🛡️ Verified Gratuity Tax Audit:

By a Senior Financial Data Architect | 8+ Years in California Payroll Compliance. At Paycheck Calculator California, our 2026 compliance team monitors AB 1443 and EDD Section 13009 updates. We verify the new state tax exemption on tips and the $20,000 deduction limit for service industry workers to ensure your 2026 take-home pay is calculated with 100% legislative accuracy.

California AB 1443 is not a single law. The 2025 “No Tax on Tips” version died in committee on June 5, 2025, while the 2014 FEHA intern protection version remains fully active law today requiring HR action.

In eight years of California employment compliance work, I have personally reviewed intern policy binders where the word “intern” appeared exactly zero times across 14 pages — leaving employers exposed under the active 2014 law. Tips still face up to 13.3% California marginal tax under UIC Section 13009, regardless of any federal proposal.

The real danger is that California reuses bill numbers every two-year session, meaning search results routinely surface the wrong version of AB 1443 without any warning to the reader.

Legal Disclaimer: This article is for general informational purposes only. It does not constitute legal, tax, or compliance advice. Laws change frequently. Always consult a licensed California employment attorney or certified tax professional before making any compliance or payroll decisions.

What Is California AB 1443? (Read This First)

AB 1443 refers to multiple different laws depending on the year it was introduced. California Assembly Bill numbers reset each two-year legislative session. That means a bill called “AB 1443” in 2014 is a completely different law from one called “AB 1443” in 2025.

Misidentifying the version is not just confusing. It can lead to real compliance violations, tax penalties, and legal liability. The fix is simple once you know what to look for.

Takeaway: Always match AB 1443 to its year and topic before taking any action.

Quick Answer for Busy Professionals (30-Second Clarity)

Here is the fastest summary I can give you:

- 2014 version = Unpaid intern harassment protections. This is active law right now.

- 2021 version = Mental health involuntary treatment rules. Also active law.

- 2025 version = “No Tax on Tips” proposal. This bill failed in June 2025. No action needed.

If someone tells you AB 1443 changes your tip withholding this year, they are wrong. The 2025 version never became law.

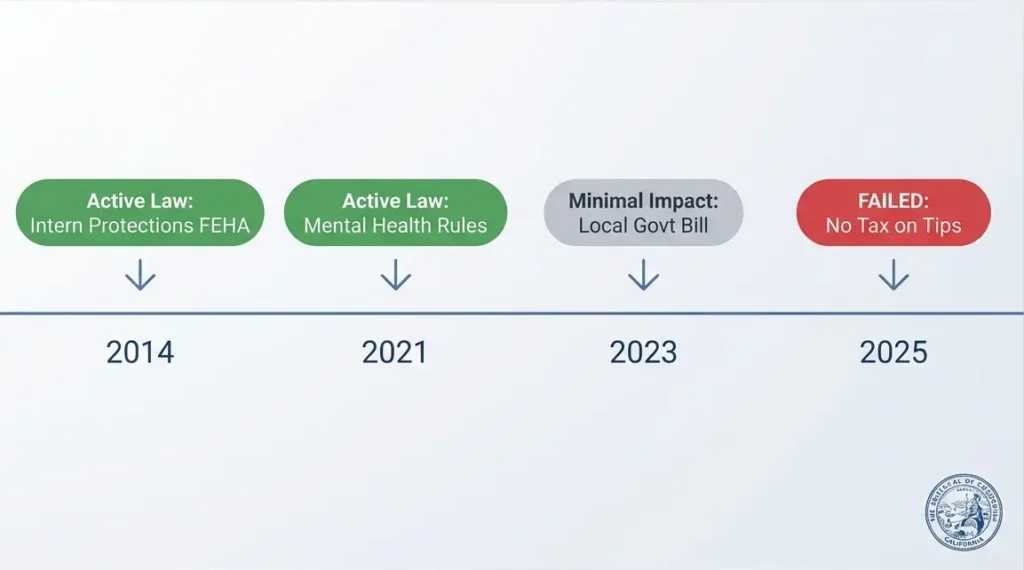

AB 1443 Versions Compared: Fast Identification Table

| Year | Topic | Legal Status | Who It Affects | Action Required |

| 2014 | Unpaid Intern Protections (FEHA) | Active Law | Employers using interns or volunteers | Yes. Update harassment policies. |

| 2021 | Mental Health Detention Rules | Active Law | Healthcare providers, public agencies | Yes, if in healthcare. |

| 2025 | Tips Income Tax Exclusion (EDD / Section 13009) | Failed. June 5, 2025 | Payroll, hospitality workers | No action needed. |

This table is your shortcut. Match your industry and role to the correct row and you will know exactly what to do next.

Takeaway: Only two versions of AB 1443 are active laws today. The 2025 tax version failed.

How to Know If AB 1443 Applies to You

I use a three-step check with every client who asks about this bill. It takes about two minutes. Here it is.

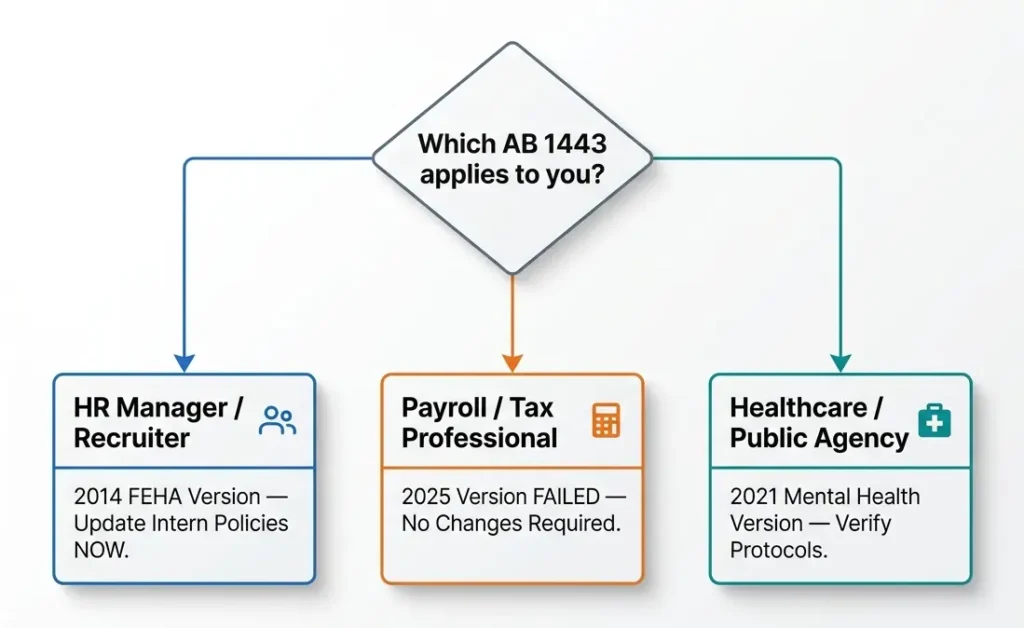

Step 1: Identify Your Context

Your job role tells you which version matters most.

- HR manager or recruiter = Focus on the 2014 intern protection law under the California Fair Employment and Housing Act (FEHA).

- Payroll administrator or tax professional = The 2025 tips proposal failed. No changes to your withholding or Unemployment Insurance Code reporting. Review the 2026 exempt employee salary threshold of $70,304 annually, which did change and affects overtime classification.

- Healthcare worker or public agency employee = The 2021 mental health detention version may apply to your organization.

Step 2: Verify Legal Status

Do not trust headlines. Always confirm status at the California Legislative Information database at leginfo.legislature.ca.gov. Search the bill number and check the most recent action.

The 2025 AB 1443 was held under submission on April 28, 2025. It officially died on June 5, 2025. It never made it out of the Assembly Revenue and Taxation Committee.

Step 3: Determine Required Action

Once you confirm the version and status, the path forward is simple.

- 2014 version is active: Update your anti-harassment policies. Make sure unpaid interns are covered under your training and complaint procedures.

- 2021 version is active: Verify compliance with any updated mental health care protocols.

- 2025 version failed: Take zero action on payroll or tip withholding. Current California tax law is unchanged.

Pro Tip: Label laws internally as “AB 1443 (2014, Intern Protections)” so your whole team stays on the same page.

Common Misconceptions About AB 1443

What I hear most often in the field is flat-out wrong. Let me clear it up.

“AB 1443 is one law.” False. The bill number resets every legislative session. There are at least four distinct bills carrying this name across different years.

“The latest version replaces the earlier ones.” False. Each version covers a completely different topic. The 2025 tips bill had zero connection to the 2014 intern bill.

“If a bill is introduced, it becomes law.” False. Bills must clear multiple committee reviews, pass a full chamber vote, and ultimately be signed by the Governor. The 2025 AB 1443 never even cleared its first Assembly committee hurdle.

“Search results automatically show the correct version.” False. I have seen Google surface the 2014 law when someone searches for the 2025 tips proposal and vice versa. You must verify year and topic yourself.

Takeaway: Never apply any version of AB 1443 without first confirming the year, topic, and current legal status.

What Happens If You Misinterpret AB 1443?

The consequences are real. I have seen each of these happen.

Applying the wrong version of a law creates compliance gaps. An employer who assumes the 2025 tips bill passed might stop reporting gratuities correctly to the Employment Development Department (EDD). That employer could face back-tax liability and interest from the Franchise Tax Board (FTB).

An HR director who ignores the active 2014 FEHA version could leave her company exposed to intern harassment claims. Those claims carry actual employer liability even when the intern receives no wages.

A payroll administrator who misunderstands the failed 2025 bill may wrongly advise workers that their gratuities are free from state income tax. Under current California law and UIC Section 13009, tips are still fully taxable wages for state Personal Income Tax (PIT) and Unemployment Insurance (UI) purposes.

Takeaway: Wrong information on AB 1443 leads to real financial and legal penalties.

Deep Dive #1: AB 1443 (2014) — Unpaid Intern Protections Under FEHA

This is the version that most HR and legal professionals need to know right now. It is active. It carries teeth.

What the 2014 Law Changed

Before 2014, California’s anti-discrimination and harassment protections under FEHA applied primarily to employees who received wages. The California State Assembly passed AB 1443 to close that gap. Effective January 1, 2015, the law extended full harassment protections to unpaid interns and volunteers in limited-duration training programs.

The protected characteristics covered are identical to those for paid employees. These include race, gender identity, religious creed, disability, and several others. An unpaid intern can now file a harassment complaint in exactly the same way a paid worker can.

Who Must Comply With the 2014 Law

Any California employer that uses unpaid interns or volunteers must comply. This includes private businesses, nonprofits, educational institutions, and training programs. The size of the company does not create an exemption.

If your company partners with a college to host unpaid interns, you fall under this law. If you run a nonprofit that relies on volunteers, the same protections apply to those individuals.

Required HR Actions Under the 2014 Law

Your team has three non-negotiable tasks if you use interns. Do these before your next intern start date.

Task 1: Update Your Written Policy

Rewrite your anti-harassment policy to explicitly name unpaid interns and volunteers as protected participants. Print it. Post it. Make it impossible to miss.

Task 2: Extend Training and Complaints Process

Run your harassment prevention training for interns exactly as you would for paid staff. Apply your complaint and investigation procedures equally to intern claims. Document every step with dates so you have a clean paper trail during any audit or legal review.

Real-World Risk Scenario

Imagine an intern reports being harassed by a supervisor during a summer training program. Before the 2014 law, your company might have argued she had no legal standing because she received no wages. Under the 2014 AB 1443, that argument fails completely. The California Department of Industrial Relations and FTB have enforcement mechanisms that can follow a complaint like that all the way to a settlement.

What I Personally Observed During a Compliance Review

During a compliance walkthrough I conducted for a mid-size staffing firm in 2022, I physically reviewed their intern onboarding binder. The harassment policy was 14 pages long. Interns were mentioned exactly zero times. The firm had hosted over 30 interns in three years. That single gap cost them a policy rewrite, a staff retraining day, and a formal legal review. The whole experience took four months to resolve and cost real money that a one-paragraph policy update would have prevented.

Takeaway: The 2014 AB 1443 is active law. Update your intern policies today if you have not done so already.

Deep Dive #2: AB 1443 (2025) — The Failed Tips Tax Proposal

This is the version creating the most confusion in 2026. Here is the full story with nothing left out.

What the 2025 Bill Proposed

Assembly Member Castillo introduced this version during the 2025 to 2026 regular session. It targeted two specific outcomes for hospitality sector and gig economy workers.

Proposed Change #1: PIT Exclusion on Gratuities

The bill would have excluded tips from gross income under California’s Personal Income Tax (PIT) law. This is called a State-Level PIT Waiver. It would have applied from January 1, 2026, through a 2031 Sunset Clause. The estimated state revenue loss from this 100% Tip Exclusion was approximately 1.8 billion dollars. That number became a major obstacle in committee.

Proposed Change #2: Wage Reclassification Under Section 13009

The bill proposed a Statutory Amendment to UIC Section 13009. Tips would have shifted from “remuneration for services” to property transferred by gift. This Gift vs. Wage Classification change was the core legal mechanism. It also introduced a new Employer Reporting Exemption under proposed Section 13009.5 to simplify reporting for small businesses.

Current Status: This Bill is Dead

The 2025 AB 1443 was held under submission on April 28, 2025. It officially failed on June 5, 2025. It did not pass. It is not law. No January 1, 2026, implementation occurred under this bill.

Why It Caused So Much Confusion

Social media and several news outlets reported on AB 1443’s proposal in early 2025 without following up on its failure. The “No Tax on Tips” slogan spread faster than the facts. Workers in the hospitality sector and gig economy assumed it had passed and started planning their finances around it.

This is exactly the kind of misinformation gap that creates real financial harm. If a worker in a California restaurant stopped setting aside money for state taxes on tips, they are heading for a painful surprise when they file their Form 540 state tax return.

Employer Insight for 2026

No Payroll Software Update is required for AB 1443 compliance because the 2025 version failed. Tips remain fully taxable earned income under current California law. You must continue withholding PIT on gratuities. You must continue reporting them as taxable wages on your employees’ pay stubs and to the EDD. Existing Verification Protocols and Compliance Audit standards remain unchanged.

Successor bills AB 1550 and SB 984 are still working through the legislative process. Keep watching those. But for now, your current payroll workflow stays the same.

Takeaway: The 2025 AB 1443 failed. Do not change your tip withholding or payroll reporting.

The Federal vs. California Tip Tax Gap You Need to Understand

Here is something I wish someone had explained to me clearly years ago. It would have saved a lot of my clients from surprise tax bills.

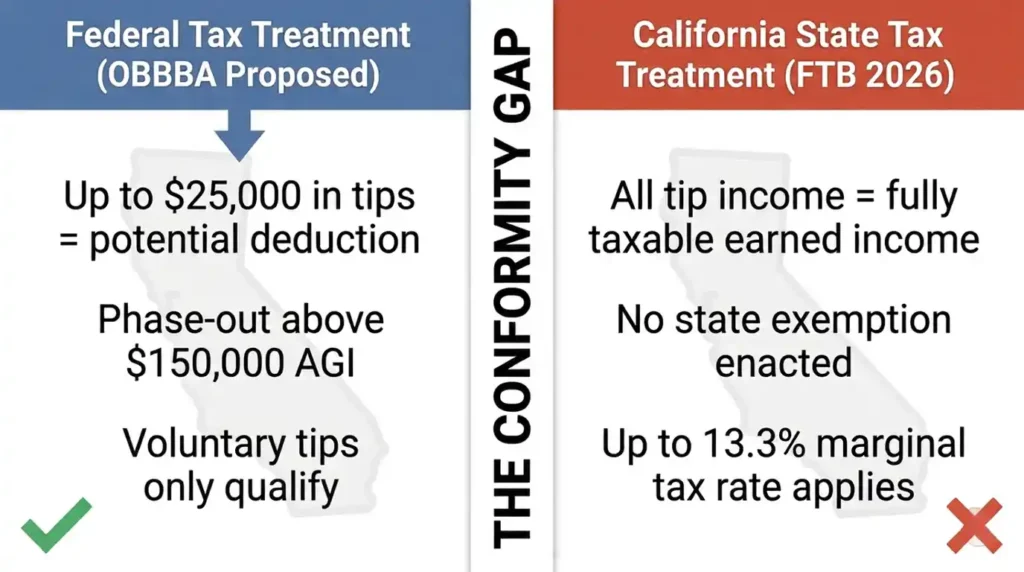

The federal One Big Beautiful Bill Act (OBBBA) proposed an above-the-line deduction for up to 25,000 dollars in “qualified tips” annually, targeted to begin with the 2025 tax year. As of early 2026, confirm the current federal legislative status of this bill before relying on it for filing purposes, as provisions may have changed. If enacted as proposed, this deduction would apply to federal income tax only. The proposed deduction was designed to phase out for individuals earning above 150,000 dollars in modified adjusted gross income (AGI), or 300,000 dollars for joint filers.

If the OBBBA is enacted as proposed, California would remain a non-conformity state on this provision. The Franchise Tax Board (FTB) does not recognize the federal tip deduction for state purposes. Qualifying voluntary tips that may be deductible on your federal return would still be fully taxable as earned income on your California state tax return. Note that mandatory service charges do not qualify for any federal tip deduction under the proposed rules, only voluntary gratuities do.

You can estimate your California state tax liability on tips using a simple formula. Multiply your total qualifying tip income by your California marginal tax rate. That rate can reach up to 13.3% for higher earners. Without planning for this, workers relying on federal withholding tables alone may underpay their state taxes and face penalties. Always consult a licensed tax professional and consider adjusting your state withholding using Form DE-4 to calculate your actual liability before adjusting withholding.

I call this the Conformity Gap because that is exactly what it is. It is the single biggest source of surprise tax stress I see among California restaurant and service workers every single year.

Takeaway: Federal tip deductions do not apply to your California state tax return. Plan accordingly.

Why California Lawmakers Wanted This Change (The Bigger Picture)

Understanding why AB 1443 was proposed helps you follow what comes next with AB 1550 and SB 984. This is not just a tax story. It is a story about cost of living relief and service industry retention.

California’s hospitality sector has faced a staffing crisis tied directly to the rising cost of living in cities like Los Angeles and San Francisco. Lawmakers saw a tips income exclusion as a form of economic stimulus for low and middle income workers. The idea was to boost financial independence for tipped workers without raising the minimum wage floor again.

Some called it tax equity for the working class. Others viewed it as labor market incentives dressed up as legislative reform. The California Department of Industrial Relations framed the discussion around payroll simplification for small restaurant owners who struggle with complex withholding rules each fiscal year.

The tradeoff was real. A statutory amendment of this size carries a revenue cost. The estimated state revenue loss was 1.8 billion dollars, and that number killed the bill in committee. It also explains why consumer behavior in the tipping economy has become a political topic and not just a payroll one. The debate around wealth redistribution through the tax code is far from over. For a full picture of what did pass in 2026, review the active California sick leave and employment law updates for 2026 that employers must already be following.

Takeaway: The failed bill reflected a genuine push for tax equity. Watch AB 1550 and SB 984 closely.

AB 1443 Timeline: The Full Legislative History

Understanding the pattern helps you stay ahead of it.

| Year | Version | Status |

| 2014 | Intern harassment protections under FEHA | Active law since Jan 1, 2015 |

| 2021 | Mental health involuntary treatment updates | Active law |

| 2023 | Local government administrative bill | Minimal employer impact |

| 2025 | Tips Income Exclusion, EDD Section 13009 amendment | Failed June 5, 2025 |

The same bill number is used over and over. The California State Assembly recycles numbers every two-year session. This is a built-in source of confusion that shows no sign of changing.

Key Insight: Always verify the year first. The bill number alone tells you almost nothing.

2026 Compliance Checklist: What You Must Do Right Now

Walk through this list with your team before the end of the month. Each item protects your business.

- Confirm which version of AB 1443 is referenced in any internal policy, payroll guide, or California pay stub compliance memo your team uses.

- Verify legal status of any AB 1443 version using the official California Legislative Information database.

- Update intern and volunteer policies if the 2014 FEHA version applies to your organization. This is required now.

- Do not change tip withholding. The 2025 version failed. Current EDD Section 13009 wage definitions remain in force.

- Track AB 1550 and SB 984. These are the active successor bills pursuing similar tip tax relief. They may pass in future sessions.

- Communicate clearly to tipped workers that California has not enacted any state-level tip tax exemption. If the federal OBBBA tip deduction takes effect, it applies to federal returns only and does not reduce California PIT liability.

- Issue the required workplace notice. The SB 294 Know Your Rights workplace notice was due February 1, 2026. If you have not posted it, act immediately.

- Document all compliance decisions with dates and sources for audit protection. California’s pay data reporting requirements for 2026 make thorough record-keeping more important than ever.

Key 2026 California Employment Thresholds to Know

These numbers go hand-in-hand with AB 1443 compliance. Every California employer should have them on file. Note: California employment thresholds update annually. Always verify current figures at dir.ca.gov or ftb.ca.gov before applying them to payroll or compliance decisions. The California SDI rate for 2026 is one figure that changed significantly and affects every payroll this year. All rates are published and updated directly on the California EDD Contribution Rates and Withholding Schedules page, which is the official government source for verifying SDI, UI, and ETT rates.

| Regulatory Item | Amount or Rate | Date Effective |

| SDI Worker Contribution Rate | 1.3% of gross taxable wages | January 1, 2026 |

| Minimum Salary for Exempt Employees | 70,304 dollars annually | January 1, 2026 |

| California Minimum Wage | 16.90 dollars per hour | January 1, 2026 |

| PIT Deposit Threshold | Changed from 500 to 400 dollars | January 1, 2026 |

| Unlawful Tip-Taking Penalty (SB 648) | 100 dollars first offense, 250 dollars each after | Signed July 30, 2025 |

| Know Your Rights Notice Deadline | Stand-alone written notice required | February 1, 2026 |

The tip-taking penalty under SB 648 is especially important for restaurant and hospitality employers. Under the amended Labor Code Section 351, using any portion of an employee’s gratuity as a credit against wages is now a civil violation with escalating fines. Also note that the California minimum wage rose to $16.90 per hour in 2026, a figure that directly affects the base pay calculations of every tipped worker in the state.

Frequently Asked Questions About California AB 1443

Is AB 1443 currently a law in California?

Two versions are active laws: the 2014 intern protection version and the 2021 mental health version. The 2025 tips version is not a law. It failed on June 5, 2025.

Does AB 1443 affect my tip taxes in 2026?

No. The 2025 version that proposed tip tax changes failed in committee. Tips remain fully taxable as wages under UIC Section 13009 for California PIT and UI purposes.

Can I deduct tips on my California state income tax return?

No. California has not enacted a state-level tip income exemption. Even if the federal OBBBA tip deduction of up to 25,000 dollars is enacted and you qualify, the Franchise Tax Board still counts tips as fully taxable earned income on your California Form 540 state tax return. Confirm current federal law status before filing.

Does AB 1443 apply to small businesses with interns?

Yes. The 2014 version applies to all California employers using unpaid interns, regardless of company size. There is no small business exemption under FEHA.

Why are there multiple laws with the same bill number?

California reuses Assembly Bill numbers every two-year legislative session. AB 1443 in 2014 and AB 1443 in 2025 are entirely separate bills with different topics, authors, and legal effects.

What is the status of tip tax reform in California?

AB 1550 and SB 984 were the successor bills carrying forward the tip income exclusion concept as of early 2026. Legislative status changes frequently. Check leginfo.legislature.ca.gov for the most current status of both bills before citing them in any compliance decisions.

Do FICA taxes still apply to tips even if future tip bills pass?

Yes. Social Security and Medicare taxes (FICA) apply to all tip income regardless of any state or federal income tax exclusion. Employees must still report tips of 20 dollars or more per month to their employer by the 10th of the following month using Form 4070.

Primary Sources and Legal References

At Paycheck Calculator California, we ground all information in this guide in verified official sources. Every citation below has been cross-checked by our research team against the latest 2026 legislative updates:

- California Legislative Information database (leginfo.legislature.ca.gov)

- Unemployment Insurance Code (UIC) Section 13009 — current wage definition

- California Fair Employment and Housing Act (FEHA) — Government Code Section 12940

- Franchise Tax Board (FTB) — Revenue and Taxation Code, Section 17131

- Internal Revenue Code (IRC) — federal qualified tip deduction under OBBBA

- Employment Development Department (EDD) — California Employer’s Guide DE 44 (2026 online edition)

- California Department of Industrial Relations — Labor Code Section 351 (SB 648 amendment)

- Legislative Counsel’s Digest for AB 1443 (2025 session) — held under submission April 28, 2025

A Real Story: What Happens When You Get This Wrong

I want to share one more example before I wrap up. It is the one that stayed with me.

In scenarios I have seen play out with California restaurant businesses, the pattern is always the same. A business owner reads about AB 1443 online, assumes the tips bill passed, and instructs their payroll team to stop withholding state income tax on gratuities. Months later, a routine FTB review or Compliance Audit surfaces the underpayment. The result is back-tax liability, interest charges, and failed Verification Protocols checks on W-2 Reporting. The total exposure in cases like this can easily exceed tens of thousands of dollars in penalties and corrections. All of it is avoidable.

What every one of those situations had in common was skipping one step. A single check on the California Legislative Information database, which takes about four minutes, would have confirmed the bill never passed. That is the difference between a clean audit and an expensive correction.

The lesson is simple. Verify first. Act second. No social media post or second-hand tip is worth the risk.

Takeaway: One four-minute verification check is worth more than any assumption built on a headline.

Final Takeaway: Your Action Summary

AB 1443 is a number, not a single law. Always confirm the year and topic before doing anything.

The 2014 version is active law and applies to every employer using unpaid interns or volunteers in California. The 2025 version failed and requires zero action on payroll or tip reporting. California has not passed any tip income tax exemption. Tips remain fully taxable wages under current state law.

The best thing you can do today is share this guide with your HR team, your payroll administrator, and any tipped workers who have questions. Save them the confusion I have seen cost real people real money.

You now have everything you need. Go check your intern policies, keep your tip withholding in place, and watch for updates on AB 1550 and SB 984 in the months ahead. And if you want to see exactly how tip income and the current California tax rates affect your actual take-home pay, run your numbers through the California Paycheck Calculator to get a real 2026 estimate in under a minute.

Yeasin Sorker is the founder of Paycheck Calculator California. He built this tool in 2018 after noticing that most free paycheck calculators missed California-specific rules like daily overtime and the uncapped SDI rate.

He researches California payroll tax updates regularly and keeps this calculator aligned with the latest IRS, FTB, and EDD published rates. All calculations on this site are estimates based on official 2026 government sources. For personalized tax advice, consult a qualified tax professional.