On a $75,000 salary in California, a single W-2 filer takes home roughly $54,500 to $57,000 per year after taxes. Add real-world benefit deductions and most people deposit $3,900 to $4,300 per month.

After 8 years walking employees through their first California paychecks, I have seen this pattern: the effective tax rate lands between 24% and 29%, yet most people only feel the 1.3% SDI and state brackets hitting at the same time.

That comfort level breaks fast in San Francisco or Los Angeles, where rent alone can consume 45% of gross income.

This guide is built for a single filer using the standard deduction, no dependents, and W-2 employment. If that is your situation, you are in the right place.

Quick Answer: How Much Is $75K After Taxes in California?

On a $75,000 California salary, your tax-only take-home is $54,500 to $57,000 per year ($4,500 to $4,750/month). Once real-world deductions like health insurance and a 401(k) are included, most people deposit closer to $3,900 to $4,300 per month. Effective tax rate lands around 24% to 29% depending on filing status and pre-tax contributions.

Here is the fast breakdown (taxes only, before benefit deductions):

- Annual net pay (tax only): approximately $54,500 to $57,000

- Monthly take-home (tax only): roughly $4,500 to $4,750

- Monthly take-home (with benefits): approximately $3,900 to $4,300

- Biweekly paycheck: around $2,027 to $2,200

- Weekly equivalent: approximately $1,013 to $1,096

- After-tax hourly rate: about $25 to $27 per hour

Takeaway: On a $75K salary in California, you keep roughly 70 to 76 cents of every dollar you earn, depending on your benefit elections.

Free California Tax Tool

Calculate What You’ll Actually Take Home

Stop guessing. Enter your California salary and see your real paycheck — federal tax, state tax, SDI, and all deductions included.

🧮 Calculate What You’ll Actually Take HomeUsed by thousands of California workers · FTB-verified 2026 rates

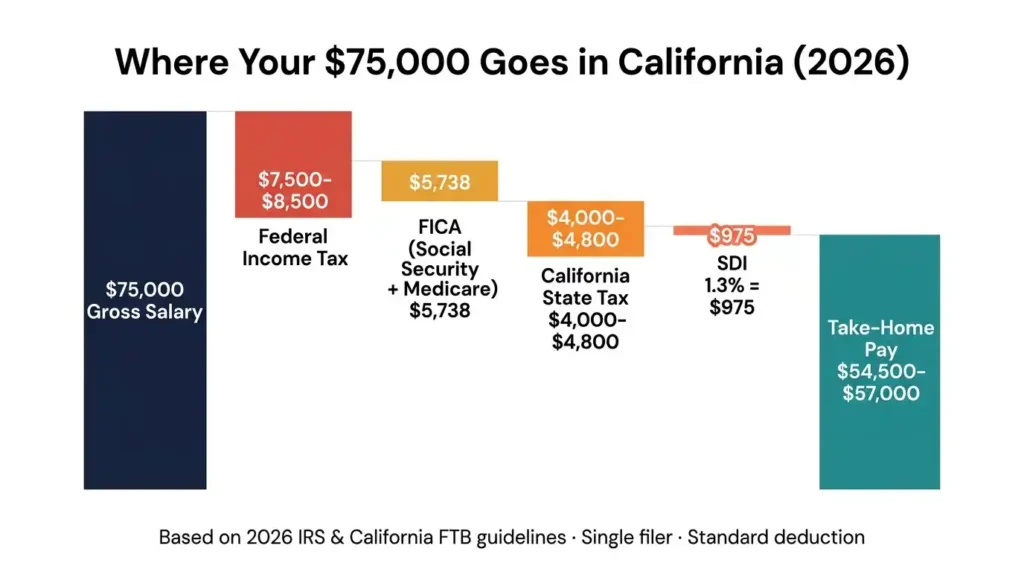

Estimated Annual Tax Breakdown for $75K in California (2026)

Here is where your $75,000 goes before it reaches your account.

Estimated Annual Tax Breakdown

Four buckets pull from your $75,000 before a dollar reaches your account: federal income tax, FICA payroll taxes, California state income tax, and SDI. The numbers below apply to a single filer using 2026 standard deductions with no additional income sources. If you are married filing jointly, your take-home will be noticeably higher. The MFJ standard deduction is $32,200 federally and $11,080 for California, which significantly lowers taxable income at both levels and can add $200 to $400 more per month to your deposit compared to a single filer on the same salary.

Federal Income Taxes

Federal income tax is progressive. Different income slices are taxed at different rates. You never pay one flat rate on all $75,000.

For 2026, single filers start with a standard deduction of $16,100 (extended permanently by the One Big Beautiful Bill Act signed in July 2025). According to the IRS Publication 501, the standard deduction is adjusted annually for inflation and automatically applies to all W-2 filers who do not itemize. That brings your federal taxable income down to about $58,900. Your federal income tax bill comes out to roughly $7,260 to $8,000 for the year.

Your marginal federal rate at $75K is 22%, but your effective rate (what you actually pay on the full $75K) is closer to 10% to 11%. Confusing these two numbers is one of the most common reasons people feel blindsided by their paycheck.

Takeaway: You do not pay 22% on all $75,000. You only pay 22% on the dollars that fall inside that bracket.

FICA Taxes: Social Security and Medicare

Every W-2 employee pays FICA. No exceptions. These are part of your broader California payroll taxes that combine to reduce your gross pay before a dollar reaches your bank account.

- Social Security: 6.2% on wages up to $168,600 (2026 cap, confirmed by the Social Security Administration). On $75K, that is about $4,650 per year.

- Medicare: 1.45% on all wages with no cap. On $75K, that is about $1,088 per year.

Together, FICA takes roughly $5,738 per year from your gross pay. Your employer matches this amount on their end, but you never see that money.

Takeaway: FICA is automatic and unavoidable on W-2 income. Budget for it from day one.

California State Taxes: State Income Tax and SDI

California’s state tax structure catches most people off guard, especially those relocating from other states.

California has 9 progressive tax brackets ranging from 1% to 12.3%. An extra 1% Mental Health Services Tax applies to income over $1 million. At $75,000, a single filer falls mostly into the 9.3% bracket, which applies to income between $70,607 and $371,479.

California’s standard deduction is only $5,706 for single filers, compared to the federal $16,100. That $10,394 gap means your California taxable income is significantly higher than your federal taxable income, which is why the state tax bill feels heavier than the bracket rate alone suggests. For a deeper look at how this deduction works, see our guide on the California standard deduction for 2026.

Your California state income tax for 2026 is estimated at $4,000 to $4,800 per year for a single filer. This accounts for the $5,706 standard deduction, the progressive bracket structure, and the $144 personal exemption credit California allows single filers.

Then there is SDI (State Disability Insurance). The 2026 SDI rate is 1.3%, up from 1.1% in 2024 and 1.2% in 2025. On a $75K salary, SDI costs you approximately $975 per year or about $38 per biweekly paycheck. SDI funds short-term disability benefits and Paid Family Leave, which provides 60% to 70% wage replacement. The official rates and eligibility rules are published by the California Employment Development Department (EDD).

Takeaway: California’s low state standard deduction and rising SDI rate make your state-level tax burden feel heavier than the headline rate suggests.

Full Tax Summary Table for $75K in California (2026)

| Tax Type | Estimated Annual Amount |

|---|---|

| Federal Income Tax | $7,500 to $8,500 |

| Social Security (6.2%) | $4,650 |

| Medicare (1.45%) | $1,088 |

| California State Income Tax | $4,000 to $4,800 |

| California SDI (1.3%) | $975 |

| Total Estimated Taxes | $18,213 to $20,013 |

| Estimated Take-Home Pay (taxes only) | $54,500 to $57,000 |

Figures are estimates for a single filer using the 2026 standard deduction. Actual withholding varies by pay frequency, W-4 elections, and employer payroll settings.

Paycheck Frequency Breakdown

Monthly Take-Home Pay

After all taxes, expect roughly $4,500 to $4,750 per month before employer benefit deductions. Health insurance, a 401(k), or other workplace programs will reduce your actual deposit below this number.

Biweekly Paycheck (Most Common Pay Schedule)

Most California employers pay biweekly. That means 26 paychecks per year. On $75K, each paycheck brings in roughly $2,027 to $2,180 after taxes. Two months per year will have a third paycheck. Treat it as a savings deposit, not extra spending money.

Weekly Pay Equivalent

Weekly, that comes to about $1,013 after taxes. Useful for comparing to hourly or contractor pay rates. If you are weighing W-2 employment against a 1099 contract offer, see our 1099 vs W-2 comparison for California workers to understand the full tax difference. For more on how paycheck schedules work in California, browse our paycheck basics guides.

Takeaway: Knowing your weekly number helps you build a budget that matches how money actually flows through your life.

Why Your Real Paycheck May Be Lower Than Online Calculators Show

Online tax calculators only estimate your tax withholding. They skip the other deductions your employer pulls before you ever see a deposit. What calculators show is your “tax take-home.” What lands in your bank account is your “real take-home.” Those two numbers are often hundreds of dollars apart. If your paycheck looks much smaller than expected, our breakdown of why your California paycheck is so low explains the six most common causes.

Common Payroll Deductions Employees Forget

Most full-time employees in California have these deductions coming out before they ever see their paycheck:

- Health insurance premiums (employer-sponsored plans average $150 to $400 per month for a single person)

- Dental and vision coverage ($10 to $50 per month combined)

- 401(k) contributions (even a 3% contribution on $75K removes $187 per month pre-tax)

- HSA or FSA contributions (health savings accounts that reduce taxable income)

- Commuter benefits (pre-tax transit or parking deductions)

- ESPP programs (Employee Stock Purchase Plans, common in tech)

One extra point many employees miss: bonuses and RSUs are taxed differently from regular salary. California withholds a flat 10.23% on supplemental wages like bonuses, and the federal supplemental rate is 22%. If you receive a $5,000 year-end bonus, expect to net roughly $3,300 to $3,500 after taxes, not the full amount.

Example of a Real California Pay Stub

Calculators say your monthly take-home is $4,542. A real pay stub tells a different story. If you have never decoded each line on your paycheck before, our guide on how to read a California pay stub in 2026 walks through every field:

- Estimated monthly tax take-home: $4,542

- Health insurance premium: -$280

- 401(k) at 5% contribution: -$312

- Dental and vision: -$35

- Actual monthly bank deposit: approximately $3,915

That is a $627 monthly gap. Over a year, $7,524 less than the calculator promised. Your budget must start with the real deposit number, not the calculator estimate.

Takeaway: Always check your actual pay stub, not just an online calculator, to know your true monthly budget.

Reality Check: Is $75K Actually a Good Salary in California?

Yes and no. Where you live matters far more than the salary number itself.

At $75,000, you sit just above the California median income of $74,068 at the 51st percentile, according to U.S. Census Bureau American Community Survey data. That is a solid starting point. But city choice determines whether it feels comfortable or tight.

Why $75K Sounds Bigger Than It Feels

People call this “gross salary psychology.” You mentally compare $75K in California to $75K in a state where rent runs $900. Then you arrive and rent quotes start at $2,200. That is not a salary flaw. It is a cost-of-living mismatch.

Recent graduates and relocating professionals are most vulnerable to this. The salary shock hits in month one. A little planning before you sign the lease prevents it entirely.

Is $75K Middle Class in California?

California’s middle class spans $59,896 to $91,357 per year. At $75,000, you are squarely in it. But California’s middle class means covering rent and bills. It does not mean saving aggressively or living without financial pressure.

What Type of Lifestyle $75K Can Support

Your lifestyle on $75K depends on where you live, whether you have roommates, and how disciplined your budget is. In Sacramento or Fresno, it feels comfortable. In San Francisco or Santa Monica, it feels tight even with smart budgeting.

Takeaway: Your zip code determines your quality of life on $75K more than the tax rate does.

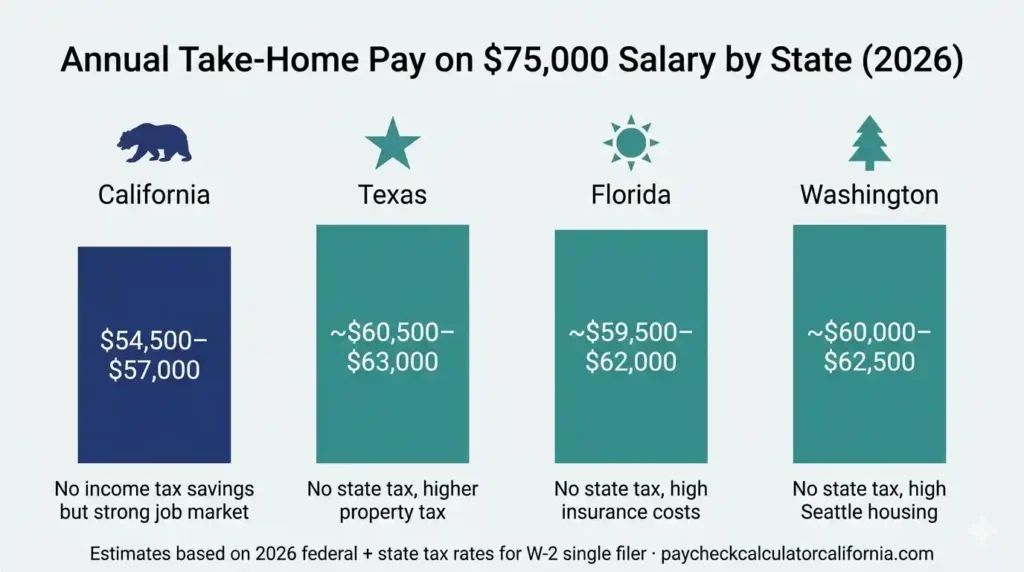

California vs. No-Income-Tax States on a $75K Salary

This comparison comes up constantly. Someone in Texas offers $70K and someone in California offers $75K. Which is actually better? The answer is rarely what people expect.

California vs. Texas

Texas has no state income tax. On the same $75K salary, a Texas resident keeps roughly $6,000 more per year than a California resident after taxes. That is a real and meaningful difference.

But Texas has significantly higher property taxes if you own a home. And housing in major Texas metros like Austin and Dallas has risen sharply. The cost-of-living gap has narrowed in recent years, especially in the tech corridors where most of these salary comparisons happen.

California vs. Florida

Florida also has no state income tax. The take-home comparison looks similar to Texas, with California workers losing roughly $5,000 to $6,000 per year to state income taxes. Florida’s homeowners insurance costs, however, have spiked significantly in recent years. This eats into the financial advantage for buyers and renters in coastal areas.

California vs. Washington

Washington has no state income tax, making it a frequent comparison for tech workers eyeing Seattle. The take-home advantage mirrors Texas and Florida. However, Seattle’s cost of living has risen sharply, which narrows the real difference for most workers.

Insider Insight: A $68,000 salary in Sacramento can outperform an $80,000 salary in San Francisco once you subtract housing costs. The number on the offer letter is never the full story. Always run the after-housing math before you decide.

Takeaway: Comparing salaries across states requires looking at taxes AND housing costs together, never separately.

Monthly Budget Reality on a $75K Salary in California

Here is a realistic monthly budget using $4,100 as the base, which accounts for typical benefit deductions most employees carry.

Example Budget: Living Alone

| Category | Monthly Cost |

|---|---|

| Rent (1BR, mid-tier CA city) | $1,800 to $2,200 |

| Utilities and Internet | $150 to $200 |

| Groceries | $350 to $450 |

| Transportation (car or transit) | $300 to $500 |

| Health/auto/renters insurance | $150 to $250 |

| Entertainment and dining out | $200 to $300 |

| Savings contributions | $100 to $300 |

| Total | $3,050 to $4,200 |

Living alone on $75K in a mid-cost California city is possible. But savings room is thin, especially in higher-rent markets. A $2,200 rent leaves very little buffer.

Example Budget: With Roommates

Sharing a two or three-bedroom apartment cuts your housing cost to $900 to $1,400 per month, freeing up $600 to $900 every month for emergency savings, retirement, or debt payoff.

Roommate living at this income level is not a compromise. It is a strategy. Two years of shared housing can build a down payment foundation or eliminate student debt significantly faster.

Example Budget: Remote Worker Lifestyle

Remote workers have a unique advantage at $75K in California. You can live in Sacramento, Fresno, or Riverside while earning a salary calibrated to a higher-cost market. Your housing cost drops to $1,000 to $1,400. Your commuting cost drops to near zero. Your savings rate can jump to 15% to 20% per month without lifestyle sacrifice.

Takeaway: Remote work is the most underrated financial upgrade available to California workers earning $75K.

Apartment Affordability on a $75K Salary

The standard rule for rent affordability says you should spend no more than 30% of your gross monthly income on housing. On $75K, that is $6,250 per month gross, which means a recommended rent ceiling of $1,875 per month.

That number is realistic in inland California cities. It is a stretch in Los Angeles. It is nearly impossible in San Francisco.

Can You Afford a Studio Apartment?

In Los Angeles, studio apartments average $1,800 to $2,100 per month in mid-tier neighborhoods. That sits right at or slightly above the 30% rule. It is doable but leaves no room for savings surprises.

In Sacramento, studios average $1,100 to $1,400. That fits comfortably within the 30% guideline and leaves meaningful budget room. Sacramento is where $75K actually feels like a solid middle-class income in 2026.

Should You Live Alone or With Roommates?

Living alone on $75K in California requires a strategic city choice. In high-cost metros, solo living often means spending 35% to 45% of gross income on rent, which compresses savings and emergency funds to near zero.

Roommate living at this income level is not a financial weakness. It is a tool. Workers who choose shared housing for two to three years while earning $75K typically accelerate their savings and investment timelines by three to five years.

Can You Save Money While Renting on $75K?

Yes. But not in every California city. In Sacramento, Riverside, Bakersfield, or Fresno, you can save $500 to $900 per month while renting comfortably. In San Francisco or Santa Monica, saving more than $200 to $300 per month requires aggressive budgeting or roommates.

Here is what saving realistically looks like across three key goals:

- Emergency fund: In lower-cost cities, building a 3-month emergency fund ($12,000 to $15,000) takes 12 to 18 months. In high-cost metros, it can take 3 or more years.

- Retirement savings: A 5% 401(k) contribution on $75K is $312 per month. Combined with any employer match, this builds meaningful long-term savings even on a tight budget.

- Debt payoff: Student loans or credit card balances compete directly with savings goals. In inland cities, extra income after rent allows $200 to $400 per month toward debt payoff. In coastal cities, that room often disappears.

Takeaway: The 30% rule is your rent compass. Choose a city where your rent fits inside it, and your finances will stay healthy.

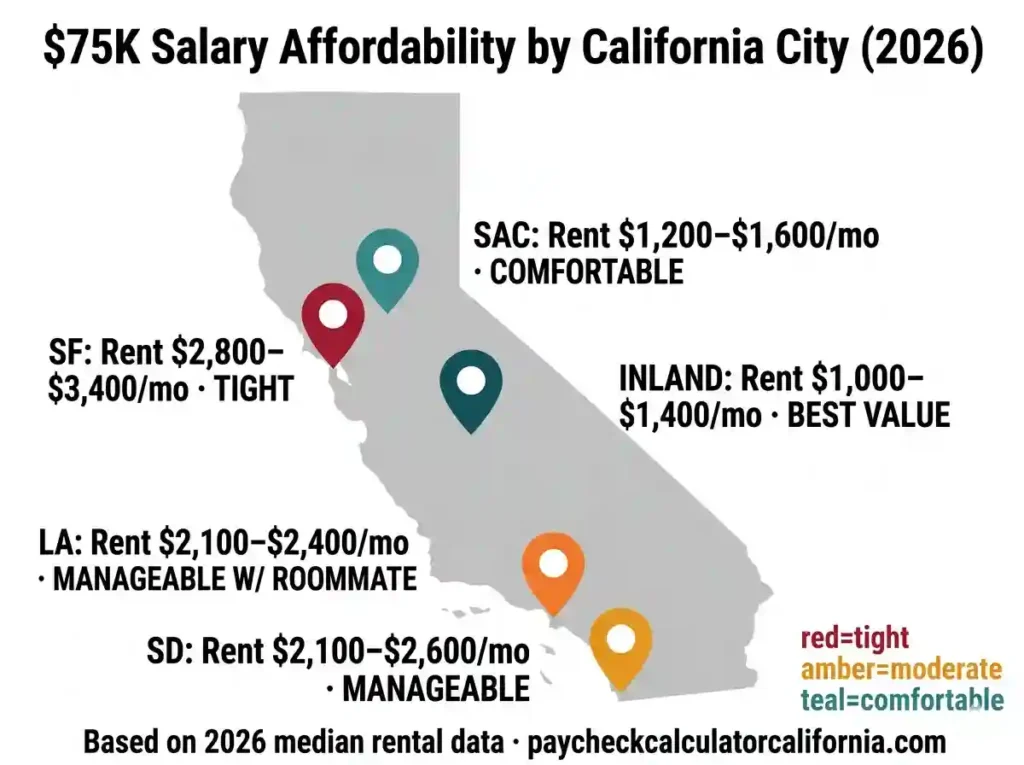

What $75K Looks Like Across California Cities

Los Angeles

Average one-bedroom rent in Los Angeles sits at $2,100 to $2,400 per month in 2026. At $75K, that means 34% to 38% of gross monthly income goes to rent alone. Transportation costs are high because LA requires a car for most commutes. Lifestyle is possible but budgeting needs to be intentional. Use the Los Angeles paycheck calculator to model your exact net pay with LA-specific deductions.

San Francisco

San Francisco is the most financially demanding major city in California. Average one-bedroom rent runs $2,800 to $3,400 per month, meaning solo living on $75K consumes 45% to 55% of gross income on housing alone. Public transit is strong, which helps offset car costs, but the math remains very tight. Even six-figure earners in San Francisco describe feeling financially squeezed. Run your numbers with the San Francisco paycheck calculator to see your exact monthly deposit.

San Diego

San Diego costs slightly less than San Francisco but more than LA inland neighborhoods. Average one-bedroom rent runs $2,100 to $2,600 per month. Coastal proximity adds a lifestyle premium. Overall, San Diego on $75K is manageable with careful budgeting and roommates or a partner. The San Diego paycheck calculator can show your exact take-home given San Diego’s local minimum wage and payroll rules.

Sacramento

Sacramento is the best financial fit for $75K earners in California right now. Average one-bedroom rent sits at $1,200 to $1,600 per month. That falls comfortably within the 30% guideline. Purchasing power is meaningfully higher. Career opportunities have grown significantly as remote work normalized and workers have relocated from the Bay Area. The Sacramento paycheck calculator can show you exactly what your biweekly deposit looks like in this city.

Inland California Cities: Fresno, Bakersfield, Riverside

These cities offer the strongest purchasing power on $75K. Rents average $1,000 to $1,400 per month for a one-bedroom. Groceries and transportation cost less. The tradeoff is fewer high-paying job opportunities locally, which matters if you are not remote. For remote workers, these cities represent a significant financial advantage.

Takeaway: The same $75K salary generates a different quality of life depending entirely on which California city you choose to live in.

How Taxes Actually Work on a $75K Salary in California

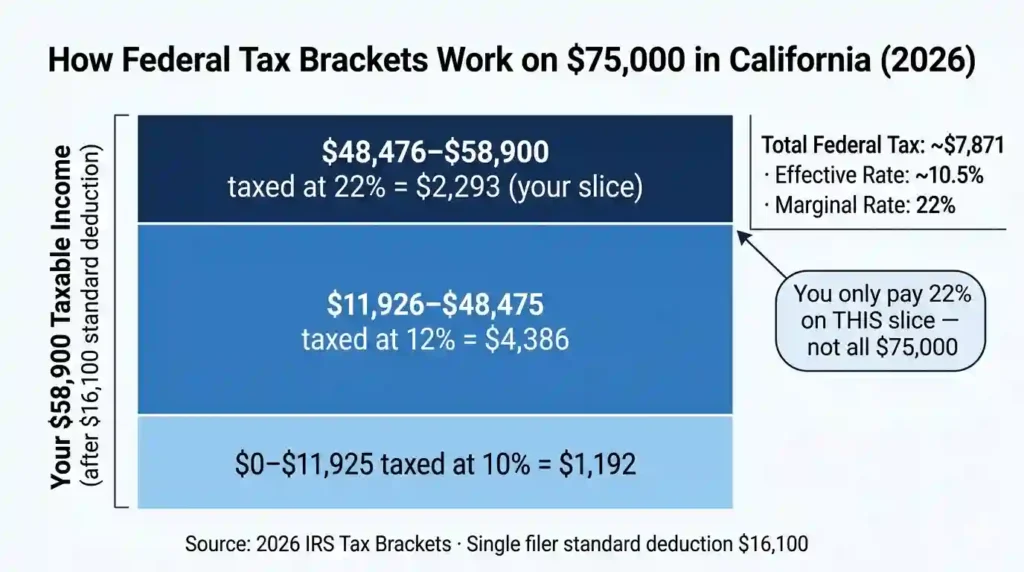

Federal Income Tax Explained

The federal tax system uses progressive brackets. Think of it like filling buckets in order. Your first dollars fill the lowest-rate bucket. Only when that is full do your dollars move to the next one.

Tax Brackets

For 2026, single filers pay:

- 10% on the first $11,925 of taxable income

- 12% on income from $11,926 to $48,475

- 22% on income from $48,476 to $103,350

Standard Deduction

The 2026 federal standard deduction is $16,100 for single filers. This is the amount subtracted from your gross income before any bracket math happens. It is the single biggest built-in tax break most W-2 workers use automatically.

Marginal vs. Effective Tax Rate

After the $16,100 standard deduction, your taxable federal income on $75K is about $58,900. You pay 22% only on the slice above $48,475. Your overall effective federal rate stays around 10% to 11%. The marginal rate is what your next dollar is taxed at. The effective rate is what you actually paid across the whole income.

FICA Taxes Explained

Every W-2 worker pays FICA. It is not optional and does not change based on how you file.

Social Security

Social Security takes 6.2% on wages up to $168,600. On $75K, that is $4,650 per year. This program provides retirement and disability income. Your employer matches your contribution behind the scenes.

Medicare

Medicare takes 1.45% on all wages with no income cap. On $75K, that is $1,088 per year. These funds pay for healthcare coverage for Americans over 65. Like Social Security, your employer matches this amount.

Why Every W-2 Employee Pays These

FICA withholding is mandatory for all W-2 employees regardless of hours or pay structure. These deductions appear on every single paycheck. Your employer matches them dollar for dollar, but that match comes from their budget, not yours.

California State Tax System

California runs its own separate tax system. It does not follow federal rules on deductions or brackets. All California income tax rules are administered by the California Franchise Tax Board (FTB), which publishes the official withholding schedules and bracket thresholds each year.

Progressive California Brackets

California’s 9 brackets create a progressive climb from 1% to 12.3%. The key bracket for a $75K earner is 9.3%, which starts at $70,607 for single filers in 2026. Because California’s standard deduction is only $5,706, most of your $75K sits inside the 9.3% bracket at the state level. For the full bracket table, see our California income tax brackets for 2026.

SDI Payroll Deductions

The 2026 SDI rate is 1.3% on all wages. There is no wage cap. On $75K, this costs you $975 per year. SDI funds short-term disability and Paid Family Leave benefits. The rate increased from 1.1% in 2024 to 1.2% in 2025 and now 1.3% in 2026.

Why California Taxes Feel Higher

California’s standard deduction is $5,706 compared to the federal $16,100. That $10,394 gap means your California taxable income is meaningfully higher than your federal taxable income. Add the uncapped SDI and the 9.3% bracket that kicks in early, and the state-level burden adds up faster than most people expect.

Takeaway: California’s progressive system means your last dollars earned are taxed harder than your first ones. Understanding this prevents tax anxiety when you see your paycheck.

Common Mistakes People Make When Evaluating a $75K Salary

In 8 years of walking people through salary decisions, I have seen the same errors repeat. Here are the ones that cost people the most.

- Ignoring benefit deductions. Calculators show your tax take-home. Your real take-home is $300 to $700 lower after health insurance and retirement deductions.

- Underestimating rent inflation. California rents have continued rising. The apartment you budgeted for in your research may cost more when you actually sign the lease.

- Forgetting commuting costs. In LA, gas, a car payment, insurance, and parking can easily cost $700 to $1,200 per month combined. California gas prices are among the highest in the nation. Parking alone in downtown San Francisco or LA can run $200 to $400 monthly. These expenses do not appear in any tax calculator but they hit your budget just as hard.

- Assuming take-home equals spending money. Take-home is your total budget. Savings, emergencies, and debt payments all come from it.

- Neglecting retirement savings. At $75K in California, every dollar you put into a 401(k) reduces your taxable income and saves you money at both the federal and state level.

- Moving to a high-cost city without a budget. Accepting a San Francisco offer without modeling monthly expenses is how people end up financially stressed on what sounded like a great salary.

How to Increase Your Take-Home Pay Legally

Increase 401(k) Contributions

Every dollar you put into a traditional 401(k) reduces your federal and California taxable income. A $5,000 annual contribution saves you approximately $1,150 in combined federal and state taxes at your income level. The IRS sets the annual 401(k) contribution limit each year — for 2026 the employee limit is $23,500 for those under 50. If your employer offers a match, you are leaving money on the table by not contributing at least enough to capture the full match.

Use an HSA or FSA

A Health Savings Account (HSA) lets you set aside pre-tax dollars for medical expenses. A $3,000 HSA contribution in 2026 saves roughly $500 to $700 in federal taxes at your income level. However, California is one of only two states that does not conform to the federal HSA tax exclusion. Your HSA contributions are still subject to California state income tax, so the state savings do not apply. The federal benefit alone still makes an HSA worthwhile for most W-2 workers.

Adjust Your W-4 Withholding

Many California workers over-withhold and effectively give the government an interest-free loan all year. Adjusting your W-4 to reflect your actual deductions and situation gives you more cash each month. Use the IRS Tax Withholding Estimator to find your ideal withholding number. California also requires a separate California DE-4 form for state withholding, which many employees never update after their first day of work.

Negotiate Total Compensation Instead of Base Salary

A raise from $75K to $80K nets about $3,000 extra per year after California taxes. But negotiating remote work flexibility can be worth $5,000 to $10,000 in commuting savings alone. Strong healthcare benefits can save another $2,000 to $4,000 over a basic plan. The base salary is rarely where the real value lives.

Push beyond the base number when negotiating. Real value often hides here:

- Remote flexibility: Living in Sacramento instead of SF can add $600 to $1,000 per month in purchasing power

- Healthcare quality: A strong employer plan saves $2,000 to $4,000 versus buying coverage independently

- Bonuses and equity: Annual bonuses and stock grants can meaningfully lift your total yearly income

- PTO and commuter benefits: More paid time off and pre-tax commuter passes reduce your real cost of working

Pro Tip: Flexible remote work that lets you live in Sacramento instead of San Francisco is worth more than a $10,000 base salary increase in most California market comparisons. I have run this math for dozens of clients and it holds up every time.

Takeaway: Legal tax optimization through retirement accounts and benefit elections can increase your real take-home by $2,000 to $5,000 per year without a single raise.

Who Can Live Comfortably on $75K in California?

Single Professionals

A single professional earning $75K can live comfortably in Sacramento, Fresno, Riverside, or other inland cities. In coastal metros, comfort requires roommates or very disciplined budgeting. Savings are possible but require intentional choices about housing and lifestyle.

Couples With Dual Income

Two partners each earning $75K creates a household income of $150K. This changes the California math dramatically. Housing costs split in half. Savings rates climb. Coastal city living becomes genuinely comfortable. A dual-income household at this level can pursue homeownership, travel, and retirement savings simultaneously. If one partner earns more, see how a $100K salary is taxed in California for the next income tier comparison.

Remote Workers

Remote workers have the most flexibility. Choosing an inland California city over a coastal one adds $600 to $1,200 in effective monthly purchasing power on the same $75K salary. That is the clearest path to financial comfort at this income level in 2026.

Families With Children

Single-income families with children face real pressure at $75K in California. Childcare alone costs $1,500 to $2,500 per month in most California cities. Add housing, transportation, and groceries, and the budget becomes extremely tight. Families in this situation benefit most from dual income, employer-sponsored childcare benefits, and strategic city selection.

Takeaway: Your household structure matters as much as your salary. A single earner at $75K and a dual-income couple at $75K each live in completely different financial realities.

Reality Myths About $75K Salaries in California

Myth 1: “$75K Means You Are Rich”

At $75,000 in California, you sit just above the median income at the 51st percentile. That is not rich. It is solidly middle class. Housing costs, taxes, and inflation make this salary a working-income level that requires budgeting, not a wealth-building machine on autopilot. The perception of richness comes from comparing this number to salaries in lower-cost states.

Myth 2: “California Taxes Take Half Your Income”

This is the most common misunderstanding I encounter. Your effective total tax rate on $75K is approximately 24% to 29%, not 50%. The confusion comes from people quoting California’s top marginal rate of 13.3%, which only applies to income over $1 million. At $75K, your California state effective rate is closer to 7% to 8%. California also has the highest statewide sales tax in the nation at 7.25%, with local add-ons pushing the average combined rate to around 8.68% in many areas. That does reduce purchasing power on everyday spending, but it is a far cry from “half your paycheck.”

Myth 3: “You Cannot Survive on $75K in California”

You can. Millions of Californians do. The key word is strategy. City choice, housing arrangement, and benefit optimization determine whether $75K is a struggle or a solid foundation. In Sacramento with a roommate and a 401(k), this salary supports a genuinely good life with savings growth.

Takeaway: California taxes are high but not as high as the myths suggest. Smart city selection matters more than tax avoidance.

Best Tools to Calculate Your Exact California Take-Home Pay

Different calculators show different numbers because they make different assumptions about pre-tax deductions, benefit elections, and withholding methods. Here is what you need to get an accurate result. For the most accurate 2026 estimate, use our California paycheck calculator which applies current SDI rates, updated state brackets, and accounts for your specific pay frequency.

What Information You Need for Accurate Results

Gather these details before using any calculator:

- Filing status (single, married filing jointly, head of household)

- Pay frequency (biweekly, semi-monthly, weekly)

- 401(k) contribution percentage or dollar amount

- Health insurance premium deducted from paycheck

- HSA or FSA contribution amounts

- Any bonus income expected during the year

- Number of allowances or additional withholding on your W-4

Why Different Calculators Show Different Results

Some calculators use the 2025 SDI rate instead of 2026. Some ignore pre-tax benefit deductions entirely. Some use older California bracket thresholds before CPI indexing adjustments. The most reliable approach is to look at your actual pay stub from your employer and use that as your ground truth.

Takeaway: Your pay stub is always more accurate than any online calculator. Use calculators for estimates and your actual stub for real budgeting.

Frequently Asked Questions

How Much Is $75K After Taxes Monthly in California?

For a single filer using the standard deduction, your estimated monthly take-home is approximately $4,500 to $4,750 per month before employer benefit deductions.

How Much Is Each Paycheck If I Make $75K in California?

On a biweekly pay schedule (26 paychecks per year), your estimated paycheck is $2,027 to $2,180 after taxes. This does not include deductions for benefits like health insurance or 401(k) contributions.

Is $75K a Good Salary in California?

Yes, $75K is a good salary in California by income percentile standards. It places you above 51% of California earners. Whether it feels good depends heavily on your city and lifestyle. In Sacramento it is comfortable. In San Francisco it is tight.

Is $75K Middle Class in California?

Yes. The middle-class income range in California is approximately $59,896 to $91,357 per year. At $75,000, you are solidly in the middle of that range.

Can I Live Alone in California Making $75K?

You can live alone in inland California cities like Sacramento, Fresno, or Bakersfield comfortably. Living alone in Los Angeles requires disciplined budgeting. Living alone in San Francisco on $75K means spending an unsustainably high percentage of your income on rent.

Can I Buy a House in California on $75K?

Buying a house in California on $75K as a single earner is extremely difficult in 2026. The median home price statewide exceeds $800,000. Most mortgage lenders look for a debt-to-income ratio under 43%, and at $75K, even a $450,000 mortgage tests that limit. A dual-income household or a move to an inland city with lower home prices opens more realistic paths. See more real-world California paycheck scenarios to understand how different household situations play out on this salary.

What Tax Bracket Is $75K in California?

For federal taxes, the 22% marginal bracket applies to the portion of income above $48,475 (after the standard deduction). For California state taxes, the 9.3% bracket applies to most of a $75K earner’s income, as that bracket starts at $70,607 for single filers in 2026.

How Much Rent Can I Afford on a $75K Salary?

Using the 30% rule, your rent ceiling is approximately $1,875 per month based on gross monthly income of $6,250. This is affordable in inland California cities but below average rent in LA, San Diego, and San Francisco.

Is $75K Enough in Los Angeles?

$75K is workable in Los Angeles with a roommate or shared housing situation. Living solo in LA on $75K means housing alone may consume 35% to 40% of your gross income, leaving limited room for savings. It is livable but not comfortable without careful budget management.

Is $75K Enough in San Francisco?

$75K in San Francisco is genuinely challenging. Average one-bedroom rent exceeds $2,800 per month. That is 45% of your gross monthly income before taxes. Most financial advisors would call that unsustainable. Roommates, subsidized housing, or a shorter-term plan with aggressive savings would be needed to make it work.

How Much Do Benefits Reduce Take-Home Pay?

Typical employer benefit deductions reduce your monthly take-home by $300 to $700 per month depending on the plan. Health insurance is the largest single deduction, followed by retirement contributions and dental or vision premiums.

How Can I Legally Reduce My Taxes?

The most effective legal strategies at $75K in California include:

- Maximize your traditional 401(k) contributions to reduce taxable income

- Contribute to an HSA to save on federal taxes (and healthcare costs)

- Adjust your W-4 to avoid over-withholding

- Use FSA accounts for dependent care or healthcare expenses

- Negotiate total compensation packages that include pre-tax benefits

- Check if you qualify for the California Earned Income Tax Credit (CalEITC) — depending on your exact income and filing status, you may be eligible for a refundable credit that reduces your final tax bill

Final Verdict: Can You Live Comfortably in California on $75K?

Yes. You absolutely can.

The most common fear I hear from people researching this salary is simple: “Will I struggle financially in California on $75K?” The honest answer is that struggle is not inevitable. It is a product of city choice and planning, not the salary itself.

This salary works better in some California cities than others, better with a roommate than alone, and better with a 401(k) than without one. Remote workers who choose Sacramento over San Francisco gain the most.

The taxes are high but not catastrophic. Your effective rate of 24% to 29% is significant. It does not take half your income. The myths about California taxes are usually worse than the reality.

City choice is what matters most. A $75K earner in Sacramento with shared housing and a 5% 401(k) contribution can save $700 to $1,000 per month. That same earner living alone in San Francisco might struggle to save $100. Same salary. Same taxes. Completely different financial life.

Evaluate your total compensation: remote flexibility, benefits quality, equity, and commuter perks. The lifestyle you want and the city you choose will determine far more than the tax rate. Understanding your rights around pay, overtime, and deductions also protects your income — our California labor laws hub covers what every employee should know, and the California Department of Industrial Relations is the official source for wage orders, labor code updates, and employee rights.

California rewards people who plan smart. And $75,000 is a solid foundation to build on.

Build the right budget for the right city. On $75K in California, financial stability is not just possible. It is within reach.

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax figures are estimates based on 2026 IRS and California FTB guidelines for a single W-2 filer using the standard deduction. Your actual take-home pay will vary based on your specific withholding elections, employer benefit deductions, and personal tax situation. Consult a licensed tax professional or CPA for advice tailored to your circumstances.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.