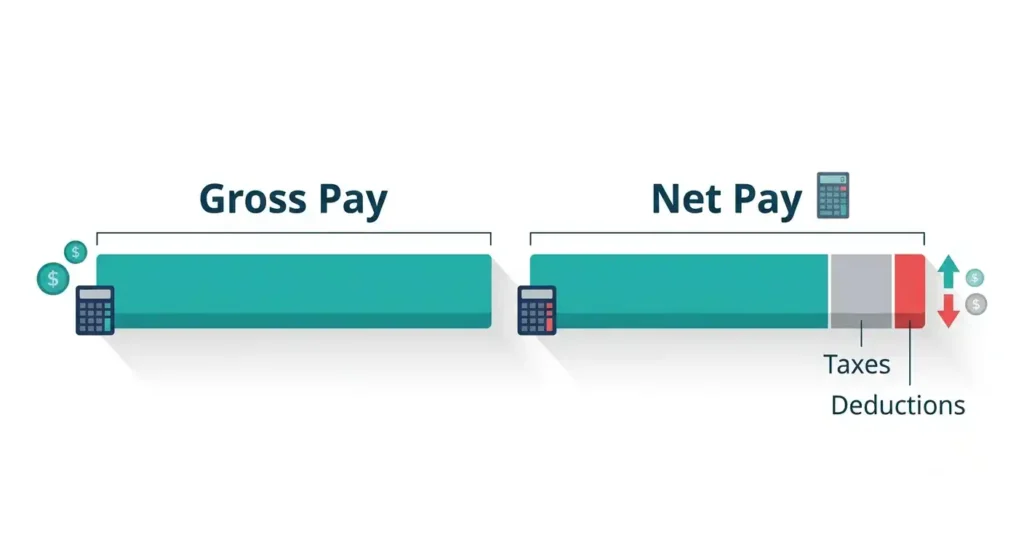

Gross pay is what you earn before deductions. Net pay is what actually lands in your bank account, and in California the gap between the two runs wider than in most states.

On a $75,000 salary, that gap can reach $650 to $750 every two weeks once federal tax, California tax, Social Security, Medicare, and SDI are all factored in. You can see the full breakdown in our $75,000 after taxes in California guide, or run your own numbers through our gross pay calculator.

The exact amount shifts based on your W-4 and DE 4 elections, but the pattern holds for nearly every California paycheck. Here is exactly where that money goes.

Gross Pay vs Net Pay at a Glance

Quick Comparison Table

| Gross Pay | Net Pay | |

|---|---|---|

| Definition | Total earnings before anything is taken out | What you actually receive |

| Where it appears | Top line of your pay stub | Bottom line, your deposit amount |

| When it matters | Salary talks, loan applications | Budgeting, daily spending |

| Typical use | Job offers, raises | Rent, bills, savings |

Gross Pay vs Net Pay Comparison

Gross pay is before the government and your benefits provider take their cut. Net pay is what’s left after federal tax, California tax, Social Security, Medicare, SDI, and any deductions you signed up for. Employers quote gross pay because it sounds bigger. Budget on net pay, it’s what you can actually spend. If you earn $5,000 a month in California, expect roughly $1,100 to $1,300 gone before you see a dollar, federal, state, and FICA combined.

What Is Gross Pay?

What Counts as Gross Pay

For more paycheck basics like this, it helps to start with the simplest definition. Gross pay is everything you earned before any deduction touches it: base salary, hourly wages, overtime, bonuses, commissions. If your employer paid you for it, it’s gross pay. A retail worker earning $22 an hour who picks up 10 hours of overtime at $33 an hour has both rolled into that week’s gross pay, taxed a bit differently once withholding kicks in. A salesperson closing a $50,000 deal at 5% commission adds $2,500 straight into that period’s gross pay. Annual salary is just gross pay multiplied over the year; hourly wages build to that same figure hour by hour, and our annual salary calculator does that math for you.

What Does NOT Reduce Gross Pay

Taxes don’t touch gross pay. Neither does your health insurance premium, 401(k) contribution, or a wage garnishment. Those come out later. Gross pay is a snapshot of what you earned, not what you kept, and confusing the two is where paycheck shock starts.

What Is Net Pay?

Why Net Pay Is Your Real Spending Money

Net pay is what hits your bank account, what covers rent, groceries, your car payment, and savings. Here is the real issue. After looking at hundreds of California pay stubs over the years, the pattern is always the same: people budget on gross pay, then come up short by the third week, wondering where the money went. It went to taxes and deductions that never touched their bank account in the first place. Net pay should drive your monthly budget, full stop.

How Net Pay Is Calculated

Gross Pay

Every calculation starts with gross pay for that period: regular wages plus anything extra earned, like overtime or a bonus.

Minus Pre-Tax Deductions

Pre-tax deductions come out first. Health insurance premiums, 401(k) contributions, and Health Savings Account (HSA) or Flexible Spending Account (FSA) contributions all lower your taxable income before the Internal Revenue Service (IRS) or the California Franchise Tax Board (FTB) sees it. Check the 2026 HSA contribution limits before you set your election. This is one of the few legal ways to shrink your tax bill while keeping more long term.

Minus Taxes

The biggest chunk disappears here. Federal income tax is withheld based on your W-4 (Form W-4), which starts from a much larger federal standard deduction than California allows. California income tax is withheld based on your DE 4 (Form DE 4), on a progressive scale from 1% up to 13.3% for income over $1 million. The Social Security tax and Medicare tax together make up FICA taxes, named after the Federal Insurance Contributions Act, taking 7.65% combined. California SDI takes 1.3% of every dollar, no wage cap in 2026.

Minus Post-Tax Deductions

What’s left can still shrink: union dues, wage garnishments, Roth 401(k) contributions, other after-tax deductions. Whatever survives is your net pay.

Gross Pay vs Net Pay Comparison Table

Side-by-Side Differences

| Gross Pay | Net Pay | |

|---|---|---|

| Definition | Total earnings | Take-home amount |

| Formula | Hours x rate, or salary / periods | Gross minus all deductions |

| Appears on paycheck | Top | Bottom |

| Used for | Job offers, taxes | Budgeting |

| Taxes | Not yet applied | Already applied |

| Job offers | Always quoted in gross | Rarely mentioned |

| Loan applications | Usually required | Sometimes requested as backup |

Every Deduction That Reduces Your California Paycheck

Mandatory Deductions

Five deductions hit nearly every California employee, no matter what job you have or what benefits you skip, and together they make up the bulk of California payroll taxes. Federal income tax follows your W-4 and bracket. California income tax follows the state’s progressive brackets. Social Security takes 6.2% up to the 2026 wage base of $184,500, capping your max contribution at $11,439. Medicare takes 1.45%, jumping to 2.35% once you cross $200,000, a threshold explained further in our $200,000 after taxes in California breakdown. Then there is SDI, which takes 1.3% of every dollar, zero wage ceiling in 2026, your entire salary, not just the first chunk.

Voluntary Deductions

These are the ones you actually choose, and that is where you have some control. Medical, dental, and vision premiums come out pre- or post-tax depending on your plan. A 401(k) lowers taxable income now. An HSA or FSA does the same, and the money stays earmarked for medical costs. Life insurance premiums, if employer-paid, usually come out post-tax. Some employers also offer commuter benefits, pre-tax dollars for transit or parking, working the same way a 401(k) does.

Court-Ordered Deductions

Not optional. Wage garnishments for unpaid debts, child support, and IRS or FTB tax levies get deducted automatically once your employer receives the order, on top of your regular withholding.

Why California Net Pay Is Lower Than Many Other States

California State Income Tax

California runs nine brackets from 1% to 12.3%, plus an extra 1% Mental Health Services Tax, now called the Behavioral Health Services Tax, on income over $1 million: a true top rate of 13.3%, the highest in the country. See the full California tax brackets for 2026 for every income range. California first subtracts a standard deduction of $5,706 for single filers or $11,412 for joint filers, so taxable income is always lower than gross salary. A single filer earning $75,000 has about $69,294 in taxable income after the deduction, landing in the 8% bracket, still enough to notice.

California SDI

California State Disability Insurance (SDI), administered by the California Employment Development Department (EDD), funds disability insurance and Paid Family Leave. It has no income cap. The 2026 SDI rate is 1.3%, up from 1.2%, and since Senate Bill 951 removed the wage ceiling in 2024, high earners pay it on every dollar, all year. A $200,000 earner pays $2,600 in SDI for the year, something that didn’t happen before 2024.

Federal Taxes Still Apply

California’s state taxes stack on top of federal ones. Federal income tax, Social Security, and Medicare apply the same way they would in Texas or Florida; California just adds a layer. Someone relocating from a no-income-tax state like Texas or Florida can see net pay drop several hundred dollars a month the moment California withholding starts, even at the same salary.

Gross Pay vs Taxable Income vs Net Pay

Three Numbers People Confuse

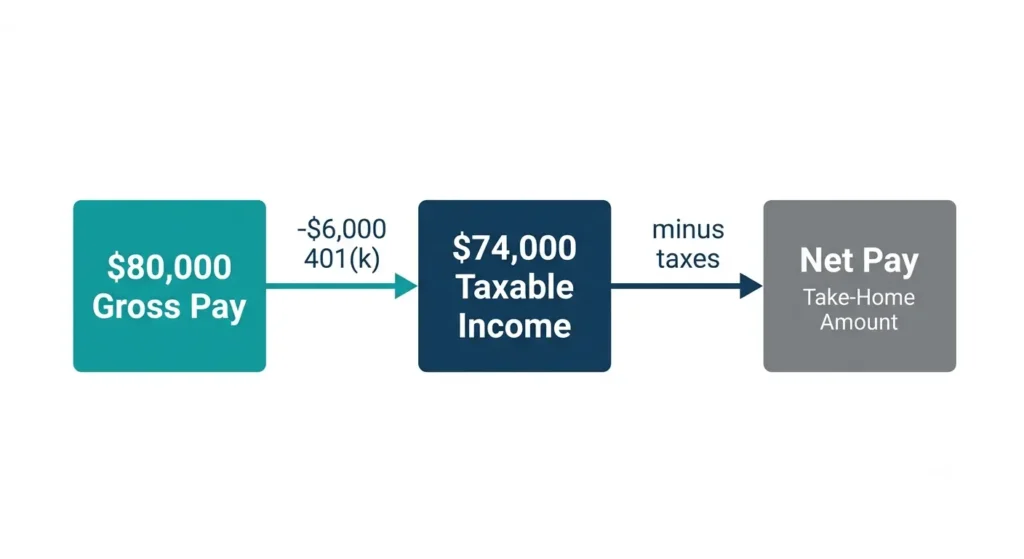

Gross pay is what you earned. Taxable income is gross pay minus pre-tax deductions like your 401(k) or health premiums, what the IRS and California Franchise Tax Board (FTB) actually tax. Net pay is what’s left after every deduction. A worker earning $80,000 who puts $6,000 into a 401(k) has $80,000 gross, $74,000 taxable, and net pay calculated off that $74,000. That income also feeds your adjusted gross income (AGI) at tax time, a separate figure the IRS uses for credit and deduction eligibility, distinct from both gross and net pay.

Which Number Matters in Different Situations

Taxable income for your tax bill. Net pay for your budget. Gross pay for salary offers and loan applications. Mixing these up is the most common planning mistake out there.

California Paycheck Example (Step-by-Step)

Hourly Employee Example

$22 an hour, 80 hours biweekly, $1,760 gross. Federal withholding roughly $150, California around $35, Social Security $109, Medicare $26, SDI $23. Net pay lands near $1,417, about 80% of gross. Federal and state figures are estimates from standard single-filer withholding tables; Social Security, Medicare, and SDI are fixed percentages.

Salaried Employee Example

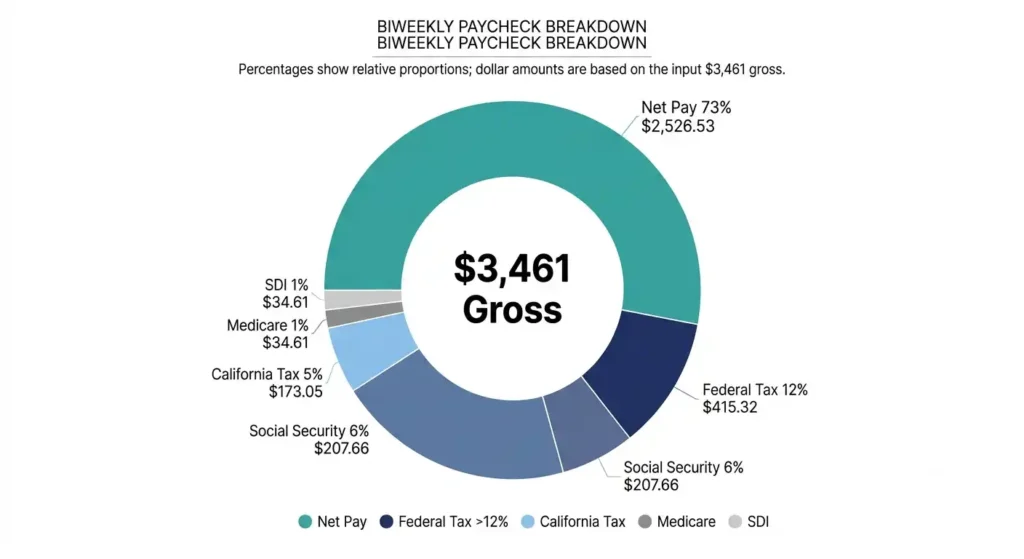

$90,000 a year is $3,461 gross biweekly. Federal withholding around $420, California around $190, Social Security $215, Medicare $50, SDI $45 (federal and state estimated). Net pay lands near $2,541, about 27% lost to taxes. The same salary is roughly $1,731 gross weekly, $3,750 semi-monthly, $7,500 monthly. The tax percentage stays about the same; only check size changes.

Bonus Pay Example

Bonuses get hit differently: a flat 10.23% California withholding on supplemental wages, plus a flat 22% federal rate for bonuses under $1 million, as covered in our California bonus tax rate guide. A $10,000 bonus loses $2,200 federal, $1,023 California, $620 Social Security, $145 Medicare, leaving around $5,882 after SDI. That flat rate isn’t your final tax bill, it reconciles when you file.

Overtime Example

Overtime is taxed like regular wages under California overtime laws, though withholding often looks higher since payroll assumes that rate all period. 10 hours at $33 adds $330 gross; between federal, state, FICA, and SDI, expect $90 to $100 gone before it hits your account.

Common Real-Life Scenarios

These paycheck scenarios come up constantly, and each one has a straightforward explanation once you know where to look.

First Paycheck Looks Too Small

New hires often hit a partial pay period, retroactive benefit deductions, or a higher default withholding before their W-4 and DE 4 fully process. Check actual hours paid and confirm your elections before assuming an error.

Comparing Two California Job Offers

Never compare gross salary alone. A $95,000 offer with a high-deductible plan and no 401(k) match can net less than an $88,000 offer with strong benefits and a 4% match. Estimate net pay for both and factor in real benefit costs.

Planning Monthly Expenses

Rent, utilities, groceries, savings: build all of it around net pay, never gross. Budgeting off your offer letter instead of your actual deposit sets up a shortfall by the second or third week.

Checking Whether Payroll Made a Mistake

Check hours worked, then withholding elections, then benefit deductions. Most errors trace to missing hours or an outdated W-4 or DE 4, not a system glitch. Our why is my paycheck so low guide walks through the six most common causes. If it still doesn’t add up, ask HR to walk through each line. Missing hours, a duplicated deduction, or an uncancelled benefit are the usual culprits. California employers must follow Labor Code § 221 and Labor Code § 224, part of the broader California labor law payroll deductions framework limiting what can legally come out of your wages. If HR can’t resolve it, the California Department of Industrial Relations (DIR) and its Division of Labor Standards Enforcement (DLSE) handle wage and deduction complaints.

Common Mistakes and Misconceptions

Gross Pay Equals Take-Home Pay

The single biggest source of paycheck disappointment. Gross pay is a promise, net pay is reality; they’re never the same once taxes and deductions hit. A related mix-up: gross pay is not taxable income. Pre-tax contributions lower taxable income below gross pay before taxes are even calculated.

Everyone With the Same Salary Gets the Same Net Pay

Two coworkers at an identical $80,000 can take home noticeably different amounts. One maxes a 401(k) and carries family coverage, the other doesn’t. Filing status and W-4 elections shift it further. A married employee filing jointly usually has less withheld than a single filer at the same salary, and claiming dependents on your W-4 or DE 4 reduces withholding more.

Bigger Gross Pay Always Means Bigger Take-Home

A raise into a higher bracket doesn’t mean less money overall, California only taxes the portion inside the new bracket. But a raise combined with higher benefit costs or a filing status change can shrink the net increase more than expected.

Net Pay Never Changes

It moves constantly. A bonus, overtime, a W-4 or DE 4 change, or a new benefit election can all shift what lands in your account even if base salary stays the same.

Which Number Should You Use?

Budgeting

Net pay, always. It’s the only number that reflects money you can actually spend.

Salary Negotiation

Gross pay. Employers think in gross terms, so should you.

Comparing Job Offers

Gross pay plus real benefit value, then estimate net pay for each. The higher salary isn’t always the higher take-home.

Mortgage or Apartment Applications

Lenders and landlords ask for gross income, then verify with pay stubs or tax returns. Keep both numbers handy.

How to Read a California Pay Stub

This section covers the essentials, and our full how to read a California pay stub guide goes deeper with annotated examples.

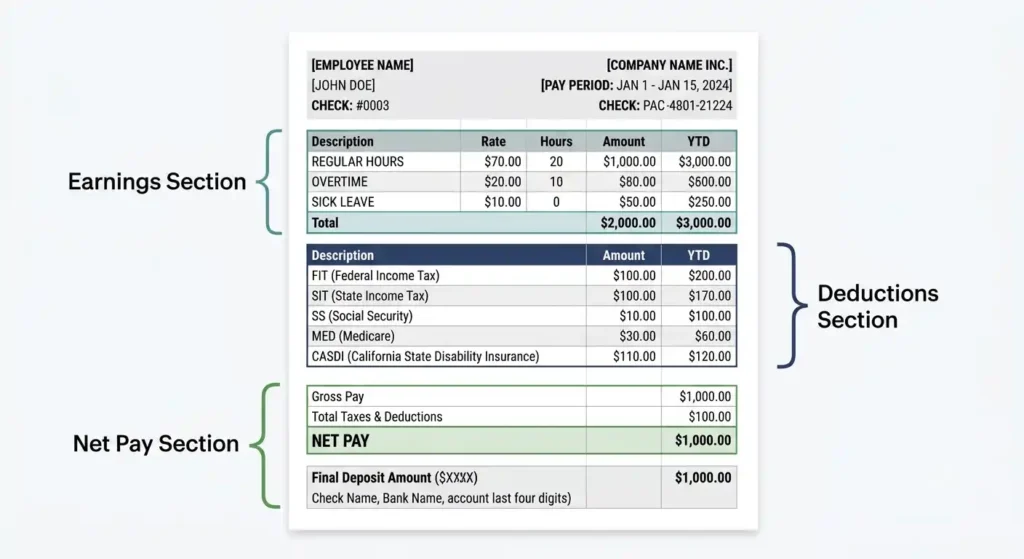

Earnings Section

Lists gross wages for the period: regular hours, overtime hours, any bonus or commission that cycle.

Deductions Section

Every tax withheld, federal, California, Social Security, Medicare, SDI, plus benefit or retirement deductions elected. Common abbreviations: FIT for federal income tax, SIT for state income tax, SS or OASDI for Social Security, MED for Medicare, CASDI for SDI.

Net Pay Section

The final line is your actual deposit, plus year-to-date totals for earnings and withholding in 2026. It’s the number sent to your bank through direct deposit, usually a day or two before payday. Your Form W-2 reports full taxable wages at year-end, which is why it rarely matches your final pay stub exactly, since pre-tax deductions are already stripped out.

Frequently Asked Questions

Is gross pay before taxes?

Yes, total earnings before any tax or deduction.

Is net pay the same as take-home pay?

Yes, same thing: the amount that lands in your bank account.

Why is my California paycheck so much lower than my salary?

California stacks state income tax and SDI on top of federal taxes and FICA, pulling a larger share than most states.

Why did my net pay change even though my salary stayed the same?

Overtime, bonuses, a new W-4 or DE 4, or a benefit election change can all shift net pay period to period.

Should I negotiate salary using gross or net pay?

Gross pay. Employers and offer letters are built around gross figures.

Which income do banks use for loans?

Gross income first, verified with pay stubs or tax returns.

Can two employees with the same salary have different net pay?

Yes. Filing status, W-4 and DE 4 elections, and benefit choices all change the final number.

What is the difference between gross pay and taxable wages?

Taxable wages are gross pay minus pre-tax deductions like a 401(k) or health premium, the number your taxes are calculated from.

Does overtime increase net pay as much as gross pay?

No. Overtime is taxed like regular wages, so a portion disappears into withholding too.

How do W-4 and DE 4 affect my paycheck?

They tell your employer how much federal and California tax to withhold. Withhold too much and you get a tax refund next spring, an interest-free loan to the government. Withhold too little and you owe money, sometimes with an underpayment penalty.

Key Takeaways

Gross pay is what you earned. Net pay is what you keep. California pulls more from every paycheck than most states because of its progressive income tax and uncapped SDI rate. Use gross pay for negotiating and loan applications; build your budget around net pay every time. Once you know where every dollar goes, running the numbers through our California paycheck calculator gives you a real estimate before payday arrives.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.