Filling out a W-4 form wrong does not change what you owe in taxes. It only changes when you pay it, through a smaller paycheck now or a bigger bill in April. The 2026 version raised the Child Tax Credit on Step 3 to $2,200 per qualifying child, up from $2,000, a quiet update that directly affects how much parents take home each pay period. The tricky part is that most of the form does not apply to most people, and figuring out which steps actually matter for your situation is where this guide starts. For more on how withholding fits into your overall paycheck, our paycheck basics category covers the fundamentals.

Quick Answer: How to Fill Out a W-4 in 5 Simple Steps

Fill in your name, address, and Social Security number in Step 1. Choose your filing status. Sign Step 5. That is it for most single people with one job. In my experience, this is where most people stop reading and just want the short version.

Every new employee fills one out before their first paycheck. If you never submit one, your employer must withhold at the highest rate, treating you as Single with no adjustments.

Steps 2 through 4 are optional, only needed for a second job, dependents, or side income. The form tells your employer how much federal income tax to pull from each paycheck. Get it right and you avoid a surprise tax bill in April. Most people finish in under 10 minutes.

Takeaway: Only Steps 1 and 5 are required. Everything else depends on your life situation.

Existing employees do not need a new W-4 every year. The one on file stays active until you replace it.

Find Your Situation First

Your situation determines which steps to fill out and which to skip.

I Have One Job and No Dependents

Fill out Step 1, select “Single or Married filing separately,” skip Steps 2 through 4, and sign Step 5.

Your employer withholds at the Single rate, the standard default. You will likely get a small refund or owe a small amount when you file in 2027.

Takeaway: One job, no dependents means you only need to complete Steps 1 and 5.

I Am Married and My Spouse Works

Each spouse completes a separate W-4. Withholding is calculated as if each job is your only income, so not enough tax gets pulled and you end up owing at tax time.

Three fixes exist. Most accurate: the IRS Tax Withholding Estimator at irs.gov/W4App, about 20 minutes, gives you a number for Step 4(c). Quickest: check the box in Step 2(c) if you have exactly two jobs with similar pay.

Takeaway: Always complete Step 2 when both spouses work. Skipping it leads to a tax bill.

I Have Two or More Jobs

Your employer only sees one salary, so without an adjustment, not enough tax gets withheld across all your jobs. The W-4 only covers federal withholding though. California also has its own version of this problem on the state side, which is why pairing this with a guide on how to fill out the California DE 4 form is worth doing at the same time.

Step 2 has three options. Option (a), the IRS estimator, is most accurate. Option (b), the Multiple Jobs Worksheet on page 3, is private but requires math. Option (c), checking a box, works only if you have exactly two jobs with similar pay. Complete Steps 3 through 4(b) on only your highest-paying W-4.

Takeaway: Use the IRS estimator or the Multiple Jobs Worksheet for accurate withholding when juggling two or more jobs.

I Have Children or Dependents

Step 3 reduces your withholding for the Child Tax Credit and other dependent credits, if your income is $200,000 or less ($400,000 married filing jointly).

For each qualifying child under 17, multiply by $2,200 and enter it in line 3(a). For other dependents, multiply by $500 for line 3(b). Add both for the total on line 3.

Only one spouse should claim dependents. Claiming on both forms causes under-withholding.

Takeaway: Claim dependents in Step 3 to boost your take-home pay. Only one spouse should do this.

I Have Freelance, Gig, or Investment Income

Side income has no automatic withholding. Step 4(a) fixes this: enter your estimated annual total from gigs, freelance work, dividends, or retirement income, and your employer pulls extra tax from your W-2 paycheck. If you are weighing whether to take a 1099 gig at all, our 1099 vs W2 take-home pay calculator shows exactly how the numbers compare in California.

You can skip Step 4(a) and file Form 1040-ES quarterly instead, but extra withholding is easier and prevents penalties. Step 4(c) also lets you add a flat extra amount per paycheck. If you are deciding whether your side work counts as employee or contractor income, our worker classification category has more on how California draws that line.

Takeaway: Use Step 4(a) for side income so you do not get hit with a surprise bill or underpayment penalty.

What the W-4 Form Actually Does

How Withholding Works

Each paycheck, your employer holds back tax and sends it to the IRS, like paying taxes in installments instead of one April payment.

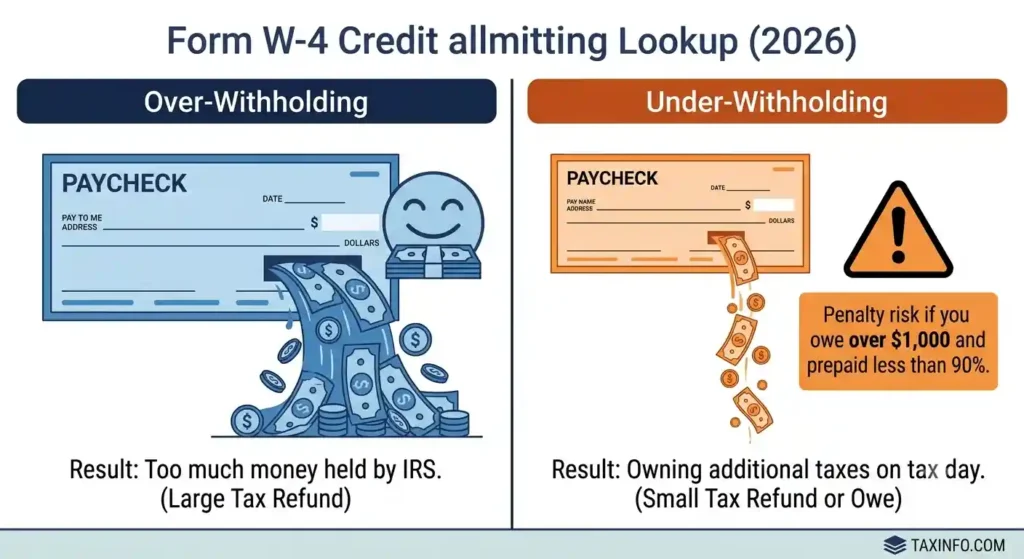

Your employer plugs your Form W-4 entries into the IRS withholding tables to calculate the exact amount per paycheck. Too little withheld means you owe later. Too much means a refund, which is really an interest-free loan to the IRS. What I have found is that most people are better off adjusting withholding to keep more money each month.

Takeaway: Withholding is prepaid tax. Getting it right means no bill and no oversized refund.

What Changed From the Old W-4

Before 2020, the form used “allowances,” claimed as 0, 1, 2, or more. That system is gone. The IRS redesigned the form in 2020, and 2026 keeps the same five-step structure.

Now you enter actual dollar amounts instead. If someone tells you to “claim single and zero,” that advice no longer applies. There are no zeros on the current form.

Takeaway: The old allowance system is gone. Ignore any advice about claiming “0” or “1” allowances.

Before You Fill Out the Form

Information to Gather

Gather your Social Security number, address, and expected 2026 filing status. If your spouse works or you have a second job, grab recent pay stubs. Know your dependent count.

Your most recent tax return helps too. Did you owe money or get a refund? That tells you whether your withholding was too low or too high.

Takeaway: Gather your SSN, pay stubs, last tax return, and dependent info before you start.

Situations Requiring Extra Planning

Multiple jobs, a working spouse, side income, or itemized deductions affect withholding in ways the basic form cannot catch automatically. Use the IRS Tax Withholding Estimator at irs.gov/W4App first. About 20 minutes, and it saves you from a nasty April surprise.

Step-by-Step Instructions for Every Line

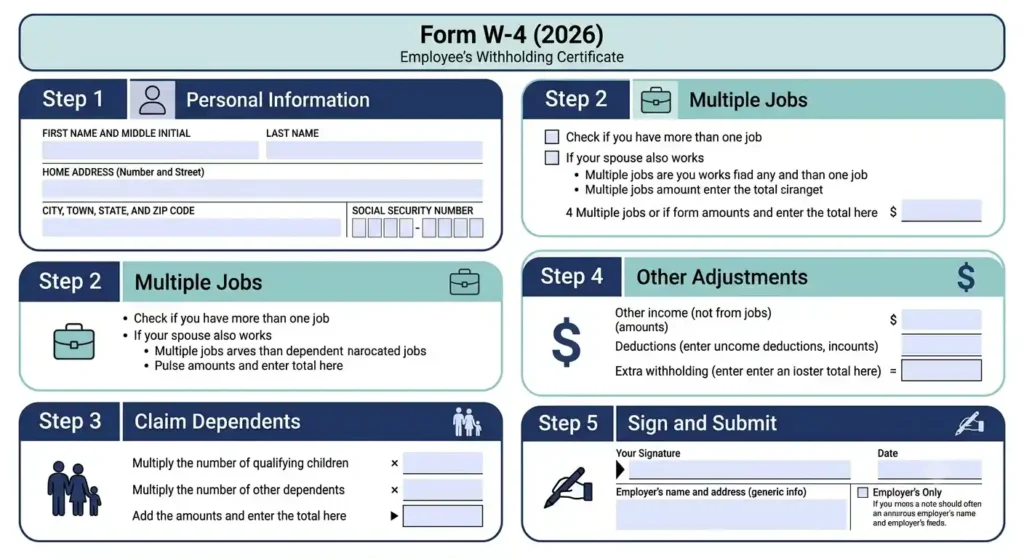

Step 1: Personal Information

Name, Address, and SSN

Line 1(a) is your name. Line 1(b) is your Social Security number. Make sure your name matches your Social Security card exactly, or call the Social Security Administration at 800-772-1213 to fix it. A mismatch can affect your future Social Security benefits.

Use your home address, not your work address.

Choosing Your Filing Status

Line 1(c) has three choices.

“Single or Married filing separately” applies to unmarried filers and married people filing separately. Least favorable brackets, more withholding. It is also the default if you pick nothing.

“Married filing jointly or Qualifying surviving spouse” applies if you file a joint return. Wider brackets and a larger standard deduction ($32,200 in 2026), so less withholding.

“Head of household” is for unmarried filers paying more than half their home costs with a qualifying person living there. Do not check it if you are married.

Pick the wrong status and every other calculation is off.

Takeaway: Filing status determines your standard deduction and tax brackets. Get this right first.

Step 2: Multiple Jobs or Working Spouse

Option 1: IRS Tax Withholding Estimator

Option (a) sends you to irs.gov/W4App, the most accurate and private choice since nothing about your outside income appears on the W-4 itself. It gives you a dollar amount for Step 4(c). Works especially well with self-employment income.

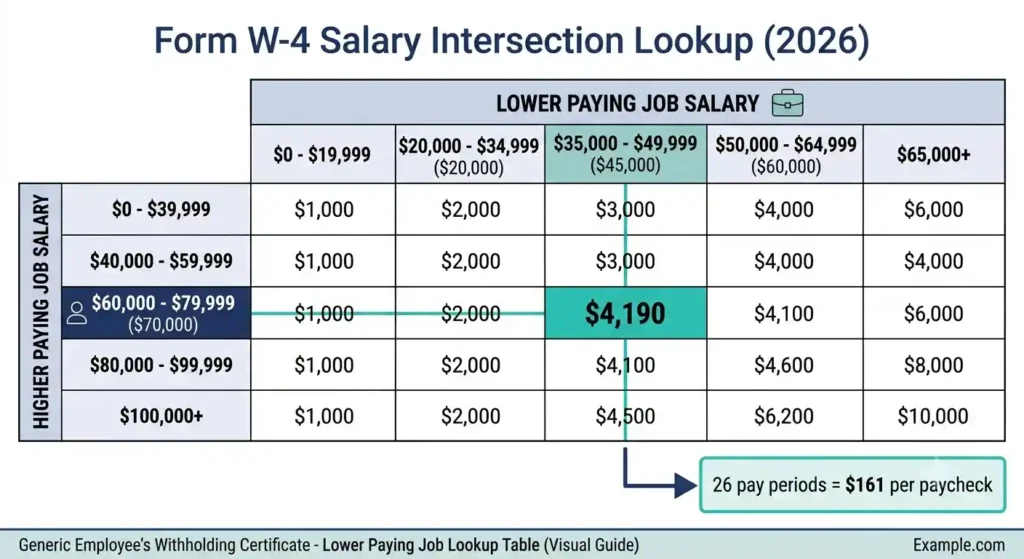

Option 2: Multiple Jobs Worksheet

Option (b) uses the multiple jobs worksheet on page 3. Find your two salaries’ intersection on the table (separate tables exist for Married Filing Jointly, Single/MFS, and Head of Household), divide the result by your pay periods, and enter it in Step 4(c). Less accurate but keeps income details off the form. Download the full form from IRS.gov.

Option 3: Check Box Method

Option (c) is a checkbox for exactly two jobs with similar pay, checked on both W-4s. Your employer halves the standard deduction and brackets for each job. Easiest but least accurate. Over-withholds if one job pays much more.

Takeaway: Use the IRS estimator for accuracy. Use the checkbox only if both jobs pay about the same.

Step 3: Claim Dependents

Qualifying Children

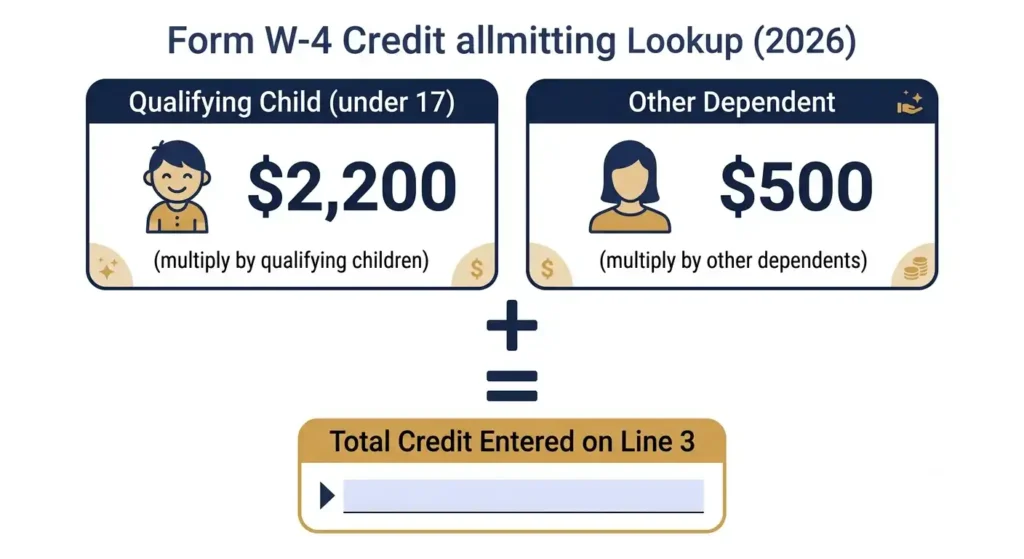

A qualifying child is under 17 as of December 31, your dependent, lives with you more than half the year, and has a valid SSN. The 2026 Child Tax Credit is $2,200 per qualifying child, up from $2,000 in recent years. Multiply your count by $2,200 for line 3(a).

Example: two children under 17 equals $4,400 on line 3(a), reducing your annual withholding by that amount.

Other Dependents

Other dependents include older children, qualifying relatives, or others you support. The IRS calls this the Credit for Other Dependents, worth $500 each, entered on line 3(b). Add 3(a) and 3(b) for the line 3 total.

You can also add other credits, like the foreign tax credit, here. Skip Step 3 entirely if your income exceeds $200,000 single or $400,000 married filing jointly; the credits phase out.

Takeaway: Step 3 increases your take-home pay now by accounting for credits your employer would otherwise not know about.

Step 4: Other Adjustments

Other Income

Line 4(a) covers income without automatic withholding: interest, dividends, retirement distributions, freelance payments on Form 1099-NEC, gig earnings on Form 1099-K, and rental income. Enter your estimated annual total and your employer withholds extra to cover it. Easier than quarterly estimated taxes and protects against underpayment penalties. Do not include W-2 wages from another job here; that goes in Step 2.

Deductions

Line 4(b) is only for deductions beyond the standard. Skip it if you take the standard deduction: $16,100 single, $24,150 head of household, $32,200 married filing jointly in 2026. For a deeper breakdown of how the California standard deduction compares to the federal one, that guide covers the state side of this calculation.

If you itemize, use the deductions worksheet on page 4. The 2026 version is expanded with lines for qualified tips (up to $25,000, income under $150,000), qualified overtime compensation (up to $12,500), and qualified passenger vehicle loan interest (up to $10,000, income under $100,000), all new under the One Big Beautiful Bill Act. Seniors 65 or older can claim an extra $6,000 per eligible spouse if household income is under $75,000 ($150,000 married). Enter the line 15 result in line 4(b).

Extra Withholding

Line 4(c) adds a flat extra amount per paycheck. Use it after the IRS estimator or Multiple Jobs Worksheet, or just as a cushion. Even $25 to $50 extra per check can eliminate a tax bill.

Takeaway: Use 4(a) for side income, 4(b) if you itemize, and 4(c) for a simple safety cushion.

Step 5: Sign and Submit

Sign and date exactly as your name appears at the top. The form is not valid without your signature.

Hand it to HR or payroll, not the IRS. The change typically takes effect within one or two payroll cycles.

Takeaway: An unsigned W-4 is invalid. Sign it and give it to your employer, not the IRS.

Completed W-4 Examples

Single Employee With One Job

Maria, single, earns $55,000 in California, no dependents. She fills in Step 1, checks “Single or Married filing separately,” skips Steps 2 through 4, and signs Step 5. She will likely get a small refund.

Married With Two Jobs

David earns $70,000, his wife Lin earns $45,000, filing jointly. Both complete Step 2. David uses the Multiple Jobs Worksheet, finds the $70,000/$45,000 intersection on the MFJ table for $4,190, divides by 26 biweekly pay periods for $161, and enters that in Step 4(c). Lin’s W-4 has only Step 1 and 5 filled in. David also completes Step 3 for their one child under 17, entering $2,200.

Parent Claiming Two Children

Jennifer, single, earns $80,000, has two kids under 17, under the $200,000 limit. She multiplies 2 by $2,200 for $4,400 on line 3(a). No other dependents, so 3(b) stays blank. This adds about $169 to each biweekly paycheck.

Employee With Side Hustle Income

Carlos earns $60,000 at his main job plus $12,000 freelancing, none withheld. He enters $12,000 in Step 4(a), and his employer withholds extra to cover it, avoiding quarterly payments and underpayment penalties.

First Job for a Teenager

Ava, 16, starts a summer retail job at $14 an hour. She fills out Step 1, checks Single, skips the rest. If she expects to earn under the standard deduction for the year, she may qualify to check the exemption box below Step 4(c) for zero federal withholding.

Part-Time and Seasonal Workers

Part-time and seasonal workers fill out the same W-4 as anyone else. There is no separate version. Fill in Step 1, skip what does not apply, sign Step 5. Low seasonal income often means minimal withholding makes sense. See our guide on part-time vs full-time paycheck differences in California for more on how hours affect your take-home pay.

Special Situations

Starting Your First Job

Fill out Step 1, check Single, skip Steps 2 through 4, sign Step 5. You may get a small refund. Update later as your situation changes.

Changing Jobs

New job means a fresh W-4, nothing transfers from the old one. A job gap may mean fewer paychecks had withholding, so adjust if needed, especially mid-year.

A second job partway through the year is just a multiple-job situation. Update your first employer’s W-4 with Step 2 and rerun the IRS estimator with both salaries. Starting in October instead of January leaves fewer pay periods to catch up.

Getting Married

Update your filing status to “Married filing jointly” as soon as possible. Complete Step 2 if your spouse works too. Marriage changes your bracket and standard deduction, so old withholding is likely off.

Having a Baby

Once your child has an SSN, add them to Step 3: multiply by $2,200. Submit as soon as you have the SSN, usually within a few weeks of birth. The same applies to an adopted child once the adoption is finalized. New parents managing leave at the same time may also want to check our guide on California maternity leave pay for how SDI and PFL benefits factor into the picture.

Buying a home does not change your W-4 directly, but mortgage interest and property taxes can push itemized deductions above the standard. If so, run the deductions worksheet for Step 4(b).

Divorce

Update your filing status immediately, likely to Single or Head of Household. Review dependent claims, coordinating with your former spouse if children split between households.

Receiving a Raise or Bonus

A raise can push you into a higher bracket; rerun the IRS estimator. Bonuses are usually withheld at a flat 22% federal rate (37% on amounts over $1 million), which may not cover what you actually owe. Our California bonus tax rate guide breaks down exactly how much of a bonus check actually lands in your account. Add extra withholding via Step 4(c) if needed.

Losing a Dependent

If a child turns 17 or no longer qualifies, remove them from Step 3 on your next update, or you will keep claiming a credit you no longer qualify for, leading to under-withholding.

Starting Retirement Income

A pension or retirement distribution while still working is generally not subject to W-4 withholding unless you request it via Form W-4P. For your job income, account for the extra retirement income using Step 4(a).

W-4 Myths and Misconceptions

Bigger Refund Means Better Taxes

A large refund means you overpaid all year, an interest-free loan to the IRS. That money could have earned 4% to 5% in savings or paid down debt. In my experience, a $3,000 refund means a $250 monthly pay cut you did not need.

Filling Out a W-4 Changes Your Tax Bill

Your W-4 only changes when you pay, not what you owe. Owe $8,000 and you owe $8,000, whether withheld in full or in pieces.

Everyone Should Complete Every Section

Most people only need Steps 1 and 5. Steps 2 through 4 are optional and only apply in specific situations. Filling them in unnecessarily causes errors. The form itself says: “Complete Steps 2 through 4 ONLY if they apply to you.”

Common W-4 Mistakes That Cost Money

Over-Withholding Mistakes

Usually happens filing Single while married, or skipping Step 3 dependent credits. Fix: submit an updated W-4 with the correct status and credits. Your next paycheck reflects it. If your paycheck already looks smaller than expected for other reasons, our guide on why your California paycheck is so low walks through the most common causes.

Under-Withholding Mistakes

Common triggers: an unaccounted working spouse, a second job pushing income into a higher bracket, or unwithheld side income. A penalty can hit if you owe over $1,000 and prepaid less than 90% through withholding. Add a Step 4(c) cushion if unsure.

Outdated Advice to Ignore

Ignore “claim zero allowances” or “claim single even if married for more withholding.” Those strategies are for the pre-2020 form. The current form has no allowances at all.

Other Costly Slip-Ups

Married couples sometimes both claim the same children on separate W-4s, doubling the credit. Some fill in every box even when nothing applies, throwing off the math.

W-4 Comparisons

W-4 vs W-2

Not interchangeable. The W-4 is filled out when you start a job and tells your employer how much to withhold. The W-2, sent every January, reports what you earned and what was withheld. You give the W-4 to your employer; your employer gives you the W-2.

W-4 vs W-9

The W-4 is for employees, the Form W-9 for independent contractors and freelancers. Employees have automatic withholding; contractors handle their own self-employment and income taxes, typically receiving a Form 1099-NEC at year end with no withholding attached. For a full breakdown of the tax tradeoffs, see our 1099 vs W2 tax guide for California workers.

W-4 vs Estimated Tax Payments

Both get money to the IRS in advance. The W-4 does it automatically through payroll. Estimated taxes are quarterly payments via Form 1040-ES, due in April, June, September, and January. You can use both together, common for a day job plus side business.

W-4 vs Tax Return

The W-4 sets withholding before the year starts; it is a prediction. Your tax return, Form 1040, is the final accounting filed afterward. The gap between the two becomes your refund or balance due.

Federal W-4 vs State Withholding Form

The W-4 only controls federal withholding. Most states with income tax need a separate form, like California’s DE 4 form. Skip the state form and your state withholding may default to something that does not match your situation. Pairing your federal W-4 with an accurate look at the California tax brackets for 2026 gives you the full picture of what is actually coming out of your check.

After You Submit Your W-4

When Changes Appear

The change usually shows within one or two pay cycles, not instantly. A Monday submission with a Friday payday already in process shows up on the next check. Check your pay stub to confirm.

How to Check Your Withholding

Find “Federal Income Tax” on your pay stub, multiply by your paychecks per year for a projected annual total. If you are not sure how to read the rest of your stub, our guide on how to read a California pay stub breaks down every line item. Compare your projected withholding to what you expect to owe. Adjust your W-4 if the numbers are far apart.

Signs you need an update: consistently owing a large balance, a growing refund every year, or a household income change with no paycheck adjustment. To estimate the impact of a change, divide the new Step 3 or 4 dollar amount by your remaining pay periods.

When to Submit a New W-4

Update after marriage, divorce, a new or adopted child, a new job, your spouse starting or leaving work, a big raise, or significant freelance income. No limit on how often you can submit. The IRS recommends an annual review too.

Frequently Asked Questions

Do I Have to Fill Out Every Section?

No. Only Steps 1 and 5 are required. Steps 2 through 4 apply only with multiple jobs, a working spouse, dependents, or other income and deductions.

Can I Change My W-4 Anytime?

Yes, as often as you want, with no waiting period or penalty. The exception is exempt status, which expires February 15 each year and must be re-filed.

What Happens if I Leave Step 2 Blank?

Fine with one job and a non-working spouse. With multiple jobs or a working spouse, each employer withholds based on your salary alone, almost always causing under-withholding.

What if I Filled It Out Incorrectly?

Submit a new W-4 with correct information, no penalty for the mistake. If you under-withheld mid-year, use Step 4(c) to close the gap for the rest of the year.

Will Changing My W-4 Affect My Refund?

Yes. More withholding means a bigger refund (or smaller balance due); less means more take-home pay now. Your actual tax liability never changes, only the timing.

Do I Need a New W-4 Every Year?

Not unless something changed. It stays in effect until you submit a new one or leave the job. The exception is exempt status, which expires February 15 and must be renewed.

How Does Claiming Exempt From Withholding Work?

If you owed no federal tax last year and expect none this year, check the exemption box below Step 4(c) for zero federal withholding. The 2026 form replaced the old write-in “Exempt” text with this checkbox. Social Security and Medicare are still withheld regardless.

Do Bonuses and Overtime Get Withheld Differently?

Bonuses and supplemental wages are usually withheld at a flat 22% federal rate (37% over $1 million in a year), separate from your regular paycheck. Overtime is taxed at your normal rate, simply added to your regular pay.

What if I Work Remotely or for Multiple Employers?

Remote workers fill out the same federal W-4. The bigger issue is usually state withholding, since some states tax based on where you physically work. Multiple employers at once means treating it like a multiple-jobs situation: complete Step 2.

Can My Employer Reject My W-4?

Employers cannot tell you how to fill in your filing status or dependents, since that is personal. Payroll can reject an incomplete, unsigned, or illegible form and ask for a corrected version.

Final W-4 Checklist Before You Submit

- Your name matches your Social Security card exactly

- Correct Social Security number entered

- Correct filing status checked

- Step 2 completed only if you have multiple jobs or a working spouse

- Step 3 filled in only if income is $200,000 or less ($400,000 married filing jointly) with qualifying dependents

- Step 4 entries match your actual income, deductions, or extra withholding needs

- Step 5 signed and dated

- Form goes to your employer, not the IRS

A correctly filled-out W-4 means no surprises at tax time and more control over your paycheck. Once your withholding is set, run the numbers through our California paycheck calculator to see exactly what your take-home pay will look like.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.