A $130,000 California salary is what you earn before federal tax, California state tax, Social Security, Medicare, and state disability insurance all take their share. Your real take-home lands well below that number, and filing status changes it further.

I ran these exact 2026 IRS and California FTB figures through the math myself, testing single, married, and 401(k) scenarios.

California hasn’t finalized 2026 bracket thresholds yet, so these numbers are close estimates, not exact.

Quick Answer: How Much Is $130K After Taxes in California?

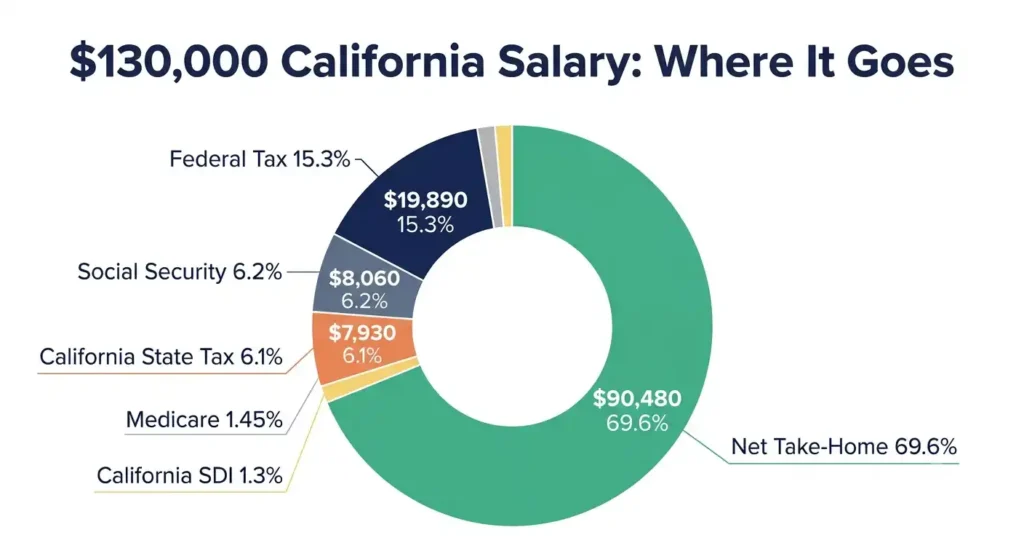

A single filer earning $130,000 in California in 2026 takes home about $90,473 a year, close to 70% of gross pay. The rest, about $39,500, goes to federal income tax, California state income tax, Social Security tax, Medicare tax, and California State Disability Insurance (SDI). Think about it this way: on a $10,833 gross month, about $3,294 disappears before you ever touch it. If you want to run a different salary through the same math, our annual salary calculator breaks it down the same way.

Estimated Take-Home Pay at a Glance

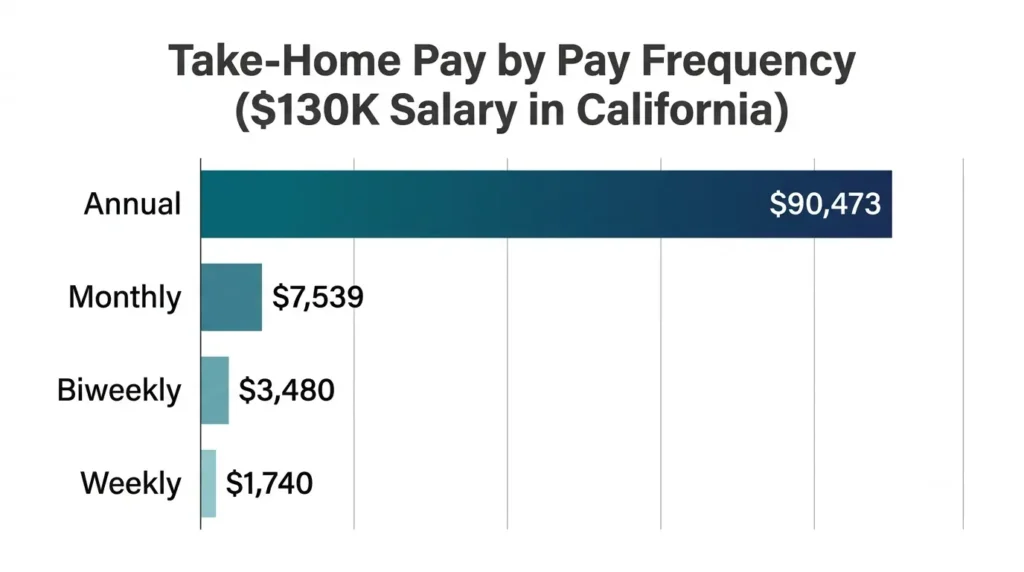

Annually: $90,473. Monthly: $7,539. Biweekly: $3,480. Weekly: $1,740. Hourly, over a 2,080-hour year: about $43.50 after taxes.

Quick Salary Breakdown Table

| Item | Amount |

|---|---|

| Gross salary | $130,000 |

| Federal income tax | $19,934 |

| California state tax | $7,958 |

| Social Security (6.2%) | $8,060 |

| Medicare (1.45%) | $1,885 |

| California SDI (1.3%) | $1,690 |

| Total estimated taxes | $39,527 |

| Estimated net income | $90,473 |

These numbers assume a single filer, the standard deduction, and no pre-tax deductions. Change any of those and the number moves. Prefer to check gross versus net side by side yourself? Our gross pay calculator lets you test it directly.

Free California Tax Tool

See What $130,000 Actually Puts in Your Pocket

$130K in California looks great on paper — but after federal tax, state tax, and SDI, your real take-home is a different number. See it now.

🧮 See My Exact $130K Take-Home After TaxesUsed by thousands of California workers · FTB-verified 2026 rates

How a $130,000 California Salary Is Taxed

Four things hit your paycheck: federal income tax, California state income tax, FICA (Social Security tax and Medicare tax), and California SDI. Each runs its own math, separately, and you can explore each one further in our California payroll taxes section.

Federal Taxes

The Internal Revenue Service (IRS) uses seven brackets in 2026, from 10% to 37%. Your standard deduction of $16,100 drops taxable income to $113,900. Taxed in layers per the IRS tax brackets, your bill comes to $19,934, lower than the “24% bracket” scare implies.

California State Taxes

The California Franchise Tax Board (FTB) runs nine brackets, 1% to 12.3% (13.3% above $1 million), detailed further in our California tax brackets 2026 guide. Your standard deduction is only $5,706, so taxable income stays at $124,294. Most of it falls in the 9.3% bracket. Total state tax: about $7,958, after the personal exemption credit. Note: the FTB finalizes exact brackets late in the year, so this is a close estimate. This also assumes full-year California residency. Moving mid-year or working remotely for an out-of-state employer may require a part-year or nonresident return.

Payroll Taxes

You owe Social Security tax at 6.2% and Medicare tax at 1.45%, both on the full $130,000 since you’re under the $184,500 Social Security wage base. That’s $8,060 and $1,885. California adds California State Disability Insurance (SDI) at 1.3%, no cap: $1,690, a rate broken down further in our CA SDI rate 2026 guide.

Tax Breakdown Explained

Four taxes, four rulebooks. That’s why two people earning $130,000 can take home different amounts.

Federal Income Tax

Taxable income is salary minus the standard deduction ($16,100 for single filers). The IRS taxes it in chunks: 10% on the first $12,400, 12% on the next slice, up to 24% above $105,700. Here’s the part people get wrong constantly: hitting the 24% bracket does not mean 24% of your paycheck disappears. Only that top slice is taxed there. Your effective rate lands near 15%. Your marginal tax rate, 24%, only applies to your last dollars earned. Think about it this way: on a $130,000 salary, you’re not handing over $31,200 to the IRS. You’re handing over $19,934, and most of that sits in the lower brackets.

California Income Tax

Same layered system, more steps, less shelter. Nine brackets instead of seven, and a much smaller standard deduction. Simply put, that gap, not one giant tax bite, is why California take-home pay looks lower than a no-tax state at the same salary. I see people blame the 9.3% bracket every year. The real culprit is the standard deduction being a fraction of the federal one.

FICA Taxes

Social Security tax takes 6.2%, Medicare tax takes 1.45%, both flat, no deductions to lower them. Social Security stops at the $184,500 wage base. Medicare never caps, and above $200,000 as a single filer, an extra 0.9% Additional Medicare Tax kicks in, which we walk through in our $200K after taxes California breakdown. At $130,000, you’re not there yet.

California SDI

SDI funds disability insurance and paid family leave, administered by the EDD. Mandatory, no opt-out. Since Senate Bill 951 removed the wage cap in 2024, all wages get hit at 1.3% in 2026. On $130,000: $1,690 a year.

Your Estimated Take-Home Pay by Pay Frequency

Your $130,000 lands differently depending on how often you’re paid.

Annual Pay

Annual Net Income

Gross: $130,000. Total taxes: about $39,527. Net: $90,473, just under 70% of gross, before any 401(k) or health insurance deductions.

Monthly Pay

Budget around $7,539 a month, not your $10,833 gross. A common rule keeps rent under 30% of net income, about $2,260 a month here.

Biweekly Pay

Most California employers pay biweekly, 26 checks a year, around $3,480 each.

Semi-Monthly Pay

Paid twice monthly instead? That’s 24 checks, around $3,770 each. Same annual total as biweekly, different math per check.

Weekly Pay

Weekly pay means 52 checks, about $1,740 each.

Real-Life Examples

Three common scenarios, same $130,000 salary, different results.

Single Employee With No Pre-Tax Deductions

Federal $19,934, state $7,958, Social Security $8,060, Medicare $1,885, SDI $1,690. Net: $90,473 a year, $7,539 a month.

Employee Contributing to a 401(k)

Put $10,000 into a traditional 401(k) and it skips taxable income entirely. Federal tax drops about $2,364, state tax about $930, saving $3,294 combined. Net take-home only drops about $6,706, not the full $10,000.

Married Employee

Sole earner, married filing jointly? Standard deductions jump to $32,200 federal and $11,412 California. Federal tax falls to about $11,240, state tax to about $4,120. Net income: about $103,005, roughly $12,500 more than the single filer example, from filing status alone. If your spouse also earns income, that stacks on top and can push your household into higher brackets.

How $130K Compares to Other Salaries

Nearby salaries make the tax math clearer. Browse our full paycheck scenarios collection for more comparisons like these.

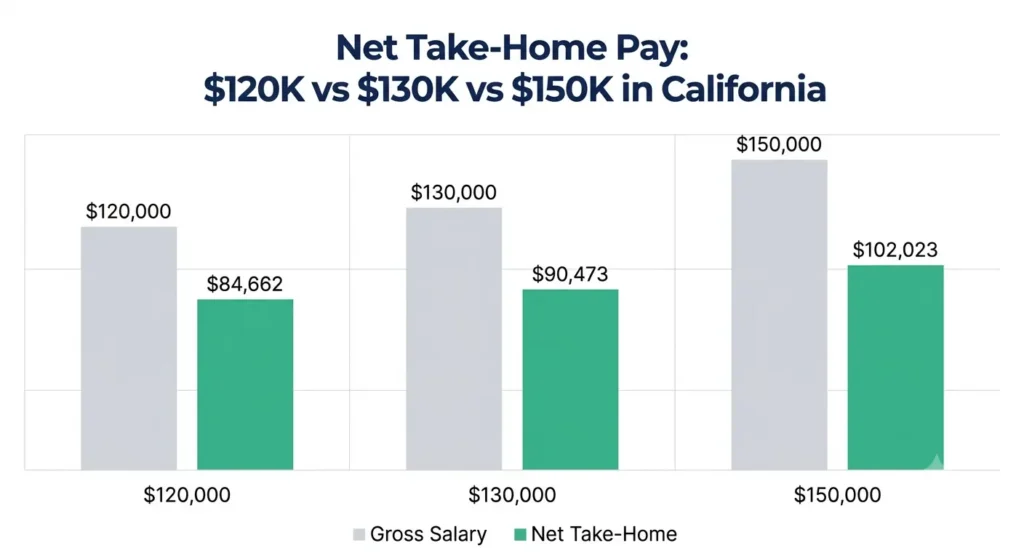

$120K vs $130K

At $120,000, net is about $84,662, detailed in our $120K after taxes California breakdown. The $10,000 raise to $130,000 adds only about $5,811 to take-home, about 58% of the raise.

$130K vs $150K

At $150,000, net climbs to about $102,023, a gain of $11,550, covered in full in our $150K after taxes California guide. Still about 58% kept, showing the marginal rate holds steady here.

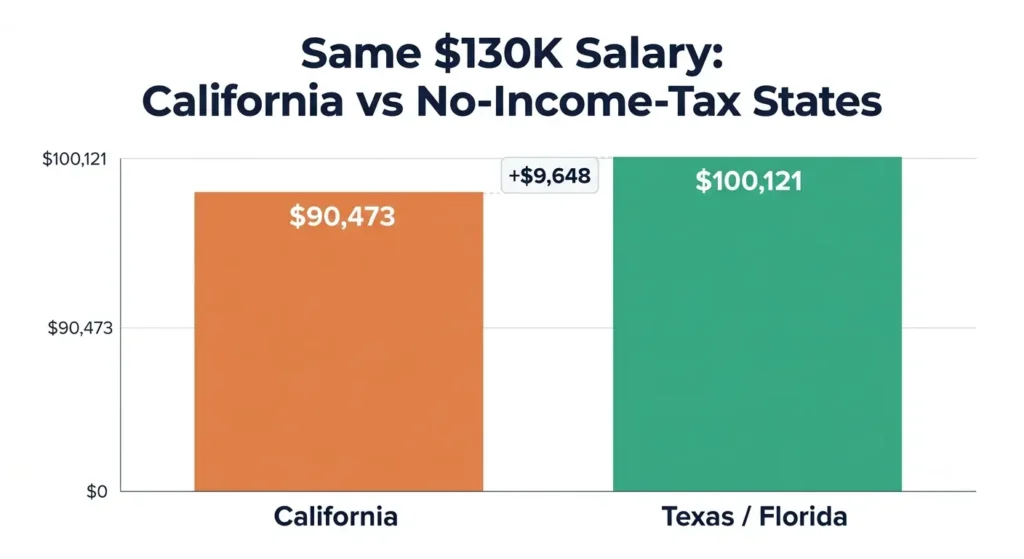

California vs No-Income-Tax States

Same $130,000 in Texas or Florida skips state income tax and SDI. Federal and FICA stay the same, but net comes to about $100,121, roughly $9,648 more than in California.

Why Your Take-Home Pay May Be Different

Your actual paycheck depends on choices you make on paper, not just your salary.

Filing Status

Single, married filing jointly, and head of household use different brackets and standard deductions. Married filing separately uses the same bracket schedule as single filers in California, no extra room there. Filing status alone can shift net income by over $12,000 a year at this salary.

Form W-4 Elections

Your Form W-4 sets your withholding, paired with California’s own DE-4 form for state withholding. Claiming dependents, requesting extra withholding, or working multiple jobs all change your paycheck, though your final tax bill stays the same. Dependents lower withholding through the dependent tax credit built into the W-4. Independent contractors skip this entirely: no withholding, plus self-employment tax on top, so an employee paycheck calculator won’t fit their situation. See our 1099 vs W-2 California comparison for the real difference.

Pre-Tax Deductions

Retirement Contributions

A traditional 401(k) contribution lowers taxable income before tax is calculated. As shown, $10,000 in costs only about $6,706 in real take-home pay. A Roth 401(k) works opposite: taxed now, tax-free in retirement, so it doesn’t reduce this year’s take-home pay.

Health Benefits

Health insurance premiums, a Health Savings Account (HSA), or a Flexible Spending Account (FSA) all come out pre-tax. So do dental, vision, and commuter benefit deductions. Same effect: lower taxable income, smaller but more efficient paycheck reduction.

Common Mistakes People Make

I see the same three mistakes come up again and again when people try to estimate their own California paycheck.

Confusing Gross Pay With Net Pay

Budget off your $90,473 net, not your $130,000 salary. That’s the fastest way to overspend. Our gross pay vs net pay guide breaks down exactly where the difference goes.

Thinking the Highest Tax Bracket Applies to All Income

This is the mistake covered earlier: only your top slice gets taxed at your highest bracket, not your whole paycheck.

Ignoring Payroll Deductions

Insurance, retirement contributions, and other benefits come out before you see your paycheck. Skip this step and your estimate can be off by hundreds a month. If your number ever looks off, our why is my paycheck so low guide walks through the usual culprits.

Frequently Asked Questions

Is $130K considered a good salary in California?

Depends on where you live. In San Francisco or San Jose, it covers the basics with little left over. In Fresno or Sacramento, it stretches much further. Comparing salaries without factoring in cost of living is a common mistake.

How much will I take home each month on $130K?

About $7,539 as a single filer with no pre-tax deductions. A 401(k) contribution or health premium lowers that further.

Why does every paycheck calculator give different results?

Different W-4 assumptions, deductions, or rounding. None are wrong, just built differently. See our methodology for the exact assumptions used here. Also remember: withholding isn’t your tax liability. Overpay and you get a tax refund. Underpay and you owe in April.

Does contributing to a 401(k) increase my take-home pay?

No, it lowers it, just by less than you put in, as shown above.

Will bonuses be taxed differently?

Yes. Bonuses get a flat 22% federal withholding under $1 million, separate from regular bracket-based withholding. California applies its own flat supplemental rate too. RSU vesting gets the same supplemental treatment. Overtime and commission usually fold into your regular paycheck at your normal rate. Your final tax bill evens out at filing time either way.

Can I reduce taxes legally on a $130K salary?

Yes. A traditional 401(k) or HSA lowers taxable income directly. Pre-tax health benefits do the same. Both are simple, no-risk ways to keep more of $130,000.

Final Takeaway

$130,000 in California nets about $90,473 a year, or $7,539 a month, for a single filer.

Key Numbers to Remember

Net: $90,473 a year. Monthly: $7,539. Filing status, 401(k) contributions, and where in California you live move that number most.

Next Steps

Check your W-4 for your actual withholding. Compare job offers by net pay, not gross. Negotiate around your target take-home number. Then build your budget around $7,539, not $10,833.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.