1099 contractors in California pay the full 15.3% self-employment tax, while W-2 employees split that cost with their employer. That gap alone costs a contractor over $7,000 more per year on $100,000 of income. But taxes are only part of the picture. Health insurance, retirement matching, and unpaid time off can quietly erase a higher contractor rate before it ever reaches a bank account. The right answer depends on total compensation, not just the number on the offer letter. Results vary based on income level, deductions claimed, and individual benefits. Use our 1099 vs W-2 calculator to run the numbers for your specific situation. For broader paycheck basics in California, our resource library covers everything from withholding to net pay.

Free California Tax Tool

1099 or W-2 — Which One Actually Pays You More?

The higher-paying offer isn’t always the better one. Compare your real take-home pay under both — after self-employment tax, state tax, and all deductions.

🧮 Find Out Which Pays More — 1099 or W-2Used by thousands of California workers · FTB-verified 2026 rates

1099 vs W-2 at a Glance

Quick Comparison Table

| Factor | W-2 Employee | 1099 Contractor |

|---|---|---|

| Tax withholding | Employer withholds taxes automatically | You pay taxes yourself |

| Social Security and Medicare | Split 50/50 with employer | You pay the full 15.3% |

| Health insurance | Often employer-subsidized | You pay out of pocket |

| Paid time off | Usually included | Not included |

| Workers’ compensation | Covered by employer | Not covered |

| Unemployment insurance | Employer pays | Not available |

| California SDI | Withheld from wages | Not applicable |

| Quarterly tax payments | Not required | Required |

| Schedule C deductions | Not available | Available |

Key Differences in One Minute

A W-2 employee works under direct company control. Taxes are withheld automatically, and most employees owe little or nothing at tax time.

A 1099 independent contractor runs their own business. No taxes are withheld. Income is reported on Form 1099-NEC once a client pays $2,000 or more in a calendar year, following the threshold increase under the One Big Beautiful Bill Act effective January 1, 2026. The contractor files Form 1040 plus Schedule C, Schedule SE, and Form 1040-ES.

Before work begins, contractors fill out a Form W-9 to provide their name, address, and taxpayer identification number to the hiring company. The IRS uses a 3-factor test covering behavioral control, financial control, and type of relationship to determine classification. California previously used the Borello test before AB 5 replaced it with the stricter ABC framework.

How Taxes Work for W-2 Employees in California

Taxes Automatically Withheld

California W-2 employees have federal income tax withheld via Form W-4, state income tax via Form DE-4, Social Security at 6.2% on wages up to $184,500, Medicare at 1.45% on all wages, and California SDI at 1.3% on all wages with no income cap, per Senate Bill 951 effective 2024.

What Employers Pay on Your Behalf

On top of your salary, employers pay 6.2% Social Security, 1.45% Medicare, FUTA at 6% on the first $7,000 of wages, California State Unemployment Insurance between 1.5% and 6.2%, and workers’ compensation averaging 1% to 3% of payroll. None of this appears on your paycheck, but it directly affects what a company can afford to pay you.

W-2 employees also receive California labor protections: overtime after 8 hours a day or 40 hours a week, mandatory meal and rest breaks, wrongful termination protections under the California Labor Code, and EDD disability benefits. Contractors have none of these. When a contract ends, there is no unemployment claim and no wage claim process.

Why W-2 Employees Usually Owe Less at Tax Time

Withholding collects roughly the right amount throughout the year. Employees who file correct W-4 and DE-4 forms typically owe a few hundred dollars or get a small refund. No quarterly deadlines, no underpayment penalties.

How Taxes Work for 1099 Contractors in California

Self-Employment Tax Explained

As a contractor, you are both the employee and the employer. That means you owe both halves of FICA, not just your half.

Social Security Portion

12.4% on net self-employment earnings up to $184,500 in 2026. Above that threshold, the Social Security portion stops. The IRS confirms the 2026 Social Security wage base each year through Topic No. 751.

Medicare Portion

2.9% on all net self-employment income with no cap. Income above $200,000 (single) or $250,000 (married filing jointly) adds a 0.9% Additional Medicare Tax, bringing the rate to 3.8% on earnings above those thresholds.

Self-employment tax is calculated on 92.35% of net earnings. You can also deduct 50% of total self-employment tax as an above-the-line deduction on your federal return, which lowers adjusted gross income but does not reduce the self-employment tax itself. The IRS Schedule SE instructions walk through this calculation step by step.

Federal and California Income Taxes

Contractors owe federal income tax at the same 10% to 37% brackets as W-2 employees. California adds 1% to 12.3%, with a 1% surcharge on income above $1 million bringing the top rate to 13.3%. California’s standard deduction is only $5,706 for single filers versus $16,100 federally, so California taxable income is often much higher.

California does not conform to the federal QBI deduction under IRC Section 199A, which lets eligible self-employed workers deduct up to 20% of net business income federally. The IRS explains QBI eligibility and limits in detail. No equivalent benefit exists on the state return, as confirmed by the California Franchise Tax Board.

Quarterly Estimated Tax Payments

Contractors must pay taxes quarterly. Federal due dates fall in April, June, September, and January. The IRS estimated tax page lists all current deadlines and the Form 1040-ES instructions. The California Franchise Tax Board publishes California’s quarterly due dates separately. The safe harbor rule protects you if you pay 100% of last year’s tax liability or 90% of the current year’s, whichever is smaller. Set aside 25% to 30% of every payment received. For a full breakdown of all California payroll taxes that apply to both employees and contractors, our dedicated guide covers every rate and obligation.

Cash flow is the real challenge. Contractor payments arrive gross. Spending it all before a deadline turns tax season into a crisis. Tax software like QuickBooks Self-Employed, FreshBooks, or TurboTax Self-Employed can automate tracking and estimate payments. Many California contractors earning above $75,000 hire a CPA, and that cost is fully deductible.

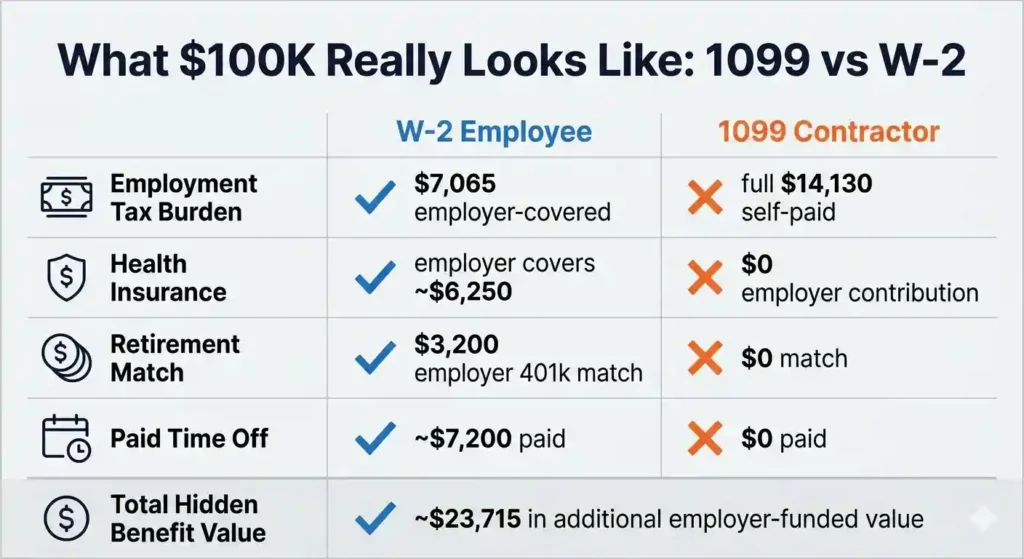

The Hidden Cost Most Comparisons Ignore: Employee Benefits

Health Insurance Value

California employer-sponsored health premiums average $7,000 to $9,000 per year for a single employee. Employers cover 70% to 80%, giving W-2 workers $5,000 to $7,500 in non-taxable compensation that never appears on the job listing. Contractors pay the full premium themselves. Family coverage runs $18,000 to $24,000 annually.

Retirement Benefits

A 4% employer 401(k) match on an $80,000 salary is worth $3,200 per year — free money a contractor never receives. Contractors can open a SEP-IRA or Solo 401(k), but no one matches their contributions. California employers without a qualifying retirement plan are also required to enroll employees in CalSavers, another benefit unavailable to 1099 workers.

Paid Time Off

Five weeks of paid time off on a $75,000 salary is worth roughly $7,200. A contractor who takes the same time off earns nothing. That cost must be priced into the contractor rate from day one. W-2 employees also accrue protected California sick leave that contractors are not entitled to.

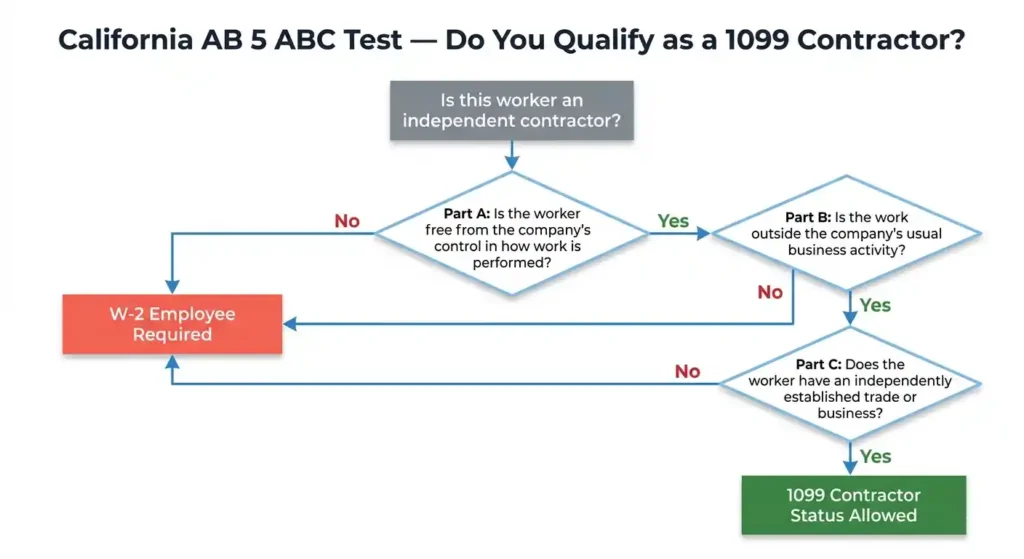

California AB 5 and Worker Classification Rules

What AB 5 Means

AB 5, effective January 2020, requires businesses to prove a worker qualifies as a contractor rather than an employee. The full text of Assembly Bill 5 is available through the California Legislature’s official portal. Gig workers were central to the debate. Uber and DoorDash resisted the law until voters passed Proposition 22 in 2020, carving out a limited exemption for app-based drivers. Outside those exemptions, misclassified workers face back taxes, unpaid benefits, and audit risk from the IRS and EDD. For a deep dive into how this test works in practice, our California ABC test guide for 2026 walks through every part with real examples. You can also browse all our worker classification resources for related guidance.

Understanding the ABC Test

All three parts must be satisfied for a worker to legally qualify as an independent contractor. Failing even one means the worker is a W-2 employee.

Part A

The worker must be free from the company’s control and direction in how the work is performed. Mandatory hours, scripted processes, or required daily video calls likely fail Part A.

Part B

The work must be outside the usual course of the hiring company’s business. A freelance graphic designer hired by a graphic design firm fails Part B. A plumber hired by a software company passes.

Part C

The worker must be engaged in an independently established trade or business of the same nature. One-client contractors with no business infrastructure typically fail Part C.

Tax Deductions Available to 1099 Contractors

Home Office Deduction

A dedicated space used exclusively for business qualifies. The simplified method allows $5 per square foot up to 300 square feet, for a maximum $1,500 deduction. The regular method uses the percentage of home square footage against actual expenses. Exclusive use is strict: a spare bedroom doubling as a guest room does not qualify.

Vehicle and Mileage Deductions

The 2026 IRS standard mileage rate is $0.725 per mile, as published in IRS Notice 2026-5. Contractors can instead track actual vehicle expenses and deduct the business-use percentage. A contemporaneous mileage log is required either way. Daily commuting to a regular client office is not deductible; driving to meet clients or pick up supplies is.

Equipment and Software Expenses

Computers, phones, software subscriptions, and internet service (business-use percentage) are deductible on Schedule C. A laptop used 70% for business yields a 70% deduction. Section 179 of the tax code allows full-year deduction in the purchase year rather than depreciation. Professional license fees, accounting fees, and bookkeeping costs are also deductible, including CPA fees.

Retirement and Health Insurance Deductions

A SEP-IRA allows up to 25% of net self-employment income, capped at $72,000 in 2026. A Solo 401(k) combines employee contributions up to $24,500 plus employer contributions up to 25% of compensation, for a combined 2026 limit of $72,000 under age 50. The IRS retirement plan contribution limits page confirms all 2026 figures. Self-employed health insurance premiums are fully deductible above the line on Form 1040, reducing adjusted gross income dollar for dollar.

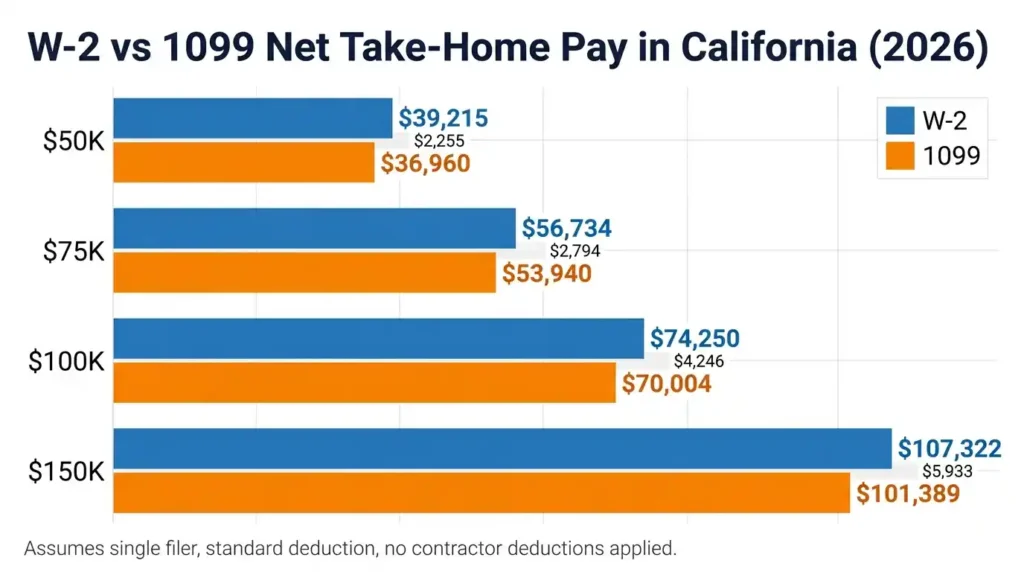

Side-by-Side Tax Comparison: 1099 vs W-2

All examples assume a single California filer using the standard deduction with no contractor deductions applied. Real 1099 tax bills will be lower with legitimate deductions.

$50,000 Income Example

W-2: ~$12,110 total taxes. Net take-home ~$37,890. 1099: ~$14,365 total taxes. Net take-home ~$35,635. Difference: $2,255 less.

$75,000 Income Example

W-2: ~$19,803 total taxes. Net take-home ~$55,197. 1099: ~$22,597 total taxes. Net take-home ~$52,403. Difference: $2,794 less. For a full breakdown of what a $75,000 salary looks like after taxes in California, including monthly and biweekly take-home figures, see our dedicated guide.

$100,000 Income Example

W-2: ~$28,684 total taxes. Net take-home ~$71,316. 1099: ~$32,930 total taxes. Net take-home ~$67,070. Difference: $4,246 less, and $7,065 more in employment taxes alone. See exactly how $100,000 is taxed in California as a W-2 employee for the full paycheck breakdown.

$150,000 Income Example

W-2: ~$49,148 total taxes. Net take-home ~$100,852. 1099: ~$55,081 total taxes. Net take-home ~$94,919 before deductions. Aggressive SEP-IRA or Solo 401(k) contributions close the gap substantially. Our guide to $150,000 after taxes in California shows exactly what W-2 employees keep at this income level.

Take-Home Pay Comparison After Taxes and Benefits

Why Higher Contractor Pay Can Be Misleading

A 1099 offer at $100,000 does not match a W-2 at $100,000. The contractor’s gross must cover the employer’s share of FICA, health insurance, unmatched retirement, and unpaid time off. Equal gross pay is actually a pay cut.

Calculating Total Compensation

Add employer health contributions ($5,000 to $8,000 for a single employee), 401(k) match (3% to 5% of salary), and PTO value to the W-2 salary for total compensation. Then subtract all 1099 costs — extra FICA, insurance, lost match, unpaid vacation. Compare the results, not the headline numbers.

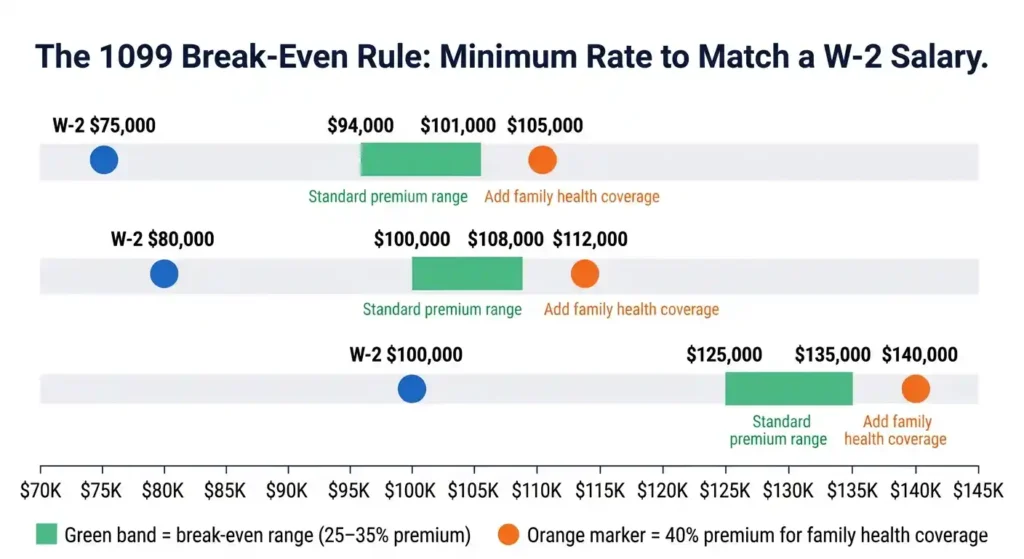

The Contractor Pay Raise Rule

A 1099 rate needs to be 25% to 35% higher than a W-2 salary just to break even. On a $75,000 W-2 with solid benefits, the equivalent 1099 rate is $94,000 to $101,000. Many California contractors recommend 40% when family healthcare is factored in.

Real-World Scenarios

Freelancer Choosing Between Two Offers

A San Jose software developer compares a W-2 at $120,000 with $8,000 in employer health coverage, a $4,800 401(k) match, and 15 vacation days (total value ~$139,800) against a 1099 contract at $140,000. After accounting for $14,000 in extra self-employment taxes, $9,000 in health insurance, $4,800 in lost match, and $7,000 in unpaid vacation, the 1099 nets ~$105,200 in effective compensation. The W-2 wins by over $34,000. Use the San Jose paycheck calculator to model your own numbers, or explore more real-world paycheck scenarios for California workers.

Remote Worker Receiving a Contract Offer

A Los Angeles marketing manager offered a switch from W-2 to 1099 at the same base rate faces two problems. First, it may violate AB 5 if the work and relationship are unchanged. Second, the same rate means a significant pay cut once benefits are removed. Negotiate the rate up or stay W-2.

Contract-to-hire arrangements carry similar risk. Get the conversion timeline in writing and price the contract rate at the full 1099 premium. Switching back from 1099 to W-2 is straightforward. Going from W-2 to 1099 requires expense tracking, a separate business bank account, and a tax reserve before the first quarterly deadline.

Worker With Both W-2 and 1099 Income

Side 1099 income is reported on Schedule C alongside W-2 income. Self-employment tax applies to any net 1099 profit above $400. If your W-2 already maxes Social Security withholding, your 1099 Social Security tax is reduced accordingly. A tax professional can prevent overpayment.

When a W-2 Job Is Usually the Better Choice

Stability-Focused Workers

W-2 provides predictable pay, automatic withholding, no quarterly deadlines, and no underpayment penalties. For workers early in their careers or managing family finances, the certainty is worth more than any contractor rate premium. If you want to understand every line of your paycheck, our guide on how to read a California pay stub in 2026 breaks down exactly what each deduction means.

Workers Who Need Employer Benefits

Family health coverage in California costs $18,000 to $24,000 annually on the open market. An employer covering 75% provides $13,500 to $18,000 in non-taxable value per year. Add a 401(k) match and paid family leave, and a good W-2 package is extremely hard for a 1099 rate to beat. W-2 employees with employer-sponsored health plans can also pair coverage with an HSA — see the 2026 HSA contribution limits to understand how much pre-tax savings that adds.

When a 1099 Position Is Usually the Better Choice

High-Income Contractors

Above $150,000 in net income, aggressive retirement contributions become powerful. The 2026 Solo 401(k) limit is $72,000 under age 50, $80,000 for ages 50 to 59 and 64+, and $83,250 for ages 60 to 63. Combined with the federal QBI deduction, high-earning contractors can reach effective tax rates comparable to W-2 workers. To see how the numbers look at the $120,000 level specifically, our $120,000 after taxes in California guide shows the full W-2 tax breakdown at that salary.

Experienced Self-Employed Professionals

Contractors with multiple clients, stable deal flow, and established business infrastructure benefit most from 1099 status. The key is client diversification. True financial independence requires operating like a genuine independent business, not functioning as a common law employee under a single company’s control.

Common Myths About 1099 vs W-2 Taxes

“1099 Workers Always Pay More Tax”

False in many cases. A contractor with strong deductions, a Solo 401(k) maxed at $72,000, and a federal QBI deduction may pay a lower effective tax rate than a W-2 employee at the same gross income.

“A Higher Contractor Rate Means More Money”

Not without the math. A contractor at $130,000 versus a W-2 at $105,000 is not necessarily ahead once self-employment taxes, health insurance, lost 401(k) match, and unpaid vacation are subtracted.

“Deductions Eliminate Self-Employment Tax”

No. Deductions reduce taxable income, which lowers income tax. Self-employment tax is calculated on net Schedule C profit regardless. A $1,000 deduction in the 22% bracket saves $220 in income tax. You still spent $780 to earn that deduction.

“Anyone Can Be a 1099 Contractor in California”

AB 5 makes this false. All three parts of the ABC test must be satisfied. Misclassifying workers exposes companies to back taxes, penalties, and unpaid benefit liability. Workers can file a claim with the California Labor Commissioner’s Office through the Department of Industrial Relations.

Decision Framework: Should You Choose 1099 or W-2?

Questions to Ask Before Accepting a 1099 Offer

- Is the 1099 rate at least 25% to 35% higher than the W-2 equivalent?

- Do you have health insurance through another source?

- Do you have savings to cover the first quarterly tax payment?

- Can you handle invoicing, recordkeeping, and taxes?

- Does this arrangement pass California’s ABC test?

Questions to Ask Before Leaving a W-2 Job

- Do you have three to six months of expenses saved?

- Do you have at least two paying clients lined up?

- Have you priced your rate to cover taxes, insurance, and unpaid time off?

- Do you have a quarterly payment plan ready?

Personal Decision Checklist

Consider income level (deductions matter more above $100,000), family health needs (dependents make employer coverage critical), risk tolerance (1099 income is irregular), financial discipline (contractors must self-withhold), and California industry (AB 5 restricts contractor classification in many fields).

Frequently Asked Questions

Do 1099 workers pay more taxes in California?

Usually yes at the baseline. 1099 workers pay the full 15.3% self-employment tax versus the 7.65% W-2 employees pay. Contractors with strong deductions, maxed retirement accounts, and QBI eligibility can close that gap substantially.

How much more should a 1099 job pay than a W-2 job?

25% to 35% more to break even. A $80,000 W-2 with benefits needs a $100,000 to $108,000 1099 rate to be equivalent. In high-cost California markets, the premium may need to be 40%.

Can I receive both a W-2 and a 1099 in the same year?

Yes. W-2 income and 1099 income are reported on the same return. 1099 profit above $400 triggers self-employment tax. W-2 withholding does not cover 1099 taxes, so adjust quarterly payments or increase W-2 withholding to avoid a penalty.

Is California stricter than other states about 1099 workers?

Yes. AB 5’s ABC test is one of the strictest classification standards in the country. California puts the burden on businesses to prove all three conditions are met and actively enforces the rules.

Can 1099 contractors deduct health insurance?

Yes, if not eligible for coverage through a spouse’s employer. Health, dental, and vision premiums are 100% deductible above the line on Form 1040, reducing federal AGI directly. California conformity differs slightly on the state side.

What happens if I do not make quarterly estimated tax payments?

Both the IRS and California FTB charge underpayment penalties. Skipping all year means a large lump sum in April. Set aside 25% to 30% of every contractor payment and make quarterly payments on schedule.

How can I estimate my take-home pay as a contractor?

Start with gross contract income. Subtract business expenses to get net profit. Calculate SE tax at 15.3% on 92.35% of net profit. Deduct 50% of SE tax, then apply federal and California income tax brackets. Budget separately for health insurance and retirement contributions. The fastest way to get a precise number is our California paycheck calculator, which handles all the withholding math automatically.

Can a company legally switch me from W-2 to 1099?

Only if the new arrangement passes all three parts of the ABC test. Same work, same company, same control structure is almost certainly illegal under AB 5. Report suspected misclassification to the California Labor Commissioner or EDD. Workers who are owed unpaid wages as a result of misclassification may also be entitled to a California waiting time penalty on top of back pay.

Final Verdict: Which Option Leaves More Money in Your Pocket?

Best Choice for Most Employees

For workers earning under $120,000, especially those with families, the W-2 wins on total value. Employer tax contributions, health subsidies, 401(k) matching, and PTO create a package a 1099 rate rarely beats without a major premium. A 4% employer match over 25 years accumulates hundreds of thousands of dollars more than an unmatched contractor account at the same base income.

Best Choice for Most Contractors

Experienced professionals earning above $120,000 with multiple clients, outside health coverage, and maxed retirement accounts often come out ahead as 1099. Deductions, QBI benefits, and income flexibility create real tax efficiency at higher income levels.

One Simple Rule for Comparing Any Offer

Never compare gross to gross. Add every benefit dollar to the W-2 side. Subtract every hidden cost from the 1099 side. Compare what actually lands in your bank account. That number is the only one that matters. Our 1099 vs W-2 comparison guide and gross pay calculator can help you model both sides precisely before making any decision.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.