The 2026 HSA contribution limit is $4,400 for self-only coverage and $8,750 for family coverage, per IRS Revenue Procedure 2025-19. Those limits cover every dollar going in, your contributions and your employer’s combined against one shared ceiling. A family at the 24% tax bracket who maxes out saves $2,100 in federal taxes alone. The catch: going even one dollar over triggers a 6% excise tax that repeats every year until corrected. Your actual limit may be lower if you were not enrolled in a qualifying plan for the full calendar year. For a broader look at how pre-tax deductions reduce your paycheck, the California payroll taxes resource hub covers every major withholding category.

Quick Answer: 2026 HSA Contribution Limits at a Glance

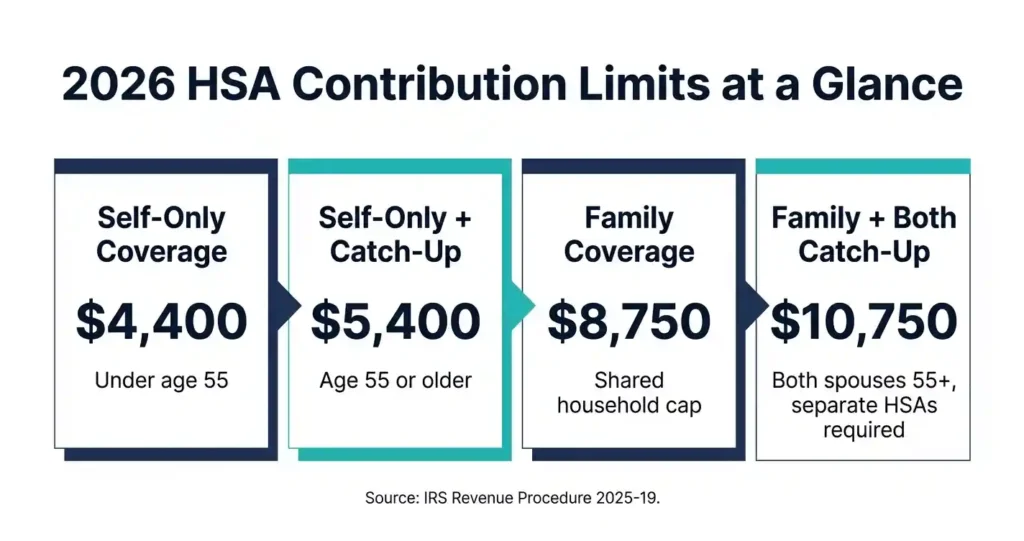

- Self-only coverage: $4,400 (up from $4,300 in 2025)

- Family coverage: $8,750 (up from $8,550 in 2025)

- Catch-up contribution (age 55+): $1,000 extra per person

- Key change from 2025: Self-only up $100. Family up $200.

These limits cover every dollar into your HSA — your contributions plus your employer’s.

2026 HSA Contribution Limits Table

| Coverage Type | 2026 Limit | Age 55+ Total |

|---|---|---|

| Self-Only | $4,400 | $5,400 (one eligible spouse) |

| Family | $8,750 | $9,750 (one 55+ spouse) / $10,750 (both 55+, separate HSAs required) |

| Catch-Up (per person) | $1,000 | N/A |

Takeaway: The 2026 HSA max is $4,400 for self-only and $8,750 for family coverage.

2025 vs 2026 HSA Limits Comparison

| 2025 | 2026 | Increase | |

|---|---|---|---|

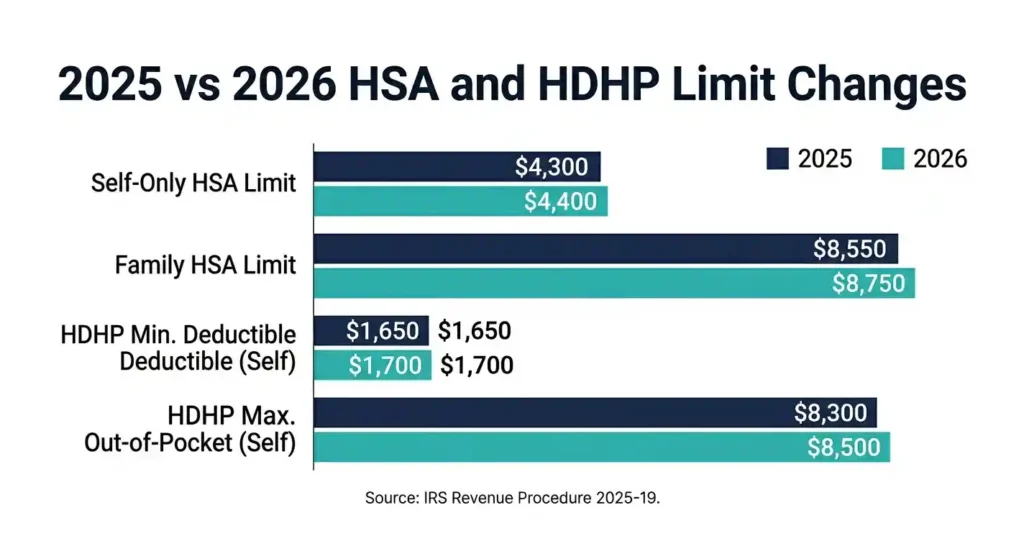

| Self-Only | $4,300 | $4,400 | +$100 (2.3%) |

| Family | $8,550 | $8,750 | +$200 (2.4%) |

| Catch-Up | $1,000 | $1,000 | No change |

| HDHP Min. Deductible (Self) | $1,650 | $1,700 | +$50 |

| HDHP Min. Deductible (Family) | $3,300 | $3,400 | +$100 |

| HDHP Max. Out-of-Pocket (Self) | $8,300 | $8,500 | +$200 |

| HDHP Max. Out-of-Pocket (Family) | $16,600 | $17,000 | +$400 |

The IRS released these cost-of-living adjustments (COLA) on May 1, 2025, through Revenue Procedure 2025-19. They apply to both HSA limits and HDHP thresholds. The contribution aggregation rule means every dollar from any source counts toward one combined annual ceiling.

Takeaway: Every 2026 HSA limit went up compared to 2025.

Who Can Contribute to an HSA in 2026?

Basic Eligibility Requirements

To contribute in 2026, you must: be enrolled in a qualifying HDHP, not be claimed as a tax dependent, not be enrolled in Medicare, and have no disqualifying non-HDHP coverage.

Under Internal Revenue Code Section 223, eligibility is determined month by month. IRS Publication 969 is the clearest plain-language guide to these rules. If your spouse carries a traditional low-deductible plan and you are covered under it even secondarily, you lose eligibility. Understanding how these deductions show up on your paycheck is easier once you know how to read a California pay stub and identify every pre-tax line item.

Takeaway: You need an HSA-eligible HDHP and no disqualifying coverage to contribute in 2026.

What Counts as a Qualified HDHP in 2026?

For 2026, your plan must have a minimum deductible of $1,700 (self-only) or $3,400 (family), and an out-of-pocket maximum no higher than $8,500 (self-only) or $17,000 (family). Your plan generally cannot pay benefits before the deductible is met — with one key exception: the OBBBA permanently allows telehealth and remote care coverage before the deductible without affecting HSA eligibility, effective for plan years beginning January 1, 2025.

The biggest 2026 rule change: under the One Big Beautiful Bill Act (signed July 4, 2025) and IRS Notice 2026-05, all Bronze and Catastrophic ACA Marketplace plans are now treated as HSA-compatible, even if they do not meet the traditional HDHP deductible thresholds. If you are on a Bronze or Catastrophic plan in 2026, you can open and fund an HSA.

Takeaway: Your HDHP must meet 2026 IRS thresholds, but Bronze and Catastrophic ACA plans are now also HSA-eligible as of January 1, 2026.

Situations That Make You Ineligible

Enrolling in Medicare Part A or Part B stops eligibility from that month forward. Watch out for one detail: if you delay Medicare past age 65, Social Security can retroactively enroll you in Part A for up to six months, making any HSA contributions during those months excess contributions. Gaining non-HDHP coverage, being claimed as a tax dependent, or holding a general-purpose Health Care FSA (not a Limited Purpose FSA) also disqualify you.

Starting January 1, 2026, having a Direct Primary Care (DPC) arrangement no longer disqualifies you. Before 2026, DPC memberships were treated as disqualifying coverage. That rule is gone under the One Big Beautiful Bill Act.

Takeaway: Medicare enrollment, non-HDHP coverage, or being a tax dependent each disqualify you. DPC arrangements no longer disqualify you as of 2026.

2026 HSA Contribution Limits Explained

Self-Only Coverage Limit

Self-only HDHP coverage means a 2026 limit of $4,400 — about $366.67 per month. You can contribute the full amount in January, spread it across the year, or wait until April 15, 2027. The limit applies regardless of your marital status or dependents. To see how an HSA contribution changes your net pay, run the numbers through the California paycheck calculator with your pre-tax deductions included.

Takeaway: Self-only HDHP enrollees can contribute up to $4,400 to their HSA in 2026.

Family Coverage Limit

Family HDHP coverage gives a 2026 combined limit of $8,750 shared across all HSAs in the household. You and your spouse do not each get $8,750. If both spouses each have their own self-only HDHP, each gets the $4,400 self-only limit. The family limit applies only when at least one of you is on a family HDHP.

Takeaway: Family HDHP enrollees share one $8,750 combined HSA limit in 2026.

Catch-Up Contributions for Age 55+

If you are 55 or older, you can add $1,000 on top of your regular limit. This amount is set by statute and has not changed since 2009. Under the default proration method, the catch-up is prorated like the regular limit for partial-year eligibility. If you are eligible all 12 months of 2026, the full $1,000 applies regardless of when your birthday falls. The last-month rule also unlocks the full catch-up if you are eligible on December 1.

If both spouses are 55 or older, each gets the $1,000 catch-up — but each must have a separate HSA account. A couple both aged 55+ on a family HDHP can contribute up to $10,750 combined if both have their own accounts.

Takeaway: Each spouse aged 55+ gets their own $1,000 catch-up, but each needs a separate HSA account.

Employer Contributions and Your Limit

Employer HSA deposits count toward your annual limit — the same $4,400 or $8,750 ceiling. If your employer puts in $800 on a family plan, your personal maximum drops to $7,950. This is the most common reason people accidentally go over the limit. Employer deposits appear as a pre-tax benefit on your pay stub, which is why learning to read every line of your California pay stub is worth your time before setting payroll deductions.

Takeaway: Employer HSA contributions count toward your IRS annual limit, so always track the combined total.

How to Calculate Your Maximum HSA Contribution

Full-Year Eligibility Calculation

If you were HSA-eligible all 12 months of 2026, your limit is the full IRS amount: $4,400 (self-only), $8,750 (family), plus $1,000 if you are 55 or older. A 58-year-old on a self-only plan can contribute up to $5,400. A couple both 55+ on a family plan with separate HSAs can contribute up to $10,750 combined.

Takeaway: Full-year eligibility means you can contribute the full IRS limit for your coverage type.

Partial-Year Eligibility Calculation

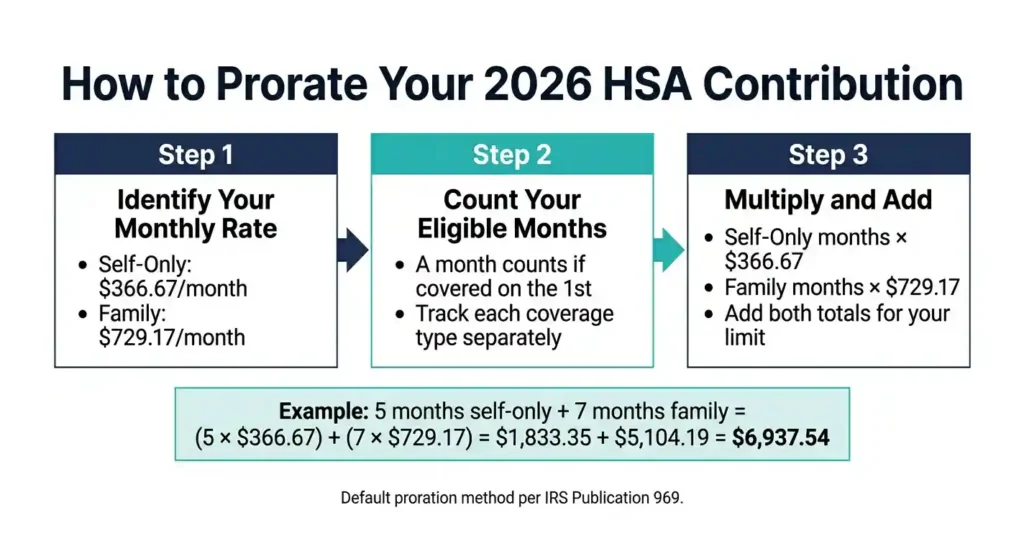

Divide your annual limit by 12 to get your monthly rate: $366.67 (self-only) or $729.17 (family). Multiply by your eligible months. A month counts if you were covered on the first day, this is the eligibility on first of month rule. Six eligible months on self-only equals a $2,200 limit.

If you switch from family to self-only mid-year, months before the switch use the family rate and months after use the self-only rate. Your limit shrinks at the switch point, and contributions already made may suddenly be over the new ceiling.

Takeaway: Partial-year eligibility reduces your limit to a prorated monthly amount based on eligible months.

Self-Only to Family Coverage Changes

Switching Mid-Year

Each month gets the rate for the coverage type you had that month. Switching to family coverage on June 1 means five months at $366.67 and seven months at $729.17 — a total 2026 limit of $6,937.52. The family rate does not apply retroactively to months before the switch.

Takeaway: Mid-year coverage changes require a month-by-month calculation to find your exact limit.

Real-World HSA Contribution Examples

Single Employee Under Age 55

Sarah, 34, is on a self-only HDHP. Her employer deposits $500. Her 2026 limit is $4,400, so she can add $3,900 more. She sets a $325 monthly payroll deduction and hits the full limit by December. At a 22% federal tax bracket, she saves $968 in federal income taxes on those contributions. Understanding where your paycheck lands inside the 2026 California tax brackets helps you calculate the exact tax value of every HSA dollar you put in.

Takeaway: Subtract your employer’s contribution from $4,400 to find exactly how much you can still add.

Married Couple with Family HDHP

Tom and Lisa, both 45, are on Tom’s family HDHP. His employer contributes $1,200. Their combined limit is $8,750, leaving $7,550 to split. Tom contributes $3,775 through payroll; Lisa, self-employed, adds $3,775 directly. They hit the limit exactly.

Takeaway: Married couples on a family plan share one limit and must track all contributions together.

Married Couple Both Age 55+

David, 58, and Maria, 57, are on David’s family HDHP. Base limit: $8,750. Each adds a $1,000 catch-up, but Maria must use her own separate HSA for her $1,000. Combined maximum: $10,750.

Takeaway: Both spouses age 55+ can claim the catch-up, but each must use a separate HSA account.

Self-Employed Individual

Marcus, 42, bought his own qualifying family HDHP. With no employer contribution, his full 2026 limit is $8,750. He contributes $729.17 per month directly and deducts the full amount on his federal return without itemizing. If you are weighing self-employment against W-2 work, the full 1099 vs W-2 comparison breaks down how your tax treatment — including HSA deductibility — changes under each status.

Takeaway: Self-employed people can contribute the full limit and deduct it directly on their tax return.

The Last-Month Rule and Testing Period

What the Last-Month Rule Means

If you are enrolled in an HSA-eligible HDHP on December 1, 2026, the IRS lets you contribute the full annual limit for 2026, regardless of when you enrolled. Even enrolling on November 15 still allows a full $4,400 (self-only) or $8,750 (family) contribution.

Takeaway: Being HSA-eligible on December 1 lets you contribute the full 2026 limit regardless of when you enrolled.

Understanding the Testing Period

Using the last-month rule triggers a 13-month testing period. You must stay enrolled in an HSA-eligible HDHP from December 1, 2026, through December 31, 2027. Drop coverage during that window and the IRS recaptures the excess as taxable income plus a 10% penalty. The only exceptions are disability or death.

Takeaway: The last-month rule requires 13 months of continuous HDHP coverage, or you face taxes and a 10% penalty.

HSA Contribution Deadlines for 2026

Final Contribution Deadline

You can make 2026 HSA contributions up to April 15, 2027 — the federal tax filing deadline. Filing an extension does not move this date. Tell your HSA provider the contribution is for tax year 2026 so it is coded correctly.

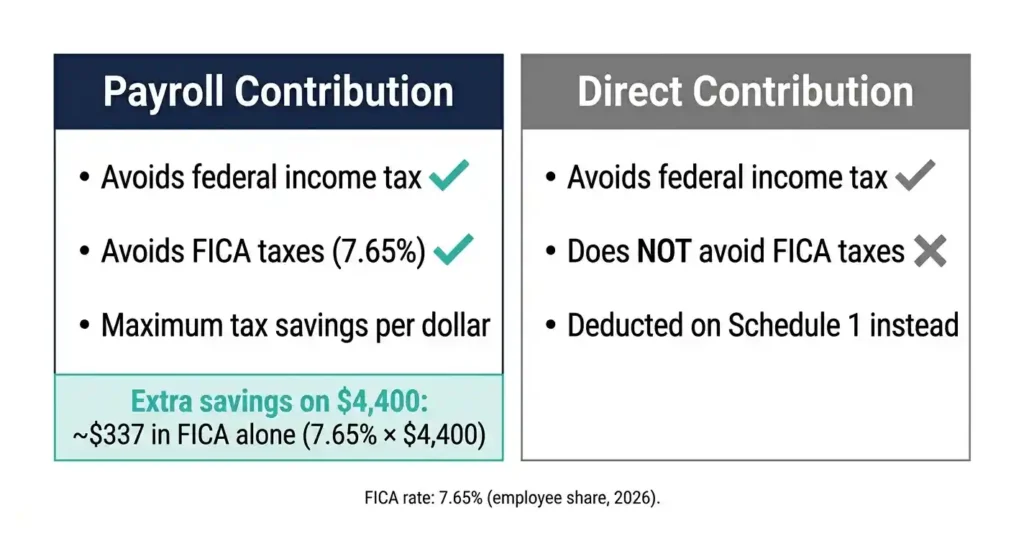

All HSA activity is reported on IRS Form 8889, attached to your Form 1040. Direct contributions outside of payroll appear as a Schedule 1 above-the-line deduction, reducing your adjusted gross income without itemizing. If you are also adjusting your state withholding for 2026, now is a good time to revisit how to fill out California Form DE-4 so your paycheck withholding stays accurate.

Takeaway: You have until April 15, 2027, to make 2026 HSA contributions.

Payroll vs Direct Contributions

Payroll HSA contributions skip both federal income tax and FICA taxes (7.65%), which includes Social Security and Medicare. Direct contributions only avoid income tax. The California SDI rate and payroll deduction guide explains how each payroll tax layer stacks — useful context when you are deciding how to structure HSA contributions. If payroll deduction is available, use it. The FICA savings compound meaningfully over a career.

Takeaway: Payroll HSA contributions save more tax than direct contributions because they avoid FICA taxes too.

What Happens If You Contribute Too Much?

Excess Contribution Penalties

The IRS charges a 6% excise tax on every excess dollar, every year it stays in your account. On top of that, excess amounts lose their tax-free growth status. A $500 over-contribution costs $30 per year until corrected.

Takeaway: Excess HSA contributions trigger a 6% annual penalty that keeps hitting until you fix the problem.

How to Fix an Over-Contribution

Contact your HSA provider and withdraw the excess plus any earnings it generated. Do this by the tax filing deadline — October 15, 2027 if you file an extension for 2026. The withdrawn amount is taxable income. Earnings on the excess may also owe a 10% additional tax. Use the IRS Form 8889 instructions to report the correction correctly on your return.

Takeaway: Withdraw excess HSA contributions by the tax deadline to avoid the 6% annual penalty.

Common Causes of Excess Contributions

The top cause: forgetting employer contributions count. Someone contributes the full $8,750, then notices their employer deposited $1,000 in January — they are $1,000 over. Mid-year coverage switches that reduce the limit also create excess if contributions were already made at the higher rate. Multiple HSA account holders often lose track of the combined total. The paycheck basics category on this site covers how to track every deduction type so nothing slips through.

Takeaway: Track employer contributions and any mid-year coverage changes carefully to avoid going over your limit.

Common HSA Myths Debunked

Myth: Employer Contributions Are Separate from IRS Limits

Wrong. Every employer dollar counts toward the same $4,400 or $8,750 ceiling. If your employer contributes $1,000 to your self-only HSA, you can only add $3,400 more.

Takeaway: Employer HSA deposits and your own contributions are added together against one shared IRS limit.

Myth: You Lose Unused HSA Funds

HSA money never expires. It rolls over every year, stays in your account through job changes, plan switches, and retirement, and you own it permanently. If you withdraw before age 65 for non-medical expenses, you owe income tax plus a 20% penalty. After 65, the penalty disappears and non-medical withdrawals are taxed like a traditional IRA.

Takeaway: HSA funds roll over every year and stay yours forever, but non-medical withdrawals before age 65 carry a 20% penalty.

Myth: Family Coverage Means Unlimited Family Contributions

The $8,750 family cap is a household total — not per person. Every dollar across all HSAs in the household counts toward that one ceiling.

Takeaway: The family HSA limit of $8,750 is a shared household cap, not a per-person amount.

Myth: You Must Contribute Monthly

You can contribute any amount at any time. One lump sum in January, one in December, or whenever you have cash — it all works. The only rule is staying under the annual limit and making contributions by April 15 of the following year.

Takeaway: You can contribute to your HSA in any amount at any time throughout the year.

Common HSA Contribution Mistakes to Avoid

Forgetting Employer Contributions Count

Set your payroll deduction before you know your employer’s 2026 deposit amount, and you risk going over. Ask HR what your employer will contribute, subtract it from the IRS limit, and set your own deduction to cover only the gap.

Takeaway: Always find out your employer’s 2026 HSA contribution before setting your own contribution amount.

Misunderstanding Family Coverage Rules

Each spouse does not get their own family limit. Two separate self-only HDHPs: each gets $4,400. One family HDHP: the household shares $8,750. Two separate family HDHPs: the household still shares $8,750 and must split it. If your situation involves both spouses working, the paycheck scenarios category walks through dual-income household examples in detail.

Takeaway: The IRS family limit of $8,750 applies to the household, regardless of how many separate HSAs exist.

Ignoring Mid-Year Eligibility Changes

Marriage, job change, a new dependent, Medicare enrollment — any of these can change your coverage type or cut off eligibility entirely. Recalculate your prorated limit every time your situation changes. If a job change is involved, the part-time vs full-time paycheck comparison shows how benefit eligibility and withholding shift when your hours or employment status changes.

Takeaway: Recalculate your prorated limit anytime your coverage or eligibility changes during the year.

HSA Contribution Strategies to Maximize Tax Savings

How Much Should You Actually Contribute?

Start by estimating your likely out-of-pocket medical costs for the year — typically $2,000 to $5,000 for most families. Fund that first. Then push toward the full limit. A family at the 24% bracket contributing $8,750 saves $2,100 in federal taxes alone, more in most states.

For priority order: capture your full 401(k) employer match first, then max your HSA, then return to your IRA or 401(k). California employers with five or more employees are now required to offer retirement savings access under the CalSavers mandate, so if no workplace plan exists, CalSavers is an option before you hit the HSA limit. If you have a Limited Purpose FSA available, use it for dental and vision to keep your HSA balance growing.

Takeaway: Capture your 401(k) match, then max your HSA, then fund your IRA — in that order.

Using an HSA as a Retirement Tool

Invest your HSA balance in mutual funds or ETFs. Let it grow tax-free for decades. Use it in retirement for Medicare premiums, dental, vision, and long-term care — all qualified medical expenses. The triple tax advantage makes the HSA the most efficient savings vehicle in the U.S. tax code. People who pay current medical costs out of pocket and let the HSA compound consistently come out ahead at retirement. To see what a maximized pre-tax strategy does to long-term take-home pay, the payroll compliance and reporting category covers the reporting side of employer-sponsored benefit programs.

Takeaway: Investing your HSA for retirement medical costs delivers the best long-term tax benefit of any account.

Frequently Asked Questions

What is the HSA contribution limit for 2026?

$4,400 for self-only HDHP coverage and $8,750 for family coverage, per IRS Revenue Procedure 2025-19, effective January 1, 2026. Add $1,000 if you are 55 or older.

Does my employer contribution count toward my HSA limit?

Yes. Employer and employee contributions share the same $4,400 or $8,750 ceiling. Always check your employer’s deposit before setting your own.

Can I contribute to an HSA if I am on Medicare?

No. Medicare Part A or Part B enrollment stops eligibility from that month forward. You can still spend your existing HSA balance tax-free on qualified expenses.

What happens if I exceed the HSA contribution limit?

A 6% excise tax applies to the excess every year until you remove it. Withdraw the excess plus earnings by your tax filing deadline to correct it. The withdrawn amount is taxable income.

Can my spouse and I each contribute the family maximum?

No. The $8,750 is a combined household cap. On separate self-only HDHPs, each spouse gets $4,400. If both are 55+, each gets a separate $1,000 catch-up — but each needs their own HSA.

How do catch-up contributions work after age 55?

You can add $1,000 per year on top of the regular limit. Both spouses can each claim $1,000 if both are 55+, but each must have their own separate HSA.

Can I contribute for a previous tax year?

Yes, until April 15 of the following year. Tell your HSA provider which tax year the contribution applies to. A filing extension does not extend this deadline.

What if I change from self-only to family coverage during the year?

Your limit is blended: multiply $366.67 by your self-only months and $729.17 by your family months, then add both totals.

Can I have multiple HSA accounts?

Yes, but combined contributions across all accounts cannot exceed your annual limit. Consolidating accounts over time makes tracking easier.

Is an HSA better than an FSA?

For HDHP enrollees, the HSA wins. Funds roll over indefinitely, the account is portable, and growth is tax-free. FSA funds generally expire annually and are employer-tied. FSAs suit people on lower-deductible plans who cannot use an HSA.

Key Takeaways

The 2026 HSA limits are $4,400 (self-only) and $8,750 (family). Age 55+ adds $1,000 per eligible person, each in their own separate HSA account.

You need a qualifying HDHP with at least a $1,700 self-only or $3,400 family deductible. Bronze and Catastrophic ACA plans now qualify as of 2026. Medicare enrollment, non-HDHP coverage, and dependent tax status all cut off eligibility.

Employer contributions count toward your limit. Exceed it and you pay 6% per year until corrected. Your deadline to contribute for 2026 is April 15, 2027. Report everything on IRS Form 8889. If you want to see exactly how your HSA contribution affects your California take-home pay, use the California paycheck calculator to model any scenario.

Your action plan: Get your employer’s 2026 HSA deposit amount. Subtract it from your limit. Set payroll deductions to fill the gap. If 55+, open a separate HSA for your catch-up. Confirm your plan qualifies. Adjust payroll now. Maximize every year.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.