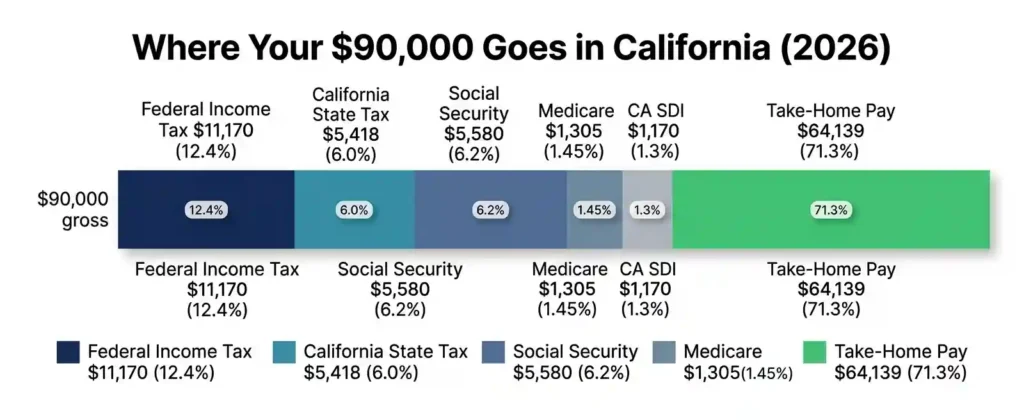

A $90,000 salary in California leaves you with roughly $64,139 per year in take-home pay as a single filer in 2026. That works out to about $5,345 per month before any personal benefit deductions. For a personalized number based on your exact situation, use our California paycheck calculator.

$90k California Salary at a Glance

2026 tax rates, single filer, standard deduction:

| Pay Period | Gross Pay | Estimated Take-Home |

|---|---|---|

| Annual | $90,000 | ~$64,139 |

| Monthly | $7,500 | ~$5,345 |

| Biweekly | $3,462 | ~$2,467 |

| Weekly | $1,731 | ~$1,234 |

| Hourly (after tax) | $43.27 | ~$30.84 |

Your total estimated tax burden is around $25,861, an effective rate of about 28.7% on your whole income, not a flat cut from every dollar.

Takeaway: A $90k salary in California puts roughly $5,345 in your pocket every month after taxes.

Free California Tax Tool

See What $90,000 Looks Like After Taxes in California

$90K salary sounds great — but after federal tax, California state tax, and SDI, your actual take-home is different. See the real number.

🧮 See What $90K Actually Pays You After TaxesUsed by thousands of California workers · FTB-verified 2026 rates

Key Assumptions Behind This Estimate

These numbers use specific baseline conditions. Your actual paycheck will differ based on your situation.

The calculation above assumes you are a single filer using the 2026 federal standard deduction of $16,100. It also assumes you are a California resident using the California state standard deduction of $5,706 for single filers. No pre-tax 401(k) contributions are included in this base estimate. No employer health insurance premiums or other voluntary deductions are factored in.

If you have significant mortgage interest, large charitable contributions, or heavy medical expenses, itemized deductions could reduce your taxable income further below the standard deduction baseline. Dependents also change the picture. Claiming a qualifying child can unlock the Child Tax Credit, which directly reduces your federal tax bill dollar for dollar rather than just lowering taxable income.

The California SDI rate for 2026 is 1.3% applied to all wages with no wage cap, up from 1.2% in 2025.

These calculations also assume full-year California residency. Part-year residents and nonresidents who earn California-sourced income are taxed differently and should consult the California FTB’s nonresident and part-year resident guidelines. If you are relocating to California from a no-income-tax state like Texas, Florida, or Washington, the shift in your net pay can be a real surprise. A $90k earner moving from Texas to California loses roughly $5,400 to $6,500 per year in state and SDI taxes that did not exist before. Factor that into any relocation decision.

Takeaway: These numbers give you a reliable starting point. Run your own numbers if you have 401(k) contributions or health insurance deductions.

Annual, Monthly, Biweekly, Weekly, and Hourly Take-Home Pay

Here is how $90,000 translates across every pay schedule for 2026.

Annual Take-Home Pay

Your gross annual salary is $90,000. After federal income tax, California state income tax, Social Security, Medicare, and SDI, your net annual income is approximately $64,139. Use this number for yearly budgeting and big purchase planning. You can also use our gross pay calculator to verify your gross earnings before taxes are applied.

Monthly Take-Home Pay

Divide your net annual income by 12 and you get approximately $5,345 per month. This is the most useful number for budgeting rent, bills, and groceries. California landlords typically want rent to be no more than one-third of gross income, putting your theoretical rent ceiling around $2,500.

Biweekly Paycheck Estimate

Most salaried employees in California get paid every two weeks. Your biweekly gross paycheck is $3,461.54. After taxes, you take home approximately $2,467 per biweekly check. Over a year, most people get 26 paychecks. Two months a year, you get three paychecks instead of two. That third check is a useful savings opportunity. If your actual paycheck looks different from what you expect, our guide on how to read a California pay stub breaks down every line item.

Some employers pay semimonthly instead of biweekly. That means 24 paychecks per year rather than 26. Your semimonthly gross check would be $3,750, and your after-tax amount would be approximately $2,672. The annual take-home is the same either way, but the timing of your cash flow differs. If you budget by paycheck rather than by month, knowing your pay frequency matters.

Weekly Pay Estimate

On a weekly basis, your gross pay is $1,730.77. After taxes, your weekly take-home lands around $1,234. This breakdown helps freelancers and hourly workers who compare their rate to an equivalent salaried position.

Hourly Equivalent After Taxes

Working full time means roughly 2,080 hours per year. Your $90,000 salary equals $43.27 per hour gross. After all taxes, your true hourly rate drops to about $30.84 per hour, meaning taxes take roughly $12.43 from every hour worked.

Takeaway: Your $90k salary becomes roughly $30.84 per hour after California taxes in 2026.

2026 Tax Breakdown for a $90,000 Salary in California

Most people hear “California taxes” and picture their entire paycheck disappearing. Once you see how each layer works, the numbers make sense.

Bonuses, RSU vesting, overtime, and commission income are taxed as supplemental wages. The IRS withholds federal tax on bonuses at a flat 22% supplemental rate, and California withholds at 10.23%. Your actual tax owed at year-end is the same, but the withholding on a bonus check can feel jarring.

Federal Income Tax

Your federal taxable income starts at $90,000. Subtract the 2026 standard deduction of $16,100 and your taxable income drops to $73,900. The IRS uses progressive brackets, so different portions of your income face different rates. Your adjusted gross income (AGI) can be reduced further by above-the-line deductions like student loan interest or traditional IRA contributions before applying the standard deduction. The IRS publishes all current bracket thresholds and standard deduction amounts in Revenue Procedure 2025-32.

Here is how the 2026 federal brackets stack up on $73,900 of taxable income:

- 10% on the first $11,925 = $1,192.50

- 12% on income from $11,926 to $48,475 = $4,385.88

- 22% on income from $48,476 to $73,900 = $5,591.28

Your total estimated federal income tax is approximately $11,170, an effective federal rate of about 12.4%. You are in the 22% bracket, but only the income above $48,475 gets taxed at that rate.

California State Income Tax

California taxes are separate from federal taxes and use a much lower standard deduction. For 2026, the California single filer standard deduction is just $5,706, making your California taxable income approximately $84,294. The California Franchise Tax Board publishes the official tax rates, deduction amounts, and bracket thresholds used in these calculations.

California has nine tax brackets. At $90,000, the top bracket you hit is 9.3%, which applies to income above $70,607. Your estimated California state income tax is approximately $5,418, an effective state rate of about 6%. The low state deduction pushes your California taxable income nearly $10,000 higher than your federal taxable income, and that gap costs real money at 9.3%. See the full California income tax brackets for 2026 for a complete rate breakdown by filing status.

Social Security Tax

Social Security is a federal payroll tax set at 6.2% of your wages. In 2026, this applies to the first $184,500 of earned income, as confirmed by the Social Security Administration. At $90,000, you fall well below the wage base cap, paying approximately $5,580 per year toward your eventual retirement benefits.

Medicare Tax

Medicare tax is 1.45% of all wages with no wage cap. At $90,000, your annual Medicare contribution is approximately $1,305. The additional 0.9% surcharge does not apply until income exceeds $200,000 for single filers.

California State Disability Insurance (SDI)

California SDI is unique to the state and often surprises new residents. The 2026 SDI rate is 1.3% on all wages with no cap, up from 1.2% in 2025. At $90,000 gross income, your SDI deduction is approximately $1,170 per year or about $97.50 per month. The rate and program rules are administered by the California Employment Development Department (EDD).

SDI covers short-term disability and funds California’s Paid Family Leave program, which provides up to 8 weeks of partial pay for a new child or sick family member. For a deeper look at how all California payroll deductions work together, browse our paycheck basics resources.

Takeaway: Your five main tax deductions total about $25,861, leaving you with $64,139 net annual pay.

Is $90,000 a Good Salary in California?

The answer depends on where in California you live and whether you are single or sharing expenses.

The median household income in California for 2026 is estimated at approximately $91,905, based on recent U.S. Census Bureau American Community Survey trend data. At $90,000 as a single earner, you earn more than about 73% of individual workers statewide, putting you solidly in the middle class. But California’s cost of living index sits at 149.9, nearly 50% more expensive than the national average. That gap shrinks what $90k can actually do.

What Lifestyle Can $90k Support?

Single Professional

In Sacramento, Fresno, or the Inland Empire, $90k provides genuine financial breathing room. You can rent a one-bedroom, drive a reliable car, save toward retirement, and still have money for dining out and weekend activities.

In Los Angeles, a decent one-bedroom near work runs $2,200 to $2,500 per month, nearly half your $5,345 take-home. After rent, a car, groceries, and utilities, discretionary spending is tight but possible.

In San Francisco, a one-bedroom averages over $3,200 per month, consuming 60% of your take-home and leaving very little room for savings.

Couple Household

If one person earns $90k while a partner earns even modestly, the picture changes dramatically. Shared rent cuts housing costs roughly in half, opening access to two-bedroom apartments and leaving more for savings and discretionary spending. Two people splitting a $3,000 rent each pay $1,500, which makes $90k genuinely comfortable in most California cities outside the Bay Area.

Challenges of Living on $90k

High housing costs are the number one challenge. California’s average rent across all apartment types reached approximately $2,700 per month in 2026, nearly double the national average of $1,995. For a single earner at $90k, this is a significant budget constraint.

Transportation is another drain. Gas in California averages around $5.20 per gallon in 2026, and car insurance runs about $2,100 to $2,500 annually. If you live somewhere without solid public transit, budget $400 to $600 per month for all vehicle-related costs.

Grocery prices run about 14% above the national average in California. A single person typically spends $350 to $400 per month on food. Dining out regularly adds another $200 to $400 per month in most cities.

For context: a $90k earner in Texas, Florida, or Washington pays zero state income tax and no SDI. Their take-home on the same gross salary is approximately $69,500 to $70,000 per year compared to $64,139 in California, a gap of $5,000 to $6,000 per year driven entirely by state taxes. California’s career opportunities and infrastructure are real trade-offs many workers consciously accept.

Takeaway: $90k is a good California salary, but location determines whether it feels comfortable or stretched.

Cost of Living Comparison Across California Cities

Where you live in California changes your entire financial story. Location is the single biggest variable in your budget at $90k.

Los Angeles

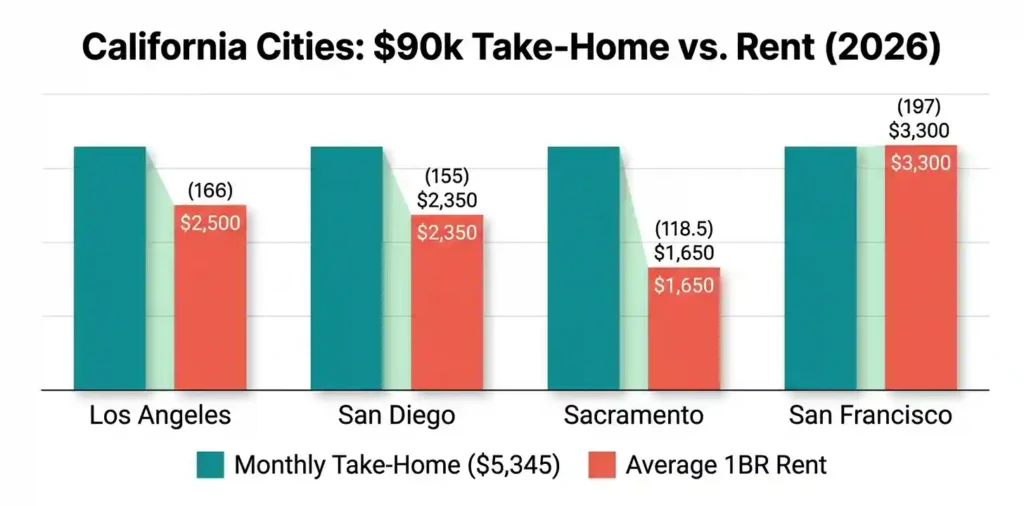

Los Angeles has a cost of living index of approximately 166, about 66% more expensive than the national average. A one-bedroom apartment averages $2,400 to $2,600 per month, and a two-bedroom pushes past $3,000 in desirable neighborhoods. After rent, a car, groceries, utilities, and phone, your $5,345 take-home leaves a tight margin. Saving aggressively requires living in less central neighborhoods. Run your exact numbers with our Los Angeles paycheck calculator.

San Diego

San Diego’s cost of living index sits around 155, with one-bedroom rents averaging $2,200 to $2,500 per month. The city has a strong job market in biotech, defense, and healthcare. Your budget math at $90k is nearly identical to LA, but many people find the shorter commutes and calmer pace worth the trade-off. Get a city-specific breakdown with our San Diego paycheck calculator.

Sacramento

Sacramento is where $90k genuinely starts to feel good. The cost of living index here is about 118.5, well below the state average. Average one-bedroom rents run approximately $1,650 per month, with solid two-bedroom apartments available for $2,000 to $2,200.

On a $5,345 monthly take-home, Sacramento rent leaves you roughly $3,700 for everything else, creating real room to save and build financial security. Use our Sacramento paycheck calculator to model your exact take-home for this city.

San Francisco Bay Area

San Francisco is the toughest test for a $90k salary in California. The cost of living index is approximately 197, nearly double the national average. A one-bedroom averages $3,200 to $3,400 per month, over 60% of your monthly take-home.

Most $90k earners in San Francisco rely on roommates, live in the East Bay, or commute from Oakland or Daly City. Even with cost-sharing, Bay Area living on $90k means limited savings capacity. Our San Francisco paycheck calculator can show you exactly what your net pay looks like at this income level in the Bay Area.

Takeaway: Sacramento offers the best quality of life per dollar on a $90k California salary in 2026.

Real-World Budget Example for a $90k Salary

Here is what a realistic monthly budget looks like on $90k after taxes in California.

Example Budget for a Single Renter

This example uses Sacramento as a baseline, since it offers the most realistic balance of California living and financial breathing room.

Monthly Take-Home: $5,345

| Category | Monthly Cost |

|---|---|

| Rent (1BR) | $1,650 |

| Car payment + insurance | $550 |

| Groceries | $380 |

| Utilities + internet | $180 |

| Gas | $150 |

| Health insurance (if not employer-covered) | $300 |

| Phone | $80 |

| Dining out + entertainment | $300 |

| Personal care + misc | $150 |

| Total Expenses | $3,740 |

| Remaining for savings/investing | $1,605 |

In Sacramento, a disciplined single renter on $90k can save over $1,600 per month. That is real wealth-building potential. Run this same budget in San Francisco and the rent line alone jumps to $3,200, wiping out most of that savings room.

Example Budget for a Couple

This example assumes one partner earns $90k. This is a single-income couple sharing costs.

Monthly Take-Home: $5,345 (one earner)

| Category | Monthly Cost |

|---|---|

| Rent (2BR in Sacramento) | $2,000 |

| Two cars (shared costs) | $700 |

| Groceries | $550 |

| Utilities + internet | $200 |

| Health insurance | $400 |

| Gas | $200 |

| Dining out + entertainment | $400 |

| Personal care + misc | $200 |

| Total Expenses | $4,650 |

| Remaining | $695 |

A single-income couple at $90k can get by in mid-cost California cities, but savings are limited without a second income. Adding even a part-time second earner creates dramatically more financial flexibility.

Savings and Emergency Fund Allocation

Financial advisors commonly recommend saving at least 20% of take-home pay. On a $5,345 monthly take-home, that is $1,069 per month. This includes retirement savings, emergency fund contributions, and any other investment vehicles.

A solid starter plan targets three to six months of expenses in an emergency fund before investing heavily. At $3,740 in monthly expenses, you need $11,220 to $22,440 in your emergency fund. Saving $500 per month gets you there in less than two years.

Once the emergency fund is in place, that same $500 to $1,000 per month becomes a powerful debt repayment or net worth building tool. At $90k, a disciplined saver in a mid-cost California city can realistically add $10,000 to $15,000 per year to their net worth through retirement contributions, savings, and debt reduction.

Takeaway: Budget for at least $1,000 in savings per month on $90k. Sacramento makes this achievable. San Francisco makes it nearly impossible without major trade-offs.

How Filing Status Changes Your Take-Home Pay

Filing status is one of the most powerful levers in your tax calculation. Getting it right can mean thousands of dollars more per year.

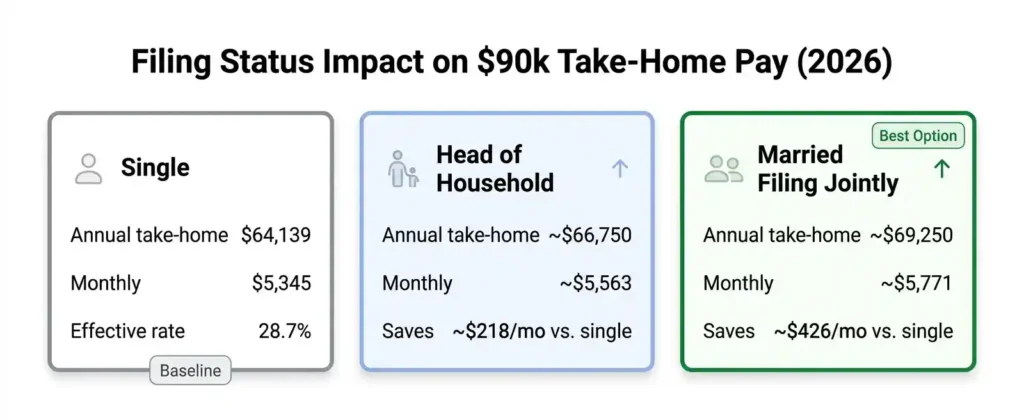

Single Filer

This is the baseline used in all the calculations above. A single filer with no dependents uses the 2026 standard deduction of $16,100 federally and $5,706 for California state taxes. Estimated annual take-home: approximately $64,139. Effective total tax rate: about 28.7%.

Married Filing Jointly

Married filers using the joint standard deduction of $32,200 federally and $11,412 for California benefit significantly. The wider federal brackets also mean less income falls into the higher 22% bracket. A household where only one spouse earns $90k and files jointly can take home approximately $68,500 to $70,000 per year, depending on deductions and credits.

The “marriage bonus” is real at this income level. Joint filers keep roughly $4,000 to $6,000 more per year than single filers earning the same salary.

Head of Household

Head of household status applies to unmarried filers who pay more than half the cost of keeping up a home for a qualifying dependent. For 2026, the federal HOH standard deduction is $24,150, giving wider brackets than single filers. A $90k earner filing HOH takes home approximately $66,000 to $67,500 per year, about $2,000 more than filing single.

Takeaway: Married filing jointly saves the most. Head of household beats single filing by about $2,000 per year at $90k.

What If You Contribute to a 401(k)?

A 401(k) contribution does not just save for retirement. It reduces your taxable income right now, so the government takes less from your paycheck immediately.

No 401(k) Contributions

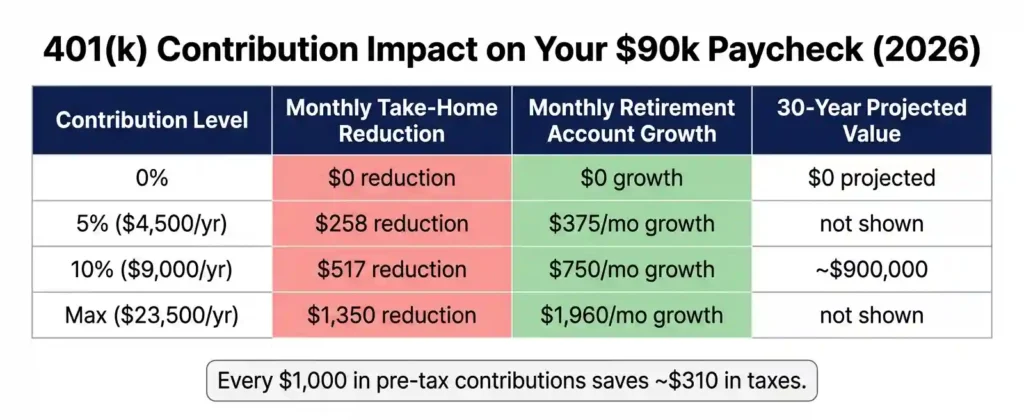

Without any 401(k) contributions, your entire $90,000 is subject to federal and state income taxes. Your estimated take-home pay is $64,139 per year.

5% Contribution Scenario

A 5% 401(k) contribution means you defer $4,500 per year into your retirement account. This reduces your federal and California taxable income by $4,500 each. The immediate tax savings in your 22% federal bracket and 9.3% California bracket combined add up to roughly $1,400 per year in tax savings.

Your monthly paycheck drops by about $258 ($4,500 divided by 12 minus the $117 in tax savings). But your retirement account grows by $375 per month before any employer match. If your employer matches 3%, you capture another $112 per month in free money.

10% Contribution Scenario

A 10% contribution defers $9,000 per year. Your taxable income falls to $81,000, lowering your tax bill by approximately $2,800 per year. Your monthly take-home drops by around $517, but your retirement account receives $750 per month before any match.

Over 30 years at a 7% average return, $750 per month compounds to approximately $900,000 in retirement savings.

If you can stretch to the 2026 IRS maximum of $23,500, the tax savings become even more substantial. At that contribution level, your taxable income drops to $66,500, and your combined tax savings reach approximately $7,300 per year. Your monthly take-home shrinks by about $1,350 compared to zero contributions, but your retirement account grows by nearly $1,960 per month before any employer match. Most people cannot max their 401(k) on $90k in a high-cost city, but even getting close is worth the effort.

One more thing worth flagging: if you have a side job or freelance income in addition to your $90k salary, that income is subject to self-employment tax at 15.3% on top of regular income taxes. Side income does not get a W-2 or employer withholding, so you may need to make quarterly estimated tax payments to avoid underpayment penalties at tax time. Our guide on 1099 vs W-2 income in California explains how the two income types are taxed differently.

Takeaway: A 10% 401(k) contribution costs about $517 per month in take-home pay but builds roughly $900,000 in retirement wealth over 30 years.

How Health Insurance and Other Payroll Deductions Affect Take-Home Pay

These tax numbers assume zero payroll deductions beyond mandatory ones. Most employees have additional deductions that further reduce their paycheck.

Employer Health Insurance

Employer-sponsored health insurance premiums paid by employees are typically deducted pre-tax under a Section 125 cafeteria plan. If your employer-sponsored plan costs you $300 per month in employee premiums, that $3,600 annual deduction reduces your federal and state taxable income. At your combined marginal rate of roughly 31%, this saves you about $1,116 per year in taxes.

The net real cost of that $300 monthly premium is closer to $207 after the tax benefit. This is why employer health insurance, even when not entirely free, is one of the most cost-effective benefits available. Dental insurance and vision insurance premiums work the same way when offered through a pre-tax cafeteria plan. If you pay $30 per month for dental and $10 for vision, those amounts also reduce your taxable income and cost you less than the face value suggests.

HSA Contributions

A Health Savings Account works with a high-deductible health plan. Contributions are pre-tax, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. The 2026 HSA contribution limit is $4,400 for individuals and $8,750 for families, as announced by the IRS in Revenue Procedure 2025-19.

Contributing the full $4,400 reduces your taxable income by $4,400, saving approximately $1,364 per year in combined taxes at your income level. Money not used for healthcare rolls over indefinitely and can be invested like a second retirement account after age 65.

Takeaway: Health insurance premiums and HSA contributions are among the most tax-efficient ways to increase your real take-home value on a $90k salary.

$90k vs Other California Salaries

Here is how $90k stacks up against nearby salary levels in California.

80k vs 90k After Taxes

Both $80k and $90k land in the same federal and California 9.3% brackets, so the marginal rate on that extra $10,000 is significant.

At $80k, a single California filer takes home approximately $57,800 per year or about $4,817 per month. At $90k, take-home is approximately $64,139, a difference of roughly $6,339 per year or $528 per month — meaningful for rent upgrades, faster debt payoff, or savings. For comparison at a lower income level, see our post on $75k after taxes in California.

90k vs 100k After Taxes

At $100k, a single California filer takes home approximately $70,200 per year, or about $5,850 per month. The step from $90k to $100k adds roughly $506 per month to your take-home pay. We cover that income level in detail in our post on $100k after taxes in California.

Crossing six figures matters psychologically in salary negotiations, but financially the move from $99k to $100k is the same ~$50 per month as any $1,000 raise at this income level. What it does signal is a stronger benchmarking position with employers.

90k vs 120k After Taxes

At $120,000, a single California filer takes home approximately $82,500 per year, or around $6,875 per month. Compared to $90k take-home of $5,345 per month, the $30k salary increase produces about $1,530 more per month in net pay. See the full breakdown in our guide on $120k after taxes in California.

However, the $120k earner begins paying California’s highest non-millionaire bracket rates more heavily. The effective total tax rate at $120k climbs to roughly 31.3%, compared to 28.7% at $90k. Each additional dollar earned between $90k and $120k is taxed more aggressively.

Takeaway: Every $10k salary increase at this income range adds roughly $500 per month to your California take-home pay.

Common Myths About a $90k Salary in California

After years of explaining California taxes, the same misconceptions come up every time. Here is the truth on each one.

Myth: A Higher Tax Bracket Means Losing Money

The U.S. tax system is progressive. Moving into a higher bracket means only the income above that bracket’s threshold gets taxed at the higher rate, not your entire income.

If your income goes from $89,000 to $91,000, only the last $2,000 is taxed at the higher rate. A raise is always a net gain.

Myth: California Takes Half Your Paycheck

California does have high taxes compared to many states, but the math does not support the “half your paycheck” claim at $90k. Your combined effective tax rate on a $90k salary is approximately 28.7%. That leaves you with 71.3% of your gross income. California’s top rate of 13.3% applies only to income over $1 million. At $90k, your California effective rate is closer to 6%. For a full breakdown of every payroll tax California employers and employees pay, see our California payroll taxes overview.

Myth: Gross Salary Determines Affordability

Many people compare salaries without accounting for taxes and local costs. A $90k salary in Sacramento has different real buying power than a $90k salary in San Francisco. Always evaluate salary offers alongside local tax burden and cost of living, not just the headline number.

Myth: Every Worker Takes Home the Same Amount

Even two people earning exactly $90k in California can have very different take-home pay. Filing status, 401(k) contributions, health insurance premiums, FSA elections, and other voluntary deductions all change the bottom line. One person contributing 10% to their 401(k) takes home about $517 less per month than a coworker earning the same salary with no contributions. If your paycheck consistently looks lower than expected, our guide on why your California paycheck is so low identifies the six most common causes.

Takeaway: Never assume your paycheck will match a coworker’s. Variables like filing status and deductions create real differences in take-home pay.

How to Increase Your Take-Home Pay Legally

You do not need a raise to put more money in your pocket. These strategies reduce your tax burden starting with your next paycheck.

Increase Pre-Tax Contributions

The fastest way to reduce your tax bill is to increase contributions to pre-tax accounts. Every dollar you put into a traditional 401(k), 403(b), or similar plan reduces your taxable income dollar for dollar. At a combined federal and state marginal rate of roughly 31%, every $1,000 in pre-tax contributions saves about $310 in current taxes. The IRS confirmed the 2026 employee 401(k) contribution limit at $23,500 per year.

Maximizing your 401(k) also helps if your employer offers a match. A common match structure is 100% on the first 3% of your salary, which adds $2,700 per year in free money at a $90k salary. Never leave an employer match on the table.

Optimize Withholding

Your W-4 controls how much federal tax your employer withholds each paycheck. Many employees over-withhold, giving the government an interest-free loan until April. The IRS Tax Withholding Estimator can tell you exactly how to adjust your W-4 to put more in each paycheck instead of a large refund.

California’s DE-4 controls state withholding. Review it after any major life change: raise, marriage, divorce, or new dependent. Our step-by-step guide on how to fill out California Form DE-4 walks you through every section.

Use HSA and FSA Accounts

A Health Savings Account or Flexible Spending Account lets you pay for medical, dental, and vision expenses with pre-tax dollars. If you spend $2,000 per year on healthcare, running those payments through an HSA or FSA saves approximately $620 per year in taxes at your income level. That is money that would otherwise go to the IRS and the California FTB.

FSAs can also cover dependent care expenses. If you pay for childcare, a Dependent Care FSA lets you shelter up to $5,000 per year in pre-tax income. For HSA users, the 2026 individual contribution limit is $4,400, giving you a powerful additional tax-reduction tool on top of your 401(k).

Takeaway: Combining a maxed 401(k), an HSA, and a correct W-4 can add $200 to $500 per month to your effective take-home pay without earning one extra dollar.

Frequently Asked Questions

How much is 90k after taxes in California per month?

A $90,000 salary in California produces approximately $5,345 per month after taxes for a single filer using the 2026 standard deduction. This includes federal income tax, California state income tax, Social Security, Medicare, and SDI. Married filers and those with pre-tax deductions will see higher monthly take-home amounts.

How much is each paycheck on a $90k salary?

If you are paid biweekly (every two weeks), your take-home paycheck is approximately $2,467. That assumes single filing status with no 401(k) or health insurance deductions. Most employees will see a lower number because of workplace benefit deductions.

Is $90,000 considered middle class in California?

Yes. According to the Pew Research Center’s middle-class income calculator, California’s middle-class income range spans from $61,269 to $183,810 for a household. California’s projected median household income is approximately $91,905 in 2026. A single earner at $90k sits just below the state median and falls squarely within middle-class territory by income level.

Can I comfortably live in California on $90k?

Comfortably is the key word. In Sacramento, Fresno, or the Inland Empire, yes. In Los Angeles, you can live well with disciplined budgeting. In San Francisco, $90k is genuinely challenging unless you have a roommate or partner sharing costs. Where you live matters more than the salary number itself.

How much tax do I pay on a $90k salary?

A single California filer earning $90,000 in 2026 pays approximately:

- Federal income tax: ~$11,170

- California state income tax: ~$5,418

- Social Security: ~$5,580

- Medicare: ~$1,305

- California SDI: ~$1,170

- Total taxes: ~$25,861 (effective rate: ~28.7%)

Does a 401(k) increase take-home pay?

Not directly. A traditional 401(k) reduces your taxable income, which lowers your tax bill. That tax reduction partially offsets the money deferred into your account. A 10% 401(k) contribution at $90k costs you about $517 per month in net take-home pay but saves roughly $2,800 per year in taxes while building significant long-term wealth.

Is $90k enough to buy a home in California?

Qualifying for a California mortgage on $90k is possible but difficult in expensive markets. Most lenders use a 43% debt-to-income ratio cap. On $90k gross ($7,500 per month), that limits your total monthly debt payments to $3,225. After taxes, your actual take-home is only $5,345, meaning a mortgage plus other debts would consume most of your income. Sacramento and Inland Empire markets are more realistic targets than LA or the Bay Area, with Sacramento median home prices running approximately $530,000 to $560,000 in 2026.

For families, $90k as a single household income gets tight quickly. Childcare alone costs $1,500 to $2,500 per month in most California cities. A family of three or four needs a second income or significantly lower housing costs to maintain a comfortable lifestyle on a $90k base salary.

Why do calculators show different results?

Different calculators use different assumptions. Variations come from filing status, whether they include SDI, which standard deduction amount they use (federal vs. state), whether pre-tax deductions are included, and how they round bracket calculations. The numbers in this guide use 2026 confirmed rates from the IRS and California FTB with single filing status and no additional deductions. Browse our paycheck scenarios to see how results shift under different contribution and deduction combinations.

Final Verdict: What a $90k California Salary Really Means in 2026

A $90,000 salary in California produces approximately $64,139 in annual take-home pay, or roughly $5,345 per month, for a single filer using the 2026 standard deduction. Your effective tax rate is about 28.7%. California’s taxes are real, but they do not come close to half your income.

Where you live and whether you share costs determines whether $90k feels comfortable or stretched. Sacramento and Fresno offer genuine breathing room. Los Angeles is workable with discipline. San Francisco requires serious trade-offs.

The person on $90k who maxes their 401(k), uses an HSA, and lives in Sacramento is in a completely different financial position than someone at the same salary renting alone in San Francisco with no retirement contributions.

If you are evaluating a job offer, anchor on $5,345 per month, not the $90k headline. If you are weighing a raise from $80k to $90k, that is $528 more per month in real cash. If you are relocating from a no-tax state, factor in $5,000 to $6,000 per year in new California taxes. Our annual salary calculator can model any income scenario side by side so you can compare offers before you decide.

The $90k salary in California is a solid foundation. What you build on top of it is entirely up to you.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.