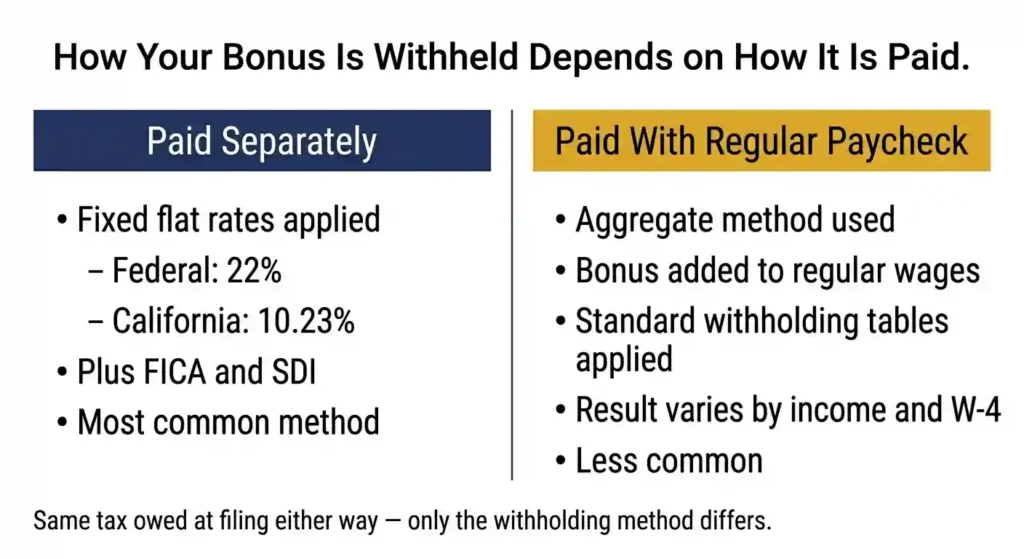

Bonus Paid Separately vs With Regular Paycheck

A separately paid bonus triggers flat supplemental rates: 22% federal, 10.23% California, plus FICA. A bonus combined with your regular paycheck uses the aggregate method instead — adding both to your wages and running the total through standard withholding tables. That can produce more or less withholding depending on your income. Most employers pay bonuses separately, so the flat rates are what most employees see.

Retirement Contributions Reducing Bonus Pay

If your 401(k) is set as a percentage of each paycheck, that same percentage comes out of your bonus. At 10% on a $10,000 bonus, $1,000 goes to your retirement account before the deposit. Pre-tax contributions slightly reduce your taxable bonus, but they also directly reduce your take-home. The 2026 annual 401(k) limit is $23,500 under 50 and $31,000 with catch-up. If you are near that ceiling, payroll may reduce or stop the 401(k) deduction on your bonus check automatically.

Other Voluntary Deductions

Health insurance premiums, FSA and HSA contributions, and union dues may or may not apply to bonus checks depending on your employer’s payroll setup. If they do, a $5,000 bonus could lose another $200 to $500 in benefit deductions. Compare your bonus pay stub to a regular one to spot the difference. If you are not sure what each line on your check means, the guide on how to read a California pay stub in 2026 walks through every deduction code.

Severance pay and lump-sum vacation payouts get the same flat withholding as a cash bonus when paid separately. Overtime is different — when paid on the same check as your regular wages, it goes through standard withholding tables, not the flat supplemental rate. For more on how overtime pay is calculated and taxed, see California overtime laws for 2026. If something looks wrong on any of these check types, contact payroll. Employer errors happen, and fixing them before your W-2 is issued is much easier than correcting it after.

Bonus Tax Calculator Examples for California Employees

All examples use 2026 rates: 22% federal, 10.23% California, 6.2% Social Security, 1.45% Medicare, 1.3% SDI. No retirement or voluntary deductions included. Wages assumed below the Social Security cap.

$2,500 Bonus Example

Gross: $2,500. Federal: $550. California: $255.75. Social Security: $155. Medicare: $36.25. SDI: $32.50. Total withheld: $1,029.50. Net deposit: approximately $1,470.

$5,000 Bonus Example

Gross: $5,000. Federal: $1,100. California: $511.50. Social Security: $310. Medicare: $72.50. SDI: $65. Total withheld: $2,059. Net deposit: approximately $2,941.

$10,000 Bonus Example

Gross: $10,000. Federal: $2,200. California: $1,023. Social Security: $620. Medicare: $145. SDI: $130. Total withheld: $4,118. Net deposit: approximately $5,882. With a 6% 401(k) contribution, subtract another $600 and your deposit drops to about $5,282.

$25,000 Bonus Example

Gross: $25,000. Federal: $5,500. California: $2,557.50. Social Security: $1,550. Medicare: $362.50. SDI: $325. Total withheld: $10,295. Net deposit: approximately $14,705.

$50,000 Bonus Example

Gross: $50,000. Federal: $11,000. California: $5,115. Social Security: $3,100. Medicare: $725. SDI: $650. Total withheld: $20,590. Net deposit: approximately $29,410. If this bonus pushes your year-to-date wages above $184,500, Social Security withholding is reduced or eliminated on the remaining amount, which improves your take-home slightly. To understand how a salary at this income level is taxed throughout the full year, the breakdown of $75K after taxes in California gives useful context.

Types of Bonuses and How California Treats Them

Every bonus type is a supplemental wage under California and federal law. The category does not change the withholding rates. What differs is context — amount, timing, and sometimes repayment rules.

Performance Bonuses

Annual and quarterly performance bonuses, profit-sharing, and productivity incentives are all supplemental wages. A $15,000 year-end bonus at a tech company in San Jose gets the same withholding treatment as a $1,500 quarterly incentive at a retail job in Fresno.

Signing Bonuses

Signing bonuses are taxed as supplemental wages like any other bonus. The key difference: many come with repayment clauses. If you leave within 12 to 24 months, you may owe back the gross amount. You paid taxes on it upfront, but you can potentially claim a deduction when you file if you repay it.

Retention Bonuses

Stay bonuses and retention incentives paid during mergers or transitions follow the same withholding rules as performance bonuses. Same flat rates, same FICA, same SDI. The business reason behind the payment does not change the tax treatment.

Commission Payments

Commissions are supplemental wages. Paid separately, they are withheld at 22% federal and 10.23% California. Paid alongside regular wages, the aggregate method may apply. Holiday bonuses, referral bonuses, and spot bonuses also follow the same supplemental wage rules. If you receive commissions as an independent contractor rather than a W-2 employee, the withholding rules are entirely different — see the full comparison of 1099 vs W-2 tax treatment in California for how that changes your tax picture.

RSUs vest as ordinary income. Most employers withhold at the 22% federal supplemental rate, though some use the aggregate method. California’s 10.23% typically applies, but your employer’s equity plan setup determines the actual method. Non-qualified stock options are taxed as ordinary income at exercise. Incentive stock options (ISOs) are different — ISOs generally have no income tax withholding at exercise, but they can trigger the Alternative Minimum Tax when you file. If you hold ISOs, plan for that tax hit separately. It will not come out of your paycheck automatically.

When Bonus Withholding Is Too High or Too Low

Flat withholding rates rarely match your actual tax liability exactly. The reconciliation happens when you file. For a broader look at how all California payroll taxes interact, the California payroll tax resource hub covers each component in detail.

Situations That May Lead to a Refund

If you are in the 12% federal bracket and 22% was withheld from your bonus, you overpaid by 10 points. You get that back. The same applies on the California side if your actual rate is below 10.23%. Large deductions, the Child Tax Credit, or significant pre-tax retirement contributions can also push your liability below what was withheld. That excess comes back as a refund.

Situations That May Lead to Taxes Owed

California’s top marginal rate is 13.3% above $1,000,000. If your income lands there, the 10.23% withholding on your bonus was not enough. Multiple jobs, large bonuses, or high overall income can also leave you under-withheld for the year. Updating your W-4 or California DE 4 elections, or paying estimated taxes during the year, helps avoid a surprise balance due.

Multi-state situations add complexity. California taxes income based on where the work was physically performed, not where your employer is based. If you worked in California, you likely owe California tax on that income even if you have since moved. But if you worked entirely outside California for a California employer, you may not owe California tax at all. The rules follow the work location. If your situation changed during the year, confirm with your employer’s payroll department or a tax professional before filing.

Common Bonus Tax Myths and Misconceptions

Myth: Bonuses Are Taxed at 40%

That number comes from combining the 22% federal rate and 10.23% California rate, rounding up, and panicking. The real combined withholding, including FICA and SDI, is about 41.18%. But that is the withholding rate, not your actual tax. If your marginal rate is lower than 22%, you will get money back when you file.

Myth: Employers Keep Part of the Bonus

Every dollar withheld goes directly to the IRS and California FTB. Your employer sends it on your behalf and keeps none of it. Your W-2 at year-end shows exactly how much was withheld and where it went.

Myth: Separate Bonus Checks Always Mean Higher Taxes

The flat supplemental rates can feel higher, but your actual tax does not change based on how your employer structured the payment. Withholding method affects the check. It does not affect what you owe when you file. The IRS guidance on supplemental wages confirms this directly.

Myth: You Never Get Bonus Taxes Back

If withholding exceeded your actual liability, the overage comes back as a refund. This is common for employees in the 12% and 22% federal brackets, and for anyone with significant deductions or credits. File accurately and collect what is yours.

How to Estimate Your Actual Bonus Take-Home Pay

Simple Bonus Estimation Formula

Step 1: Start With Gross Bonus

Confirm the gross bonus amount in writing. Verbal figures sometimes differ from what payroll processes.

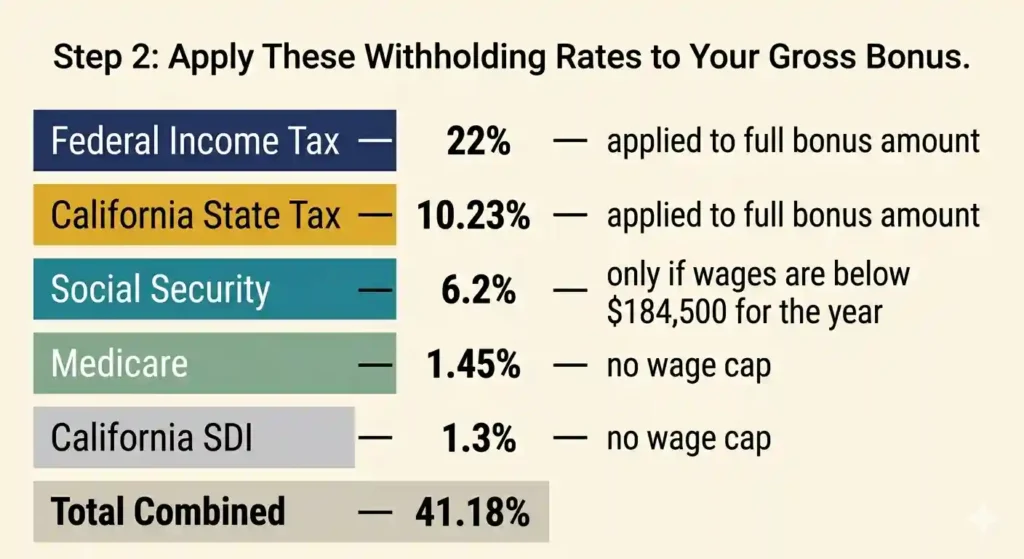

Step 2: Subtract Expected Withholding

Apply each rate to the gross: Federal 22%, California 10.23%, Social Security 6.2% (if under the $184,500 cap), Medicare 1.45%, SDI 1.3%. Add the five amounts together.

Step 3: Adjust for Personal Deductions

Subtract any 401(k), HSA, health insurance, or other benefit deductions your employer applies to bonus checks.

Step 4: Estimate Final Deposit

Gross minus total withholding minus deductions equals your estimated deposit. Expect to land within $50 to $100 of the actual figure on a typical bonus.

Frequently Asked Questions

What is the California bonus tax rate for 2026?

California withholds 10.23% on separately paid bonuses. Federal withholding is 22%. Add Social Security at 6.2%, Medicare at 1.45%, and SDI at 1.3%, and total withholding reaches about 41.18%. That is the withholding rate, not your final tax rate.

Why was nearly 40% taken from my bonus?

Five withholding categories hit simultaneously: 22% federal, 10.23% California, 6.2% Social Security, 1.45% Medicare, and 1.3% SDI. Together that is about 41.18%. None of it is your final tax. All of it is credited against your actual liability when you file.

Will I get bonus taxes back when I file?

It depends on your total income. If your actual tax rate is lower than the withholding rate, you get the difference back. Employees in the 12% bracket who had 22% withheld often see a meaningful refund. High earners may owe more if flat withholding was not enough.

Are bonuses taxed more than salary?

No. Both are ordinary income with the same actual tax rate. The difference is how withholding is calculated at payment time, not how much you ultimately owe.

Can I reduce bonus withholding?

For flat-rate supplemental bonuses, the 22% federal and 10.23% California rates are fixed. Some employers allow the aggregate method, which can produce less withholding. Updating your W-4 or California DE 4 can help over the full year. When you file your federal Form 1040 and California Form 540, any over-withholding is refunded.

Are signing bonuses taxed differently?

No. Same supplemental wage rules apply. The repayment clause is a legal matter, not a tax distinction.

Do commissions use the same withholding rules?

Yes. Commissions are supplemental wages. Paid separately: 22% federal, 10.23% California. Paid with regular wages: aggregate method may apply.

How much will I keep from a $10,000 bonus in California?

Approximately $5,882 before any voluntary deductions. Federal: $2,200. California: $1,023. Social Security: $620. Medicare: $145. SDI: $130. Total withheld: $4,118. A 6% 401(k) contribution drops the deposit to about $5,282.

Final Takeaway — What California Employees Should Expect From a Bonus Check

About 41 cents of every dollar in a California bonus goes to withholding before it reaches your account. That is not a penalty and it is not your final tax rate. It is five separate withholding categories hitting at once.

What comes out of your check and what you actually owe are two different numbers. Know your rates, run the four-step estimate before your bonus arrives, and do not panic when the deposit looks small. That gap is normal.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.