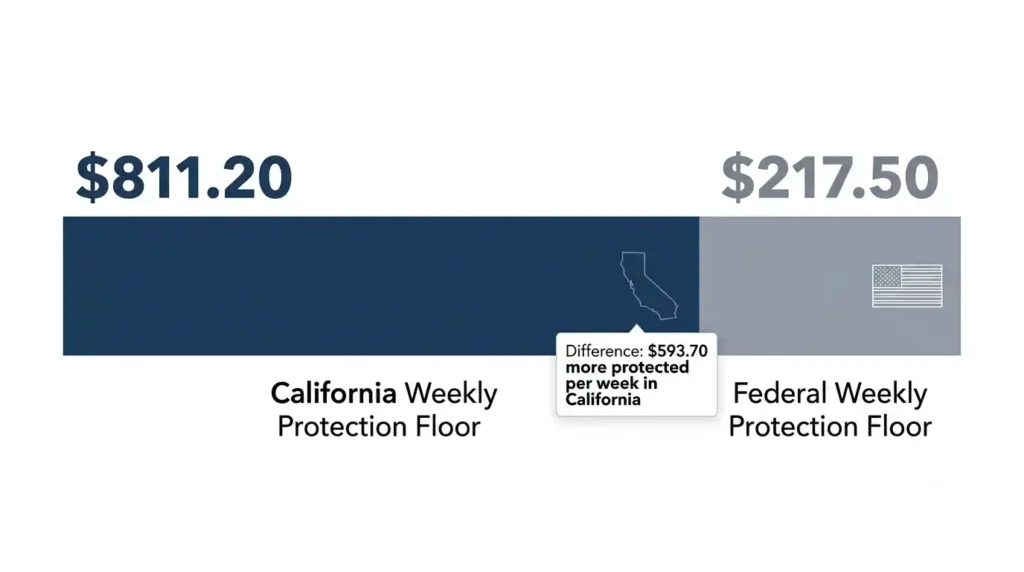

California limits wage garnishment to the lesser of 20% of disposable earnings or 40% above the minimum wage threshold, whichever is smaller. With the statewide minimum wage at $16.90 per hour in 2026, workers earning $811.20 or less per week in disposable pay are fully protected from standard consumer debt garnishment.

That floor is higher than the federal protection by more than $593 per week. However, child support, tax levies, and federal student loans follow separate rules with higher limits. Deadlines in this process are strict, and missing them can cost you money you could have kept.

California Wage Garnishment at a Glance

Wage garnishment is when a court orders your employer to deduct part of your paycheck and send it directly to a creditor. It happens only after a creditor has sued you and won a court judgment against you.

Most garnishments in California involve consumer debts, child support, tax levies, or student loans. Each follows different rules and different limits.

California workers have three key protections: the right to receive notice before garnishment begins, the right to file a Claim of Exemption if withholding would prevent you from covering basic living expenses, and the right not to be fired over a single garnishment order. To see exactly how garnishment affects your specific paycheck, use the California paycheck calculator to run your numbers before and after withholding.

California vs Federal Wage Garnishment Rules

Key Differences Between State and Federal Limits

Federal law under the Consumer Credit Protection Act, codified at 15 USC Section 1673, caps garnishment at 25% of disposable earnings or the amount exceeding 30 times the federal minimum wage of $7.25 per hour, whichever is less. That puts the federal protection floor at $217.50 per week. California’s floor using the $16.90 state minimum wage is $811.20 per week. California also uses a 20% cap versus the federal 25%. When both laws apply, the one that protects more of your pay wins. That is almost always California law.

Comparison Table: California vs Federal Garnishment Limits

| Rule | California (2026) | Federal |

|---|---|---|

| Maximum withholding (consumer debt) | Lesser of 20% of disposable earnings OR 40% above 48x state minimum wage | Lesser of 25% of disposable earnings OR amount above 30x federal minimum wage |

| Weekly protection floor | $811.20 (48 x $16.90) | $217.50 (30 x $7.25) |

| Exemption options | Claim of Exemption for hardship | Limited federal exemptions |

| Employee anti-retaliation protection | Cannot be fired for single garnishment | Cannot be fired for single garnishment |

How Wage Garnishment Works in California

The Legal Process Before Garnishment Begins

A creditor must sue you in court and win before any garnishment can begin. The debt goes delinquent, the creditor files a lawsuit, a judge enters a court judgment, and the creditor then takes steps to enforce it. You have the right to respond before any judgment is entered.

Child support agencies, the IRS, and the California Franchise Tax Board can initiate garnishment without a court judgment. For everyone else, the full lawsuit process applies.

AB 2837, effective in 2025, requires creditors to verify your current address within 12 months before submitting garnishment papers to the levying officer. This law also limits how frequently and for how long an EWO can be enforced under CCP § 706.022.

How an Earnings Withholding Order Works

The creditor’s attorney files an Application for Earnings Withholding Order using form WG-001, then applies for a Writ of Execution using form EJ-130. That writ authorizes the sheriff to issue an Earnings Withholding Order using form WG-002, served on your employer along with Employee Instructions form WG-003. Your employer must give you a copy within 10 days. California Code of Civil Procedure Section 706.051 governs employer obligations and the timing of withholding.

Timeline From Lawsuit to First Garnished Paycheck

From lawsuit filing to first garnished paycheck takes roughly three to six months. Once your employer is served, California law requires a wait until the first pay period ending at least 30 days after service before withholding begins. That window is your time to file a claim of exemption.

Which Debts Can Lead to Wage Garnishment?

Consumer Debts

Credit card balances, medical bills, personal loans, payday loan debts, and collection accounts all require a court judgment first. Payday lenders have no special garnishment authority. All unsecured consumer creditors are subject to the 20% cap and the minimum wage protection floor. See the California labor laws category for related worker protections.

Student Loan Garnishment

Federal student loans in default can trigger administrative wage garnishment without a court judgment. The federal government can take up to 15% of your disposable earnings, and you must be left with at least 30 times the federal minimum wage per week. Private student loans require a court judgment first, like any consumer debt.

Child Support Garnishment

Child support can take up to 50% of disposable earnings if you are supporting another spouse or child, or up to 60% if you are not. If you are more than 12 weeks behind, an additional 5% is added. Child support garnishments hold the highest priority and go ahead of all other orders.

Tax Debt Garnishment

The IRS and the California Franchise Tax Board do not need a court judgment. They issue a tax levy directly to your employer after advance notice. The levy calculation factors in dependents and standard deduction. Resolving tax debt directly with the agency through an installment agreement or offer in compromise is usually faster than waiting for a levy. Understanding your California tax brackets in 2026 can help you estimate how much state tax debt exposure you may have.

How Much Can Be Garnished From Your Paycheck in California?

California Wage Garnishment Limits

Under California Code of Civil Procedure Section 706.050, your employer withholds the lesser of 20% of disposable earnings or 40% of the amount disposable earnings exceed the minimum wage threshold for your pay period. The weekly threshold is $811.20 (48 x $16.90). The biweekly threshold is $1,622.40 (96 x $16.90). The actual amount withheld is often lower than the 20% ceiling. Many workers near the threshold end up with very small garnishments or none at all. For full details on how the $16.90 rate was set and what it means for paychecks across California, see the California minimum wage 2026 guide.

Per CCP § 706.050, if you work where the local minimum wage exceeds the state rate, the local rate applies to the calculation. Workers in cities like Los Angeles, San Francisco, or Santa Monica may have a higher protection floor than the statewide baseline. The $811.20 floor in the examples below reflects the $16.90 statewide rate. If your local rate is higher, your floor is higher too.

Child support, taxes, and federal student loans have separate and usually higher limits.

What Are Disposable Earnings?

Disposable earnings are what remains after your employer removes all legally required deductions. Garnishment is calculated on disposable earnings, not gross wages. If you are unsure what deductions appear on your paycheck and why, the guide on how to read a California pay stub walks through every line item in plain language.

Deductions Included Before Calculating Garnishment

Federal income tax, California state income tax, Social Security taxes, Medicare taxes, California SDI, and mandatory public employee retirement contributions are all required deductions. These come out first, and garnishment is calculated on what remains.

Deductions Not Included

Health insurance premiums, voluntary 401(k) contributions, union dues, and wage assignments do not reduce disposable earnings for garnishment purposes.

Income That May Be Protected From Garnishment

Government Benefits Protected by Law

Social Security retirement and disability benefits, Supplemental Security Income (SSI), veterans benefits, and public assistance payments are fully exempt. Direct deposits of these funds are automatically protected up to two months’ worth. If you receive benefits by check, you may need to prove the funds are exempt in court. The Social Security Administration provides official guidance on which benefit types qualify for automatic protection.

Other Potentially Exempt Income

Disability income from state programs, workers’ compensation benefits, unemployment insurance payments, and many forms of retirement income carry protections. The strength of those protections depends on the income source and how the funds are held. California’s paid family leave and SDI benefits are generally protected as well.

What Happens After Protected Funds Are Deposited Into a Bank Account

Mixing protected funds with regular income in the same account makes it harder to prove which dollars are exempt. This is called commingling. If your account is levied, you will need documentation showing the source of the funds. Keeping protected benefits in a separate account and saving direct deposit statements makes this easier to prove.

Financial Hardship Exemptions Explained

Situations That May Qualify

A judge can reduce or eliminate garnishment if you show the withheld earnings are necessary to support yourself or your dependents. Supporting minor children, high housing costs, significant medical expenses, or recent loss of another household income are all factors courts consider.

Evidence Courts Commonly Expect

Bring your lease or mortgage statement, recent utility bills, childcare invoices, medical bills, and records of household expenses. Specific numbers are more persuasive than general descriptions.

Paycheck Calculation Examples

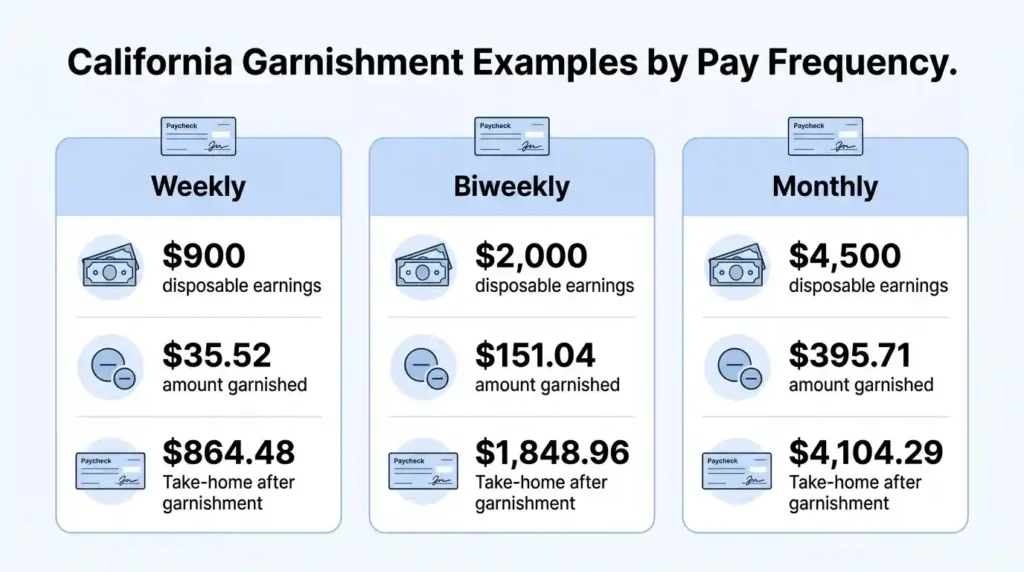

Weekly Paycheck Example

Disposable earnings: $900 per week. Weekly threshold: $811.20 (48 x $16.90).

- Option A: 20% of $900 = $180

- Option B: 40% of ($900 minus $811.20) = 40% of $88.80 = $35.52

The creditor can only garnish $35.52 per week. You keep $864.48.

Biweekly Paycheck Example

Disposable earnings: $2,000 biweekly. Threshold: $1,622.40 (96 x $16.90).

- Option A: 20% of $2,000 = $400

- Option B: 40% of ($2,000 minus $1,622.40) = 40% of $377.60 = $151.04

The creditor is limited to $151.04. You keep $1,848.96.

Monthly Salary Example

Disposable earnings: $4,500 per month. Threshold: $3,510.72 (208 x $16.90).

- Option A: 20% of $4,500 = $900

- Option B: 40% of ($4,500 minus $3,510.72) = 40% of $989.28 = $395.71

The creditor takes $395.71 per month. At higher income levels, the 20% cap is usually the binding limit. Browse the paycheck scenarios category for more examples at different salary levels across California.

Special Situations and Edge Cases

What Happens If You Change Jobs?

Changing jobs pauses garnishment, it does not erase it. The creditor obtains a new Earnings Withholding Order and serves your new employer. The judgment remains fully enforceable. If you leave the job entirely, California’s final paycheck law still requires your employer to pay all earned wages on time.

What Happens If You Have Multiple Jobs?

Each employer receives a separate EWO and calculates garnishment based only on earnings from that job. If both jobs pay below the threshold, neither can be garnished. The part-time vs full-time paycheck guide covers how withholding works when income comes from more than one employer.

Can Bonuses, Commissions, and Overtime Be Garnished?

Yes. Commissions, bonuses, overtime, and vacation pay are all subject to garnishment. Customer-paid tips are generally not included because they are not paid by the employer. Employer-distributed tips may be. The same percentage limits apply. If you receive significant bonus income, the California bonus tax rate guide explains how bonuses are withheld and how garnishment interacts with supplemental wage payments. For overtime specifically, California’s rules on overtime pay calculations affect what your gross overtime earnings look like before the garnishment formula applies.

What If You Are Self-Employed or a Gig Worker?

Independent contractors and gig workers do not receive a traditional paycheck, so earnings withholding orders do not apply. Creditors pursuing self-employed workers use bank levies instead, which take funds directly from a bank account and follow a separate set of exemptions. The 1099 vs W2 tax comparison for California explains how contractor status affects your exposure to collection.

What Happens When Multiple Garnishments Exist?

Child support goes first. Tax levies from the IRS and FTB follow. Consumer debt garnishments come last. Total withholding cannot exceed the applicable cap regardless of how many orders exist. If child support is already at the maximum, a consumer creditor waits until it is satisfied.

If both spouses have separate garnishment orders, each order applies only to that spouse’s wages. If you are already being garnished for child support and a consumer creditor also holds an order, the consumer creditor collects nothing until the child support withholding drops below the consumer cap. That can take months or years.

Common Myths About California Wage Garnishment

“Creditors Can Garnish Without Going to Court”

False for most consumer debts. Creditors must file a lawsuit, win a court judgment, and follow California’s enforcement procedures. Child support agencies, the IRS, the FTB, and federal student loan agencies are the exceptions.

“Changing Jobs Stops Garnishment Permanently”

Changing jobs creates a gap, not a solution. The creditor files a new order with your new employer. The judgment can be renewed and enforced for years.

“All My Income Can Be Taken”

California law prevents this. The minimum wage protection floor, the 20% cap, and the hardship exemption process together ensure you keep enough to meet basic living expenses. Low-wage workers often cannot be garnished at all under California’s formula.

“Employers Can Ignore Garnishment Orders”

They cannot. An employer who fails to comply with a valid Earnings Withholding Order faces personal liability to the creditor for amounts that should have been withheld.

“If I Ignore the Notice, It Will Go Away”

It will not. Ignoring the notice means losing your window to file a claim of exemption before garnishment begins. Money withheld before you file is not automatically returned. Waiting can cost you hundreds of dollars.

What To Do Immediately If You Receive a Wage Garnishment Notice

First Steps to Take Within the Next 24 Hours

Read every page of the paperwork. Identify the creditor, find the case number, confirm all deadlines, and verify the debt is actually yours and the amount is correct. You have a narrow window to respond. The California Department of Industrial Relations provides official guidance on worker rights during wage-related legal proceedings.

Documents You Should Gather Right Away

Collect your most recent pay stubs, all garnishment paperwork, prior correspondence about the debt, and monthly household expense records. A hardship claim requires documented proof of your expenses.

Mistakes That Can Make the Situation Worse

Do not ignore the notice. Do not miss the exemption filing deadline. Do not assume your employer can refuse the order. Do not quit without understanding the garnishment follows you to your next job. If you lose your job involuntarily, the EWO becomes temporarily unenforceable, but the judgment and accruing interest remain. A new order can be issued the moment you start a new job.

California’s garnishment formula ties the protection floor to the state minimum wage, not a fixed dollar amount. As the minimum wage rises, so does your protected floor. The 2026 formula reflects the $16.90 statewide rate effective January 1, 2026.

How to Stop or Reduce Wage Garnishment in California

Filing a Claim of Exemption

If garnishment prevents you from covering basic living expenses, you can file a Claim of Exemption. There is no automatic income test. You must document that your earnings are necessary for support. File as early as possible. Money withheld before you file is generally not returned unless you win the hearing.

Required Court Forms

Form WG-006

Form WG-006 is the Claim of Exemption for Wage Garnishment. File it with the levying officer, usually the county sheriff, not with the court. The current version is effective January 1, 2026. Submit it to the levying officer listed on your Earnings Withholding Order. It asks for your pay frequency, your grounds for exemption, and any amount you are willing to have withheld. All forms are available through the California Courts Self-Help Guide at no cost.

Form WG-007 or EJ-165

Form WG-007 (also called EJ-165) is the Financial Statement accompanying your claim. It covers monthly income and expenses including rent, food, utilities, childcare, insurance, and medical costs. List every dependent. A vague or incomplete statement weakens your claim.

What Happens After You File

The levying officer sends a Notice of Filing of Claim of Exemption using form WG-008 to the creditor. The creditor has 10 days to respond. If they oppose, they file a Notice of Opposition to Claim of Exemption using form WG-009. You then receive a Notice of Hearing on Claim of Exemption using form WG-010 with a court date. A judge decides at the hearing. If the creditor does not oppose, the employer is told to stop or reduce withholding and any held funds since your filing are returned.

Other Ways to Stop Wage Garnishment

Negotiating Directly With the Creditor

As the judgment debtor, you can contact the judgment creditor to discuss a lump-sum settlement, a payment plan, or a temporary pause. Get any agreement in writing before stopping payments. A verbal deal does not stop the Earnings Withholding Order. When settled, ask the creditor to file both a release of the EWO with the levying officer and an Acknowledgment of Satisfaction of Judgment with the court. Without both, your employer may keep withholding.

Challenging the Underlying Judgment

If you were never properly served with the original lawsuit, you may be able to file a motion to vacate the judgment. Default judgments are especially vulnerable when the debtor was not properly notified. A creditor may have served papers at an old address, and you may not have learned about the judgment until a garnishment notice arrived years later. Check the case number on your EWO, pull the court file, and review how service was documented. Faulty service can make vacating the judgment possible. This process benefits from an attorney but can fully eliminate the garnishment if successful.

Bankruptcy as a Last Resort

Filing for bankruptcy triggers an automatic stay that immediately halts most wage garnishments. Chapter 7 bankruptcy can eliminate many consumer debts entirely, ending garnishment permanently. Chapter 13 reorganizes debts into a payment plan with garnishments paused during the plan. Bankruptcy does not discharge child support, alimony, or most tax debts, so those garnishments resume after the bankruptcy concludes.

Employer Rules and Responsibilities

What Employers Must Do

On receiving an Earnings Withholding Order, the employer must give the employee a copy within 10 days, return the Employer’s Return form WG-005 to the levying officer within 15 days, and begin withholding on the first pay period ending at least 30 days after service. All required forms are published by the Judicial Council of California and available through the California Courts Self-Help Guide at courts.ca.gov.

Can Your Employer Fire You?

No, not for a single garnishment. Federal and California law both prohibit termination over one wage garnishment. Contact the California Labor Commissioner if your employer fires you over a single order. The protection weakens if you have prior garnishments from different judgments.

Frequently Asked Questions

Can a creditor garnish wages without a judgment in California?

For most consumer debts, no. Creditors must sue, win, and obtain a court judgment first. The exceptions are child support agencies, the IRS, the California Franchise Tax Board, and federal student loan agencies, which can garnish administratively.

How long does wage garnishment last in California?

A single Earnings Withholding Order is valid for up to one year. If unpaid, the creditor can seek a new order. Court judgments are valid for 10 years and can be renewed. Interest accrues on the unpaid balance under CCP § 685.010 at 10% per year for most judgments. For personal consumer debt judgments under $50,000 and medical debt judgments under $200,000 entered or renewed on or after January 1, 2023, the rate is 5% per year. Most standard credit card and personal loan judgments fall into the 5% category. Sheriff fees and administrative costs are also added to the balance. Once fully paid, the creditor must file an Acknowledgment of Satisfaction of Judgment with the court, and the garnishment ends.

Can I get garnished wages back?

Money withheld after you file a successful Claim of Exemption can be returned. Money withheld before you filed is generally not recoverable. If the judgment is vacated or paid in full, any funds held by the levying officer at that time are returned.

Can my employer fire me because of garnishment?

Not for a single garnishment order. Contact the California Labor Commissioner immediately if they do.

How long do I have to file a Claim of Exemption?

File within 10 days of receiving the Earnings Withholding Order from your employer. Filing before withholding begins gives you the most protection, but you can file at any time during the garnishment.

Does wage garnishment affect my credit score?

The underlying court judgment likely already appears on your credit report. Satisfying the judgment and requesting an acknowledgment of satisfaction from the court can improve your credit over time.

Can my bank account also be levied?

Yes. A bank levy is a separate tool a creditor can use alongside or instead of wage garnishment. Social Security and certain federal benefits deposited directly are automatically protected up to two months’ worth, but commingling those funds with other income can complicate the exemption.

Can I negotiate a settlement after garnishment starts?

Yes. Many creditors will negotiate a lump-sum settlement or payment plan even after garnishment begins. Get any agreement in writing. The written settlement must state the creditor will release the garnishment order upon payment. Do not pay without that written release.

Key Takeaways and Next Steps

California’s garnishment laws give low and moderate wage earners real protection. Workers at or near the minimum wage floor often cannot be garnished at all. Above the threshold, the 20% cap limits how much any consumer creditor can take, and hardship exemptions are available if even that amount is too much.

Act immediately. Review your paperwork today. File your Claim of Exemption before withholding begins if you qualify. Contact the creditor to explore a settlement if you can offer one.

Missing the exemption deadline by even a few days can cost you money you could have kept. If the amount at stake is significant, a free consultation with a California consumer law attorney or legal aid organization is worth the call.

For official court forms including WG-006 and WG-007, visit courts.ca.gov. For employee rights questions, contact the California Labor Commissioner at dir.ca.gov. For a complete index of California payroll and labor law topics, browse the California payroll taxes and paycheck basics categories.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.