California taxes capital gains the same way it taxes a paycheck. There’s no separate capital gains rate, gains get added to ordinary income and taxed under the state’s brackets, from 1% up to 13.3%. Stack that onto the federal long-term rate and the NIIT, and a top earner can lose close to 37.1% of a single sale. The lower bracket thresholds shift with inflation each year, so check the FTB’s published schedule before assuming your exact cutoff.

Quick Answer: How California Taxes Capital Gains

This guide is for anyone in California about to sell stock, a rental house, crypto, or a business. All of it lands on your return the same way your paycheck does, taxed by the same brackets, no matter how long you held it.

California Capital Gains Tax at a Glance

California taxes capital gains as ordinary income, 1% to 13.3% based on total taxable income. The federal government taxes long-term gains at 0%, 15%, or 20%, plus a possible 3.8% surtax for high earners. Combined, a top earner selling a long-term asset in 2026 can owe close to 37.1%. Short-term sellers in the top bracket can lose more than half their profit to the IRS and the Franchise Tax Board.

| Quick Fact | 2026 Number |

|---|---|

| California capital gains tax rate | 1% to 13.3% |

| Federal long-term capital gains rate | 0%, 15%, or 20% |

| Federal short-term rate | Same as ordinary income, up to 37% |

| Net Investment Income Tax (NIIT) | 3.8% over $200,000 (single) / $250,000 (MFJ) |

| Highest possible combined rate (long-term) | About 37.1% |

| Highest possible combined rate (short-term) | Over 50% |

Fast Answer by Asset Type

Stocks are taxed like wages in California, regardless of holding period. Real estate works the same way, but Section 121’s home sale exclusion or a 1031 exchange can reduce the bill. Crypto is taxed like any other property sale, and the FTB gets the same exchange data the IRS does. Business sales usually create the biggest gains and the biggest tax bills.

Federal vs California Capital Gains Tax

Side-by-Side Comparison Table

| Federal | California | |

|---|---|---|

| Long-term rate | 0%, 15%, or 20% | Same as ordinary income (1% to 13.3%) |

| Short-term rate | Ordinary income rates, up to 37% | Same as ordinary income (1% to 13.3%) |

| Holding period matters? | Yes | No |

| Extra surtax | 3.8% NIIT over certain income | None |

| Top combined rate (long-term) | — | About 37.1% |

Why California Is Different

California gives no discount for long-term holdings. The Franchise Tax Board adds your gain to your total income and runs it through the same nine brackets that tax your salary under California’s payroll tax system, so one big sale, like a $300,000 stock cash-out, can push you into a higher bracket for the year. This rule traces back to the California Revenue and Taxation Code, enforced by the California Franchise Tax Board with no carve-out for investment income. Most people find this out the hard way, after the sale already closed.

California Capital Gains Tax Rates Explained

Does California Have a Capital Gains Tax Rate?

No separate one. California taxes capital gains as ordinary income under its progressive brackets, with no break for holding period. A capital gain only becomes taxable once you sell or exchange the asset, the transaction underlying Internal Revenue Code Section 1221’s definition of a capital asset. An unrealized gain, where the asset rose in value but you still own it, isn’t taxed by California or the IRS until that sale happens. It works a lot like a bonus, which also settles at your regular bracket despite a different upfront withholding rate, see our guide to California’s bonus tax rate for that comparison.

Current California Tax Brackets

Single Filers

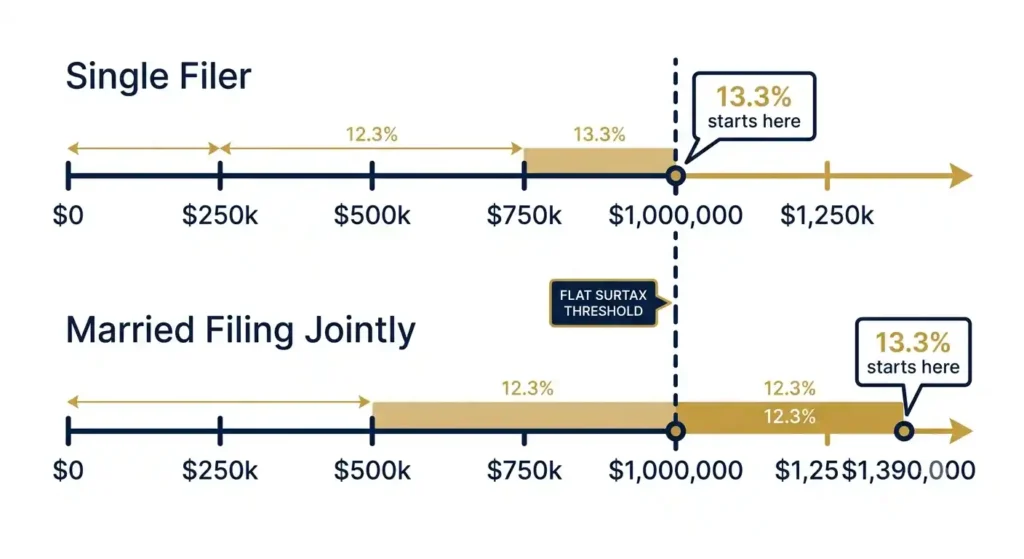

California runs nine brackets for single filers in 2026, from 1% on the first roughly $11,000 of taxable income to 13.3% above $1,000,000. The FTB adjusts the lower thresholds for inflation yearly, so check our full breakdown of California’s 2026 tax brackets for the exact current cutoff. The 13.3% top rate includes the extra 1% Mental Health Services Tax above $1,000,000. At $200,000 taxable income, you pay each lower rate on its slice of income, not 9.3% on the whole amount.

Married Filing Jointly

The regular 1% to 12.3% brackets roughly double in width for joint filers. The extra 1% surtax above $1,000,000 does not double, it still starts at $1,000,000 combined taxable income, same as for single filers. So the full 13.3% combined rate generally starts closer to $1,390,000 for joint filers, once the doubled 12.3% bracket overlaps the flat $1,000,000 surtax line.

Head of Household

Head of household brackets sit between single and married filing jointly. You’ll generally have more room before hitting higher brackets than a single filer with the same income, so confirm your filing status before estimating your bill.

How to Calculate Your California Capital Gains Tax

Formula

Selling price minus adjusted basis (what you paid plus improvements, minus depreciation claimed) equals your capital gain. Add that gain to your other taxable income, then apply California’s brackets to the total. Your California standard deduction reduces that total before the brackets apply, and running the combined number through our California paycheck calculator shows the bracket impact instantly.

What Information You’ll Need

You need your purchase price, improvement records, selling costs (commissions, closing fees), and filing status, gathered before you sell. Missing improvement receipts is a common reason people overpay, since every improvement dollar lowers your taxable gain.

Factors That Affect How Much You’ll Pay

Filing Status

Single, married filing jointly, and head of household use different bracket widths. The same $100,000 gain can land in a 9.3% bracket for one filer and 6% for another, based on filing status and total income.

Taxable Income

Your gain stacks on top of existing income, so your marginal bracket, not your average rate, sets the cost. Plug your salary into our annual salary calculator first to see exactly where that stacking begins. A $50,000 earner adding a $200,000 gain pays a much higher rate on that gain than someone barely crossing into the next bracket.

Holding Period

Holding an asset over a year unlocks the lower federal long-term rates (0%, 15%, or 20%). California ignores holding period entirely, so waiting a year does nothing for your state tax bill.

Cost Basis

Basis starts at purchase price, grows with improvements, shrinks with depreciation claimed. Selling expenses like commissions and title fees reduce your gain too. Getting this number right is the biggest lever you control before a sale.

Real Examples of California Capital Gains Tax

Selling Stocks

Stock bought for $20,000, sold for $70,000 after two years: a $50,000 long-term gain taxed federally at 15% (about $7,500), plus California at roughly 9.3% to 13.3% ($4,650 to $6,650 more), depending on total income. A $300,000 gain can hit California’s top bracket and the federal NIIT at once, pushing the combined tax close to a third of the profit. For more real-number breakdowns like this, see our other paycheck scenarios.

Selling Cryptocurrency

Bitcoin bought at $20,000, sold at $60,000: the $40,000 gain is taxed like a stock sale, no special crypto treatment. Coinbase, Kraken, and other exchanges report transaction data to both the IRS and the FTB.

Selling a Primary Residence

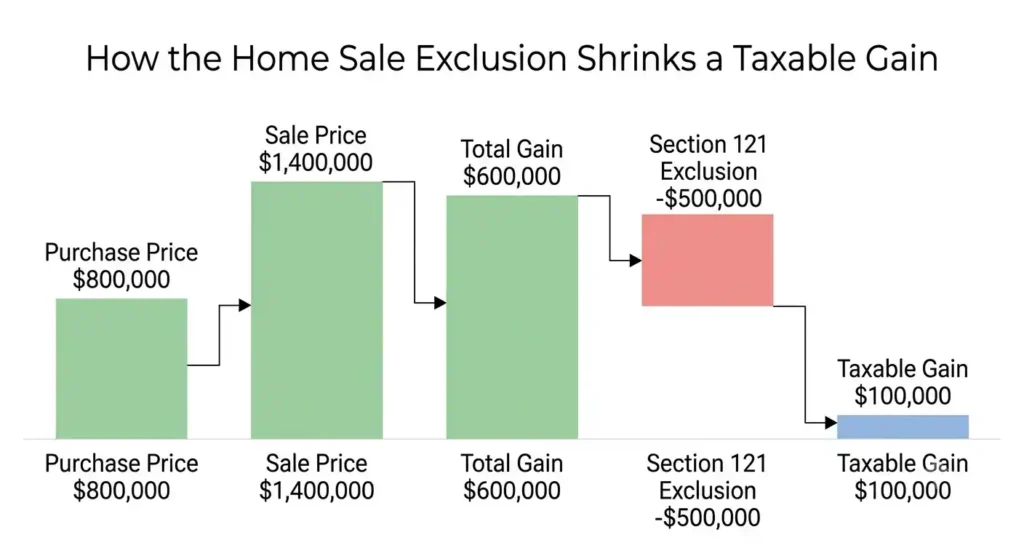

Internal Revenue Code Section 121 excludes up to $250,000 of gain (single) or $500,000 (married filing jointly), if you lived in the home at least two of the last five years. The IRS lays this out in detail in Topic 701 on the sale of a home. Example: a Los Angeles home bought in 2019 for $800,000, sold in 2026 for $1.4 million, a $600,000 gain. After the $500,000 exclusion, only $100,000 is taxable.

Selling Rental Property

Rental sales combine capital gain with depreciation recapture, both taxed as ordinary income in California. Example: a Sacramento duplex bought in 2018 for $400,000, sold in 2026 for $650,000, a $250,000 gain, taxed at your marginal rate, easily $20,000 or more to California alone at 9.3% or higher, before federal tax. That depreciation recapture falls under Internal Revenue Code Section 1250, and it’s a big reason an investment property sale often owes more tax than selling a primary residence of similar value, since a residence never had depreciation lowering its basis, though the exact gap depends on gain size, bracket, and exclusion used.

Selling a Business

A $3 million business sale can trigger six figures in combined state and federal tax, since California gives no special discount on business gains. Business assets like equipment or real estate used in the company often fall under Internal Revenue Code Section 1231, blending capital gain treatment with ordinary income recapture depending on what’s sold. If you’re still drawing income from the business right up to closing, check how California’s self-employment tax rate applies to that final stretch too.

Selling Inherited Property

Inherited property gets a stepped-up basis to fair market value on the date the previous owner died. Sell soon after inheriting and you’ll owe little to nothing. Appreciation after that point becomes taxable on sale.

Special Situations That Can Change Your Tax Bill

Moving Out of California

California taxes gains realized while you were a resident. Part-year residents owe tax only on the gain tied to their California residency period. If you’ve already left, you’re a nonresident, and you’ll typically file Form 540NR with Schedule CA (540NR) to report California-source income, such as gain from selling California real estate after moving away. This often creates a multi-state filing situation too, since your new home state may also tax the gain, so waiting to move usually adds a second state’s paperwork rather than erasing the bill.

RSUs and Employee Stock

RSU value at vesting is compensation, taxed as ordinary income. Gain after vesting is a separate capital gain under California’s normal rules. ESPP shares split the same way: the purchase discount is ordinary income, further gain is a separate capital gain. A big vesting event is also a good time to revisit your DE4 withholding so your paycheck doesn’t fall short later.

Mutual Funds and ETFs

Funds can distribute capital gains even if you never sold a share, since the fund sold holdings internally; these distributions are taxable the year received. Reinvesting them isn’t tax-free, it just buys more shares with after-tax money. Dividends are taxed as income when received; a capital gain only arises when you sell shares for a profit.

Gifts and Inherited Assets

Gifted assets carry the giver’s original basis; inherited assets get a stepped-up basis at death. Example: a parent buys stock for $5,000, gifts it at $30,000 value, your basis stays $5,000, so selling it for $40,000 makes your taxable gain $35,000, not $10,000.

Net Investment Income Tax

The 3.8% NIIT applies federally above $200,000 (single) or $250,000 (MFJ) modified AGI. California has no equivalent tax, but the NIIT still stacks on top of your federal bill. High earners should also check the Alternative Minimum Tax, since add-back deductions can raise the real federal bill. California runs its own separate AMT too, on Schedule P (540), so a large gain can trigger an add-back on both returns.

Common Mistakes and Myths

Myth: California Has Lower Long-Term Capital Gains Rates

False. California taxes short-term and long-term gains identically; the lower long-term rates exist only at the federal level.

Myth: Reinvesting Eliminates Tax

A sale is taxable the moment it closes, regardless of what you do with the proceeds. The exceptions, like a properly structured 1031 exchange, require rules followed before the sale.

Myth: Only Cash Withdrawals Are Taxable

Selling inside a taxable brokerage account triggers tax at execution, even if you never withdraw the cash.

Mistakes That Cost Thousands

Wrong cost basis, forgotten improvement costs, ignored selling expenses, and missed estimated payments are the priciest errors. Poor timing, like stacking a big gain onto a high-income year, can push you into an avoidable bracket. A California capital gains tax calculator can give a different number than your CPA, since most use rough averages instead of your actual basis, filing status, and bracket stacking, so treat any California tax calculator as a starting estimate.

Ways to Reduce California Capital Gains Tax Legally

Tax-Loss Harvesting

Losses offset gains dollar for dollar; up to $3,000 of leftover loss can offset ordinary income yearly, with the rest carried forward indefinitely. Example: a $120,000 gain plus a $40,000 loss drops your taxable gain to $80,000. The offset only applies to gains and losses realized in the same tax year. California generally follows federal rules for loss carryforwards, so your federal carryforward applies to your state filing too.

Home Sale Exclusion

The $250,000 (single) or $500,000 (married) exclusion under Section 121 requires owning and living in the home two of the last five years. Partial exclusions exist for certain job, health, or unforeseen-circumstance moves even without the full two years. This isn’t a blanket exemption: rental properties, vacation homes, and any gain above the limit on a primary residence remain fully taxable.

Timing Your Sale

Selling this year versus next can shift a gain into a lower-income year. Spreading a sale across two tax years can keep more of it in lower brackets. Some people wait to realize gains until after retirement, once work income drops and so does their bracket.

Installment Sales

Spreading a gain over several years via an installment sale can keep you out of the top bracket. Works best for real estate or business sales where the buyer pays over time, not for a quick stock sale.

Charitable Giving Strategies

Donating appreciated stock or property directly to a qualified charity avoids the capital gains tax entirely while still earning a deduction at fair market value, better than selling first and donating cash.

California Capital Gains Tax Comparison Tables

California vs Federal Rates

| Income Level | California Rate | Federal Long-Term Rate | Combined Estimate |

|---|---|---|---|

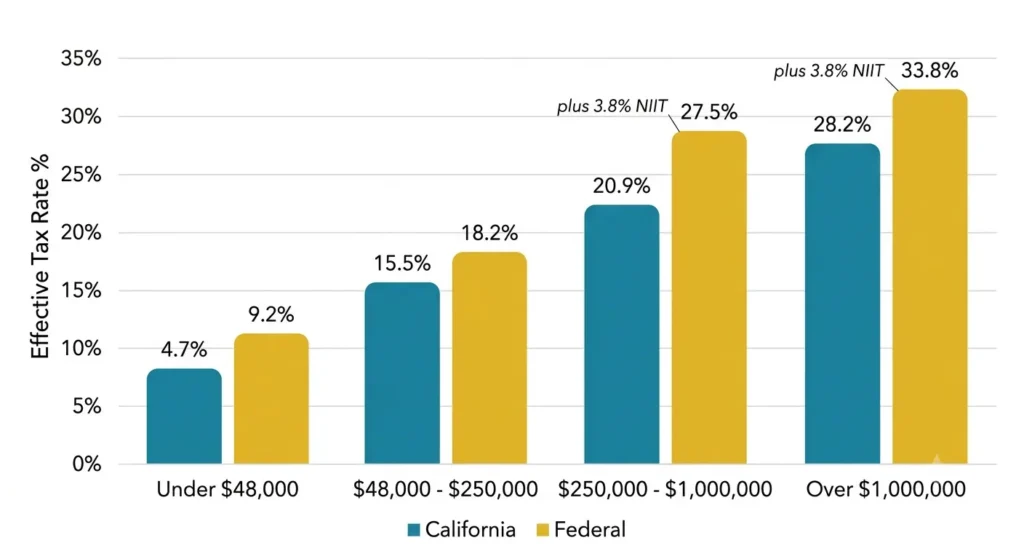

| Under $48,000 (single) | 1% to 6% | 0% | 1% to 6% |

| $48,000 to $250,000 | 6% to 9.3% (9.3% starts near $68,000) | 15% | 21% to 24.3% |

| $250,000 to $1,000,000 | 9.3% to 12.3% | 15% to 20% | 24.3% to 32.3% |

| Over $1,000,000 | 13.3% | 20% + 3.8% NIIT | About 37.1% |

Asset Type Comparison

| Asset | Special Rule | Holding Period Matters Federally? |

|---|---|---|

| Stocks | None | Yes |

| Real estate | Section 121 exclusion, 1031 exchange | Yes |

| Crypto | Treated as property | Yes |

| Business | No discount | Yes |

| Collectibles | Federal cap of 28% | Yes |

Estimated Tax by Income Level

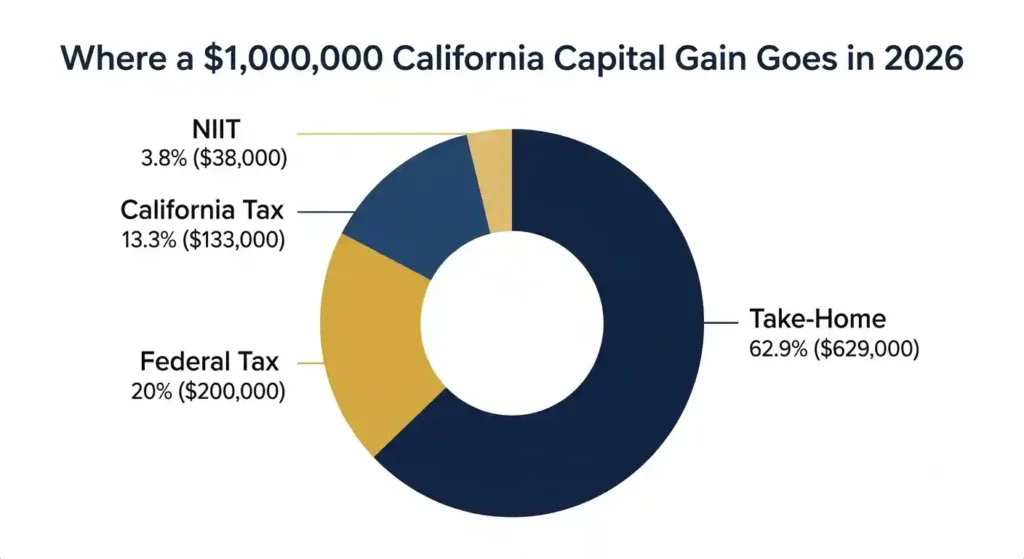

A $10,000 gain at low income might owe close to nothing federally and 1% to 2% to California. A $75,000 gain at middle income lands around 24% combined, comparable to the bracket pressure a $75,000 W-2 earner already feels on a regular paycheck. Above $1 million, the full 37.1% combined ceiling applies on long-term gains, more on short-term. Example: a $1,000,000 long-term business sale gain owes roughly $133,000 to California at 13.3%, about $200,000 federally at 20%, and $38,000 in NIIT, a total near $371,000.

Reporting Capital Gains on Your California Tax Return

Federal Forms

The Internal Revenue Service requires Form 8949 to list each sale’s dates, proceeds, and basis. IRS Schedule D summarizes everything into your total federal gain or loss. Keep brokerage statements and closing documents in case of an IRS request.

California Forms

California Schedule D (540), also called FTB Schedule D (540), is only needed when your California gain differs from your federal gain. Schedule CA (540) adjusts your federal figures to California’s rules, and both feed into Form 540, the main California return. Filing both correctly avoids a mismatch that can trigger an FTB notice. Once everything’s filed, you can track your California tax refund status directly with the FTB.

Recordkeeping Checklist

Keep purchase documents, improvement receipts, brokerage statements, and closing statements. Without them, the IRS and FTB assume a basis of zero. After filing, both agencies can cross-check your reported gain against the 1099-B your broker or title company sent, so matching records make any follow-up quick to resolve. If part of your gain started as RSU or ESPP income, your numbers should also match what’s already on your pay stub.

Frequently Asked Questions

Does California tax long-term capital gains differently?

No. California taxes long-term and short-term gains identically, as ordinary income up to 13.3%. Only the federal government gives long-term gains a lower rate.

How much tax will I pay if I sell stock in California?

Depends on income and holding period. A $50,000 long-term gain might cost $7,500 federally plus $4,650 to $6,650 in California, depending on bracket.

Is selling a house taxable in California?

Yes, unless covered by the Section 121 exclusion of up to $250,000 (single) or $500,000 (married). Gain above that is fully taxable federally and at the state level.

Can I avoid California capital gains tax by moving?

Not easily. California taxes gains realized while you were a resident, based on the timing of your move relative to the sale’s closing date.

Does California tax cryptocurrency gains?

Yes, like stock or property gains. Exchanges report transaction data to the IRS and the FTB, so unreported crypto gains carry real audit risk.

How do capital losses reduce my taxes?

Losses offset gains dollar for dollar. Extra loss beyond gains can cut up to $3,000 of ordinary income yearly, with unlimited carryforward.

Do I have to make estimated tax payments?

If you expect to owe a significant amount, yes, both the IRS and California generally require quarterly estimated payments. California’s safe harbor rules generally protect you if you pay at least 90% of this year’s tax or 100% to 110% of last year’s tax, depending on income. If your California AGI hits $1,000,000 or more ($500,000 if married filing separately), the prior-year safe harbor disappears, and you must pay 90% of the current year’s tax instead, which catches many people right after a big asset sale.

What’s the difference between marginal and effective tax rates?

Marginal rate is what you pay on your last dollar of income, your top bracket. Effective rate is your average rate across all income, always lower than marginal.

Key Takeaways

Before You Sell an Asset

Estimate your combined federal and California tax before signing anything. Review your cost basis and gather receipts for improvements and selling costs. Check eligibility for the home sale exclusion, a 1031 exchange, or tax-loss harvesting. Consider whether spreading the sale across two tax years keeps you out of a higher bracket.

Next Steps

Estimate your liability using actual numbers, not guesses. Gather records now. Review which federal and California forms apply. Talk to a tax professional before closing if the gain is large enough to shift your bracket. A little prep now saves a much bigger surprise at tax time.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.